Term Life Insurance in Singapore A Local Guide

A detailed guide to term life insurance policies available in Singapore, including local regulations and best practices.

A detailed guide to term life insurance policies available in Singapore, including local regulations and best practices.

Term Life Insurance in Singapore A Local Guide

Understanding Term Life Insurance for Singaporeans

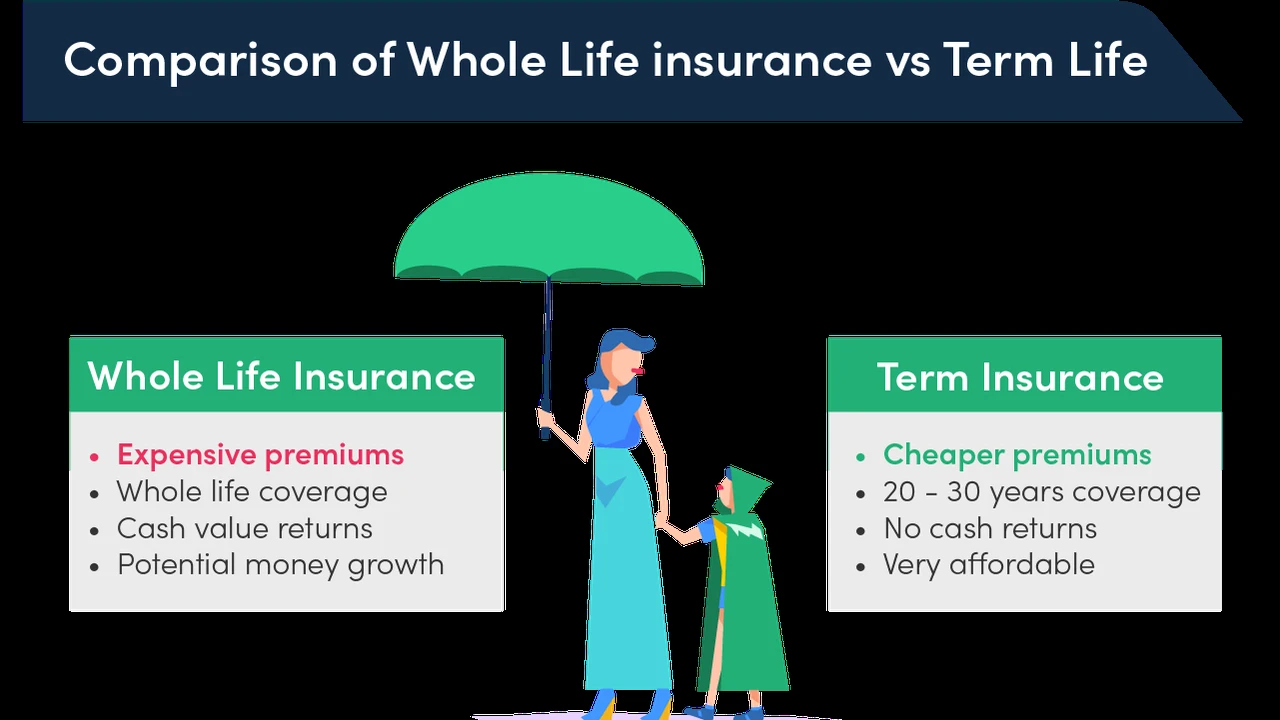

Hey there! If you're living in Singapore and thinking about getting your finances in order, term life insurance is probably on your radar. It's a pretty straightforward product designed to give your loved ones a financial safety net if something unexpected happens to you. Unlike whole life insurance, which covers you for your entire life, term life insurance covers you for a specific period, or 'term.' This makes it generally more affordable, especially when you're younger and just starting out.

So, why is term life insurance a big deal in Singapore? Well, with the high cost of living and rising expenses, ensuring your family's financial stability is paramount. Whether you're a young professional, a parent, or someone planning for retirement, a term life policy can provide peace of mind. It can cover things like outstanding mortgage payments, children's education, daily living expenses, and even medical bills, preventing your family from facing financial hardship during an already difficult time.

In Singapore, the insurance market is quite robust, with many local and international players offering a variety of term life products. This means you have plenty of options, but it also means you need to do your homework to find the best fit for your specific needs. We'll dive into some of the key aspects you should consider, from policy types to local regulations and even some specific product recommendations.

Key Features and Benefits of Singapore Term Life Policies

When you're looking at term life insurance in Singapore, there are a few core features and benefits that stand out. Understanding these will help you compare policies more effectively.

Affordable Premiums and Flexible Terms

One of the biggest draws of term life insurance is its affordability. Because it's not designed to last your entire life, the premiums are generally much lower than whole life policies. You can choose a term that suits your needs, typically ranging from 5 to 30 years, or even up to a specific age like 65 or 70. This flexibility allows you to align your coverage with your major financial commitments, like paying off a home loan or seeing your kids through university.

Lump Sum Payout for Financial Security

Should the unthinkable happen during your policy term, your beneficiaries will receive a tax-free lump sum payout. This money can be used for anything they need – replacing your income, covering debts, or maintaining their lifestyle. It's a direct way to ensure your family's financial future is protected, even if you're no longer there to provide for them.

Convertibility and Renewability Options

Many term life policies in Singapore come with options to convert to a permanent life insurance policy (like whole life or universal life) without needing another medical examination. This is super useful if your needs change and you decide you want lifelong coverage. Similarly, some policies are renewable, meaning you can extend your coverage at the end of the term, though usually at a higher premium due to your increased age.

Riders and Additional Coverage for Enhanced Protection

To customize your policy, you can often add various riders. These are optional benefits that enhance your coverage. Common riders include:

- Critical Illness (CI) Rider: Pays out a lump sum if you're diagnosed with a specified critical illness. This is incredibly important in Singapore, where healthcare costs can be substantial.

- Total and Permanent Disability (TPD) Rider: Provides a payout if you become totally and permanently disabled and can no longer work.

- Waiver of Premium Rider: Waives future premiums if you become disabled or critically ill, ensuring your coverage continues without financial strain.

- Accidental Death Benefit Rider: Offers an additional payout if your death is due to an accident.

Local Regulations and Best Practices for Singapore Term Life

Navigating the insurance landscape in Singapore means understanding some local nuances and regulations. The Monetary Authority of Singapore (MAS) regulates the insurance industry, ensuring consumer protection and fair practices.

MAS Regulations and Consumer Protection

MAS sets out guidelines for insurers, including disclosure requirements, capital adequacy, and conduct. This means you can generally trust that policies offered by licensed insurers are legitimate and regulated. Always ensure you're dealing with a licensed financial advisor or insurer.

Free Look Period Your Right to Review

In Singapore, most life insurance policies come with a 'free look period,' typically 14 days from the date you receive your policy document. During this time, you can review the policy terms and conditions. If you decide it's not for you, you can cancel it and get a full refund of the premiums paid, minus any medical examination costs incurred by the insurer. This is a great safety net!

Financial Needs Analysis The Importance of Professional Advice

Before purchasing any insurance, a licensed financial advisor in Singapore is required to conduct a Financial Needs Analysis (FNA). This helps them understand your financial situation, goals, and existing coverage to recommend suitable products. Don't skip this step – it's crucial for getting the right coverage.

Nomination of Beneficiaries Ensuring Your Wishes Are Met

It's vital to properly nominate your beneficiaries for your life insurance policy. In Singapore, you can make a trust nomination or a revocable nomination. A trust nomination ensures the proceeds go directly to your beneficiaries without forming part of your estate, which can be important for estate planning. A revocable nomination can be changed at any time. Make sure your nominations are up-to-date and reflect your current wishes.

Comparing Top Term Life Insurance Products in Singapore

Alright, let's get down to some specifics. The Singapore market has a lot to offer, and while I can't give you personalized financial advice, I can highlight some popular products and what makes them stand out. Remember, always consult with a financial advisor to get recommendations tailored to your situation.

Product Spotlight Prudential PRUShield Term

Prudential is a big name in Singapore, and their PRUShield Term is a popular choice. It offers flexible coverage terms and sum assured options. A key feature is its convertibility option, allowing you to switch to a whole life or endowment plan later without further medical underwriting. It's often chosen for its strong brand reputation and comprehensive rider options, including critical illness and total and permanent disability. Premiums are competitive, especially for younger individuals, and it's a solid choice for those looking for a reliable, straightforward term plan.

Product Spotlight Great Eastern GREAT Term

Great Eastern's GREAT Term plan is another strong contender. It's known for its flexibility in choosing policy terms, from 5 years up to age 85. What's interesting about GREAT Term is its guaranteed renewability feature, meaning you can renew your policy at the end of the term without medical underwriting, though premiums will be adjusted based on your age. They also offer a wide range of riders, including early critical illness coverage, which is a significant advantage in Singapore's healthcare landscape. This plan is often recommended for those who value guaranteed renewability and extensive critical illness protection.

Product Spotlight AIA Secure Term

AIA Secure Term is designed to provide comprehensive coverage at an affordable price. It offers a choice of policy terms and sum assured, and like others, it comes with various riders to enhance protection. AIA is known for its strong network of financial advisors and customer service. A notable feature of AIA Secure Term is its potential for higher coverage amounts, making it suitable for individuals with significant financial obligations, such as large mortgages or multiple dependents. They also have competitive rates for non-smokers and those in good health.

Product Spotlight Income iTerm

NTUC Income's iTerm is a digital-first term life insurance product that's often praised for its simplicity and ease of application. You can get a quote and apply online, making it very convenient. It offers coverage up to age 85 and comes with optional riders for critical illness and total and permanent disability. iTerm is particularly attractive for those who prefer a hassle-free online experience and competitive pricing, especially for basic term life coverage. It's a great option if you're comfortable managing your policy digitally.

Product Spotlight AXA Term Protector

AXA Term Protector offers robust coverage with flexible options for policy terms and sum assured. It's known for its comprehensive critical illness riders, including multi-stage critical illness coverage, which pays out at different stages of a critical illness. This can be a huge benefit, as some illnesses require ongoing treatment. AXA also provides a strong focus on customer support and claims processing. This plan is often chosen by those who prioritize extensive critical illness protection and a strong global insurer backing.

Using Term Life Insurance for Specific Scenarios in Singapore

Term life insurance isn't just a generic product; it can be tailored to fit various life stages and financial goals. Let's look at some common scenarios in Singapore.

Mortgage Protection Securing Your Home

For many Singaporeans, their HDB flat or private property is their biggest asset and liability. A term life policy can be specifically structured to cover your outstanding mortgage. If you pass away, the payout can clear your home loan, ensuring your family retains their home without financial burden. This is a very common and highly recommended use of term life insurance in Singapore.

Income Replacement Protecting Your Family's Lifestyle

If you're the primary breadwinner, your income is crucial for your family's daily expenses, education, and future plans. A term life policy can provide a lump sum that replaces your lost income for a significant period, allowing your family to maintain their lifestyle and achieve their financial goals, even in your absence. When calculating the sum assured, consider your annual income, the number of years your family would need support, and any future expenses like university fees.

Children's Education Funding Their Future

Education costs in Singapore are substantial, from primary school to university. A term life policy can be earmarked to ensure your children's education funds are secure, regardless of what happens to you. You can align the policy term with when your children are expected to complete their tertiary education.

Business Loan Protection Safeguarding Your Enterprise

If you're a business owner with outstanding business loans, a term life policy can protect your company. Should you pass away, the policy payout can be used to settle these debts, preventing your business from collapsing and protecting your partners or employees. This is often referred to as 'key person insurance' when covering a vital individual in the company.

Retirement Planning Bridging the Gap

While term life insurance isn't a retirement savings vehicle, it can play a role in your overall retirement plan. For instance, if you have dependents who will still rely on you during your early retirement years, a term policy can provide coverage until other retirement assets mature or become sufficient. It acts as a temporary bridge during a critical financial transition period.

Factors Influencing Term Life Insurance Premiums in Singapore

The cost of your term life insurance in Singapore isn't arbitrary. Several factors come into play, and understanding them can help you get the best rates.

Age The Younger The Better

This is probably the biggest factor. The younger you are when you purchase term life insurance, the lower your premiums will generally be. This is because you're considered less of a risk to the insurer. Premiums increase significantly as you age.

Health and Medical History Your Wellness Matters

Your current health status and medical history are crucial. Insurers will typically ask about pre-existing conditions, family medical history, and conduct a medical examination (for higher coverage amounts). Being in good health, with no chronic conditions, will result in lower premiums. Conditions like diabetes, high blood pressure, or a history of serious illness will likely lead to higher premiums or even policy exclusions.

Lifestyle Choices Smoking and Hobbies

Smoking is a major red flag for insurers. Smokers typically pay significantly higher premiums than non-smokers. Similarly, engaging in high-risk hobbies like skydiving, scuba diving, or competitive motorsports can also lead to increased premiums or specific exclusions in your policy.

Sum Assured How Much Coverage You Need

The higher the sum assured (the payout amount), the higher your premiums will be. It's a direct correlation. This is why a proper Financial Needs Analysis is so important – it helps you determine the right amount of coverage without overpaying.

Policy Term Duration of Coverage

Generally, a longer policy term will result in higher premiums compared to a shorter term, assuming all other factors are equal. This is because the insurer is taking on risk for a longer period.

Gender A Small Factor

In some cases, gender can play a minor role, with women sometimes paying slightly lower premiums due to longer life expectancies, though this factor is less significant than age or health.

Tips for Choosing the Best Term Life Insurance in Singapore

With so many options, how do you pick the right one? Here are some practical tips.

Assess Your Financial Needs Accurately

Don't guess! Use online calculators or work with a financial advisor to accurately determine how much coverage you need. Consider your debts, income replacement needs, future expenses (like education), and any existing savings or insurance.

Compare Quotes from Multiple Insurers

Never settle for the first quote you get. Different insurers have different underwriting guidelines and pricing structures. Get quotes from at least three to five different providers to ensure you're getting a competitive rate for the coverage you need.

Read the Fine Print Understand Exclusions

Insurance policies can be complex. Pay close attention to the terms and conditions, especially any exclusions. For example, some policies might have exclusions for certain high-risk activities or pre-existing conditions. Make sure you understand what is and isn't covered.

Consider Riders for Comprehensive Protection

While term life insurance provides a death benefit, adding riders like critical illness or total and permanent disability can offer a much more comprehensive safety net. Think about your personal risks and whether these additional protections are worth the extra premium.

Review Your Policy Regularly Life Changes

Life isn't static. Major life events like getting married, having children, buying a home, or changing jobs should prompt a review of your insurance coverage. What was sufficient five years ago might not be enough today. Aim to review your policy every few years or after any significant life change.

Seek Professional Financial Advice

A qualified financial advisor in Singapore can be an invaluable resource. They can help you conduct a thorough needs analysis, compare policies from various insurers, explain complex terms, and guide you through the application process. Their expertise can save you time and ensure you make an informed decision.

Common Misconceptions About Term Life Insurance in Singapore

Let's clear up a few common misunderstandings about term life insurance that Singaporeans often have.

Myth 1 It's Only for the Elderly

Absolutely not! Term life insurance is often most beneficial for younger individuals and families. This is when you typically have the most financial dependents (young children, a spouse) and significant debts (mortgage). Getting it young also means lower premiums.

Myth 2 It's Too Expensive

Compared to whole life insurance, term life is generally very affordable. You can get substantial coverage for a relatively low monthly premium, especially if you're healthy and young. The cost is often much less than people anticipate.

Myth 3 I Have Group Insurance So I'm Covered

While group insurance from your employer is a great benefit, it's usually not enough. Group policies often have limited coverage amounts, and they typically end if you leave your job. Personal term life insurance provides portable, comprehensive coverage that you control.

Myth 4 I'm Single So I Don't Need It

Even if you're single, you might have financial obligations like outstanding loans (student, car, personal), or you might want to leave a legacy or cover your funeral expenses without burdening your family. If you have anyone who would be financially impacted by your death, term life insurance is worth considering.

Myth 5 It's a Waste of Money If I Don't Die

Think of term life insurance like car insurance or home insurance. You hope you never have to use it, but you're glad you have it if you do. The peace of mind it provides, knowing your loved ones are protected, is invaluable. It's a financial safety net, not an investment with a guaranteed return.

The Future of Term Life Insurance in Singapore Digitalization and Innovation

The insurance industry in Singapore is constantly evolving, with technology playing a huge role. We're seeing more digitalization and innovation in how term life insurance is offered and managed.

Online Platforms and Digital Applications

Many insurers are now offering online platforms where you can get quotes, compare policies, and even apply for term life insurance digitally. This streamlines the process, making it faster and more convenient for consumers. Products like Income's iTerm are great examples of this trend.

Personalized Pricing and Wearable Tech

Some insurers are exploring personalized pricing models, potentially using data from wearable devices (with your consent, of course) to offer discounts to policyholders who maintain healthy lifestyles. While still in early stages for life insurance, this could become more prevalent.

Simplified Underwriting Processes

For certain coverage amounts, insurers are moving towards simplified underwriting, requiring fewer medical tests or questionnaires, especially for younger, healthier applicants. This speeds up the approval process significantly.

Integrated Financial Planning Tools

Expect to see more integrated platforms that combine insurance with other financial planning tools, allowing you to manage your entire financial portfolio in one place. This holistic approach helps Singaporeans make more informed decisions about their overall financial well-being.

So, there you have it – a comprehensive look at term life insurance in Singapore. It's a vital component of a sound financial plan, offering crucial protection for your loved ones. Take the time to understand your needs, explore the options available, and don't hesitate to seek expert advice. Your family's financial future is worth it!

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)