Understanding Dividends from Whole Life Insurance Policies

Learn about dividends paid by participating whole life insurance policies and how they can benefit policyholders.

Learn about dividends paid by participating whole life insurance policies and how they can benefit policyholders.

Understanding Dividends from Whole Life Insurance Policies

What Are Whole Life Insurance Dividends and How Do They Work

So, you've heard about whole life insurance, right? It's that type of policy that sticks with you for your entire life, builds cash value, and often comes with a guaranteed death benefit. But then there's this other term that pops up: dividends. What exactly are these, and how do they fit into the whole life picture? Let's break it down in a way that's easy to understand.

First off, it's super important to know that not all whole life insurance policies pay dividends. Only what we call 'participating' whole life policies do. These are typically offered by mutual insurance companies. Unlike stock companies that are owned by shareholders and aim to maximize profits for those shareholders, mutual companies are owned by their policyholders. This ownership structure is key to understanding dividends.

Think of it this way: when you buy a participating whole life policy from a mutual company, you're essentially becoming a part-owner. The company collects premiums from all its policyholders, invests that money, and pays out claims. At the end of the year, if the company has performed better than expected – maybe their investments did really well, or they had fewer claims than anticipated, or their operating expenses were lower – they end up with a surplus. Instead of keeping all that extra money as profit for external shareholders, a mutual company distributes a portion of it back to its policyholders in the form of dividends.

It's crucial to understand that these dividends aren't guaranteed. They depend on the company's financial performance. While many established mutual companies have a long history of paying dividends, and often boast about never missing a payment for decades, it's still not a contractual guarantee. The amount can fluctuate year to year based on the company's experience.

So, in essence, dividends are a return of a portion of the premium you paid, reflecting the company's favorable financial results. They're not like stock dividends, which are a share of company profits. Instead, they're more akin to a refund or a bonus that comes from the company's operational efficiency and investment success.

How Do Policyholders Receive Whole Life Insurance Dividends Exploring Payout Options

Alright, so you've got a participating whole life policy, and your insurance company has declared a dividend. That's great news! But how do you actually get that money, or rather, how can you use it? This is where the flexibility of whole life dividends really shines. Policyholders usually have several options for how they want to receive or apply their dividends. Let's dive into the most common ones:

1. Cash Payout: Direct Deposit or Check

This is the most straightforward option. You can simply choose to receive your dividend as a direct cash payment. The insurance company will either mail you a check or deposit the funds directly into your bank account. This is great if you need immediate access to the money for any reason, whether it's to cover an unexpected expense, treat yourself, or simply add to your savings. It's your money, and you can use it however you see fit.

2. Reduce Future Premiums: Lowering Your Out-of-Pocket Costs

Many policyholders opt to use their dividends to offset their upcoming premium payments. Instead of receiving the cash, the dividend amount is applied directly to reduce the next premium due. For example, if your annual premium is $2,000 and your dividend is $300, you'd only need to pay $1,700 out of pocket. This can be a fantastic way to make your whole life policy more affordable over time, especially as dividends tend to grow as your policy matures.

3. Purchase Paid-Up Additions (PUAs): Boosting Your Policy's Value

This is arguably one of the most popular and powerful ways to use whole life dividends, especially for those focused on long-term growth and maximizing their policy's benefits. When you use dividends to purchase Paid-Up Additions (PUAs), you're essentially buying small, single-premium whole life policies that immediately add to your policy's cash value and death benefit. These PUAs also generate their own dividends, creating a compounding effect. It's like a snowball rolling downhill, getting bigger and bigger. This option significantly accelerates the growth of your cash value and increases your death benefit without requiring additional underwriting.

4. Accumulate at Interest: Growing Your Money Within the Policy

With this option, your dividends are left with the insurance company to accumulate interest. The interest rate is typically declared by the insurer and can be quite competitive, often tax-deferred. This is a good choice if you don't need the cash immediately but want your dividends to continue growing within the policy, providing another layer of savings that you can access later if needed. It's a bit like a savings account, but held within your insurance policy.

5. Repay Policy Loans: Reducing Debt and Interest

If you've taken a loan against your policy's cash value, you can use your dividends to repay all or part of that loan. This is a smart move because it reduces the outstanding loan balance and the interest you're paying on it, helping to restore your policy's full cash value and death benefit more quickly.

The best option for you really depends on your personal financial goals and current needs. If you need immediate cash, take the cash. If you want to lower your ongoing expenses, reduce premiums. But if you're looking to maximize the long-term growth of your policy's cash value and death benefit, purchasing Paid-Up Additions is often the most strategic choice. It's worth discussing these options with your financial advisor to determine which one aligns best with your overall financial plan.

Tax Implications of Whole Life Insurance Dividends Understanding the Rules

When it comes to any financial product, especially one that involves growth and payouts, understanding the tax implications is crucial. Whole life insurance dividends are no exception. The good news is that, in most cases, these dividends are treated quite favorably by tax authorities, particularly in the US. Let's break down what you need to know.

Dividends as a Return of Premium: Generally Tax-Free

The primary reason whole life dividends are often tax-free is that the IRS (and similar tax bodies in other countries) generally views them as a 'return of premium.' Remember how we discussed that dividends are essentially a portion of your premium being returned to you because the company performed better than expected? Well, since you've already paid taxes on the money you used to pay your premiums, receiving a portion of it back isn't considered new income. Therefore, up to the amount of premiums you've paid into the policy, dividends are typically not taxable.

For example, if you've paid $10,000 in premiums over the years and receive a $500 dividend, that $500 is generally tax-free because it's less than your total premiums paid.

When Dividends Become Taxable: The Cost Basis Rule

There's a point, however, where dividends can become taxable. This happens if the cumulative amount of dividends you've received (or applied to your policy) exceeds the total amount of premiums you've paid into the policy. This is often referred to as your 'cost basis.' Once your dividends surpass your cost basis, any subsequent dividends are considered taxable income.

This scenario is less common in the early years of a policy but can occur with very mature policies that have accumulated significant dividends over decades. It's a good problem to have, as it means your policy has performed exceptionally well!

Tax Treatment of Different Dividend Options

- Cash Payout: As long as the total dividends received don't exceed your total premiums paid, the cash payout is tax-free.

- Reduce Future Premiums: When dividends are used to reduce premiums, they are also generally tax-free, as they are still considered a return of premium.

- Paid-Up Additions (PUAs): Dividends used to purchase PUAs are typically tax-free. The cash value growth within these PUAs is tax-deferred, meaning you don't pay taxes on the growth until you withdraw it or surrender the policy.

- Accumulate at Interest: This is where it gets a little different. While the dividend itself is tax-free (up to your cost basis), the interest earned on those accumulated dividends is typically taxable in the year it's credited to your policy, even if you don't withdraw it. This is an important distinction to remember.

Important Considerations

- Modified Endowment Contracts (MECs): If your whole life policy becomes a Modified Endowment Contract (MEC) due to overfunding, the tax treatment of withdrawals and loans, including those from dividends, changes significantly. MECs lose some of the favorable tax treatment of traditional life insurance, with withdrawals and loans being taxed on a 'last-in, first-out' (LIFO) basis, meaning gains are taxed first, and a 10% penalty may apply if you're under 59½.

- State Taxes: While federal tax rules are generally consistent, it's always wise to check with a tax professional regarding state-specific tax laws, as they can vary.

In summary, whole life insurance dividends are usually a tax-efficient way to benefit from your policy, primarily because they are treated as a return of premium. However, understanding the cost basis rule and the specific tax implications of each dividend option is key to effective financial planning. Always consult with a qualified tax advisor for personalized advice.

Comparing Whole Life Insurance Dividend Performance Top Providers and Their Offerings

When you're looking at participating whole life insurance, the dividend history and current dividend rates of different companies are a huge factor. While past performance doesn't guarantee future results, a long, consistent history of strong dividend payments is a good indicator of a company's financial strength and commitment to its policyholders. Let's look at some of the top mutual companies known for their whole life products and dividend performance, keeping in mind that specific rates and product features can change.

It's important to note that dividend rates are typically expressed as a percentage, but this isn't like an interest rate on a savings account. It's a complex calculation based on the company's investment returns, mortality experience, and expenses. A higher dividend rate generally means more money returned to policyholders.

Leading Mutual Companies Known for Dividends:

1. Northwestern Mutual

- Overview: Northwestern Mutual is consistently ranked among the top life insurance companies in the US and is renowned for its financial strength and long history of paying dividends. They have paid dividends every year since 1872.

- Product Focus: Their whole life policies are a cornerstone of their offerings, emphasizing guaranteed growth, strong cash value accumulation, and competitive dividends.

- Dividend Philosophy: They are known for a conservative investment strategy that aims for consistent, long-term returns, which translates into stable dividend payments.

- Typical Use Cases: Ideal for individuals and families seeking maximum long-term cash value growth, estate planning, and reliable financial security. Their policies are often used for wealth accumulation and tax-efficient access to cash.

- Example Scenario: A 35-year-old healthy male purchasing a $500,000 whole life policy might see initial annual premiums around $5,000-$7,000. Over time, dividends could significantly reduce out-of-pocket premiums or be used to purchase substantial Paid-Up Additions, potentially increasing the death benefit to $700,000-$800,000 and cash value to several hundred thousand by retirement age.

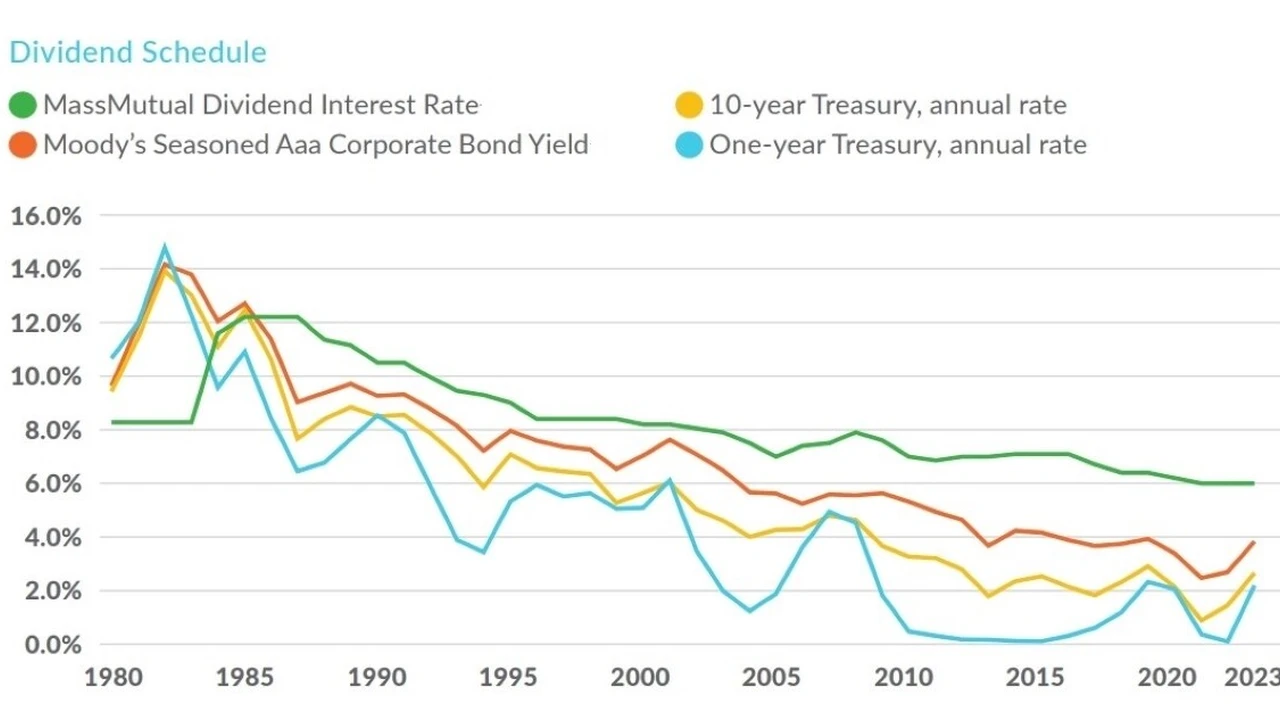

2. MassMutual (Massachusetts Mutual Life Insurance Company)

- Overview: Another giant in the mutual insurance space, MassMutual boasts a strong financial rating and a consistent dividend-paying history, dating back to 1869.

- Product Focus: They offer a range of whole life products designed for various needs, from basic protection to advanced wealth accumulation strategies.

- Dividend Philosophy: MassMutual also employs a disciplined investment approach, aiming for competitive dividends while maintaining financial stability.

- Typical Use Cases: Excellent for those prioritizing guaranteed growth, policy loans for liquidity, and estate planning. They are also popular for business planning strategies.

- Example Scenario: A 40-year-old healthy female looking for a $1,000,000 whole life policy might have annual premiums in the range of $10,000-$13,000. MassMutual's dividends could be used to accelerate cash value growth, allowing for tax-free policy loans later in life for retirement income or other large expenses.

3. Guardian Life Insurance Company of America

- Overview: Guardian is a highly respected mutual company with a long-standing tradition of paying dividends to its policyholders, consistently since 1868.

- Product Focus: Known for its robust whole life policies that emphasize strong guarantees and competitive dividend performance.

- Dividend Philosophy: Guardian focuses on a balanced approach to investments and underwriting, contributing to its consistent dividend payouts.

- Typical Use Cases: Often chosen by individuals and businesses seeking reliable, long-term financial solutions, including wealth transfer and business succession planning.

- Example Scenario: A 50-year-old healthy couple (joint policy or individual policies) planning for estate liquidity might consider a $2,000,000 whole life policy. Annual premiums could be around $25,000-$35,000. Guardian's dividends, particularly if used for PUAs, could significantly enhance the death benefit over time, ensuring sufficient funds for estate taxes or wealth transfer.

4. New York Life Insurance Company

- Overview: New York Life is one of the largest mutual life insurance companies in the US, with a dividend payment history stretching back to 1854.

- Product Focus: Offers a comprehensive suite of whole life products, known for their strong guarantees and competitive dividend scale.

- Dividend Philosophy: Their investment strategy is designed to provide long-term stability and growth, supporting consistent dividend payments.

- Typical Use Cases: Suitable for a wide range of financial goals, including retirement planning, wealth preservation, and providing a legacy.

- Example Scenario: A young family (e.g., parents in their 30s) looking for foundational protection and future savings might start with a $250,000 whole life policy for each parent, with annual premiums around $2,500-$3,500 per policy. New York Life's dividends could be reinvested to grow the cash value, providing a future resource for college funding or a down payment on a home, while also increasing the death benefit for family protection.

Important Considerations When Comparing:

- Dividend Scale Interest Rate: This is the rate the company uses in its dividend calculation. While important, it's not the only factor.

- Mortality and Expense Experience: How efficiently the company manages claims and operating costs also impacts dividends.

- Policy Design: Different whole life products from the same company might have varying dividend performance based on their specific design and guarantees.

- Illustrations: Always ask for an illustration that shows both guaranteed and non-guaranteed (dividend-based) values. Understand that the non-guaranteed values are projections and not promises.

- Financial Strength Ratings: Look at ratings from agencies like A.M. Best, S&P, Moody's, and Fitch. Strong ratings indicate a company's ability to meet its financial obligations, including dividend payments.

When comparing, it's not just about the highest dividend rate today, but the company's overall financial stability, its long-term track record, and how its products align with your specific financial objectives. Working with an experienced financial advisor who understands these nuances is invaluable.

Maximizing Your Whole Life Policy Dividends Strategies for Growth

So, you've got a participating whole life policy, and you understand how dividends work. Now, how can you make the most of them? There are several strategies you can employ to maximize the benefits of your dividends, primarily focusing on accelerating your policy's cash value and death benefit growth. Let's explore some of the most effective approaches.

1. Reinvesting Dividends into Paid-Up Additions (PUAs): The Power of Compounding

As we touched upon earlier, using your dividends to purchase Paid-Up Additions (PUAs) is often considered the most powerful strategy for maximizing your policy's long-term value. Here's why it's so effective:

- Immediate Cash Value Growth: Each PUA you purchase immediately adds to your policy's cash value. Unlike your base policy, which builds cash value more slowly in the early years, PUAs contribute directly and significantly.

- Increased Death Benefit: Along with cash value, PUAs also increase your policy's death benefit. This means more protection for your loved ones without having to go through additional underwriting for the PUA portion.

- Generates Its Own Dividends: This is the magic of compounding. The PUAs themselves are participating and generate their own dividends. This creates a snowball effect, where your policy's growth accelerates over time. The more PUAs you buy, the more dividends they generate, which in turn can buy more PUAs, and so on.

- Tax-Advantaged Growth: The cash value growth within PUAs is tax-deferred, meaning you don't pay taxes on the gains until you withdraw them or surrender the policy.

Scenario Example: Imagine a policyholder who consistently uses their $500 annual dividend to buy PUAs. In the first year, that $500 buys a small amount of additional death benefit and cash value. In subsequent years, not only does the original policy pay a dividend, but the PUAs purchased in previous years also start generating their own dividends. This can lead to significantly higher cash values and death benefits than if the dividends were taken as cash or used to reduce premiums.

2. Overfunding with a Paid-Up Additions Rider: Supercharging Your Policy

Beyond just using your regular dividends for PUAs, many whole life policies allow you to add a Paid-Up Additions (PUA) rider. This rider enables you to pay additional, optional premiums directly into the PUA component of your policy. This is essentially a way to 'overfund' your policy in a tax-efficient manner, accelerating cash value growth even further.

- Faster Cash Value Accumulation: By contributing extra funds to the PUA rider, you rapidly increase your policy's cash value, making it a more robust savings vehicle.

- Enhanced Liquidity: A larger cash value means more money available for policy loans, which can be accessed tax-free (as long as the policy isn't a MEC and the loan is repaid).

- Increased Internal Rate of Return (IRR): Strategically overfunding with a PUA rider can improve the overall internal rate of return of your whole life policy, making it a more competitive financial asset.

Important Note: Be careful not to overfund your policy to the point where it becomes a Modified Endowment Contract (MEC). A MEC loses some of the favorable tax treatment of life insurance, particularly regarding withdrawals and loans. Your insurance agent or financial advisor can help you stay within the IRS guidelines to avoid MEC status.

3. Maintaining Your Policy for the Long Term: Time is Your Ally

Whole life insurance, and especially its dividend component, is designed for the long haul. The power of compounding truly shines over decades. The longer you hold your policy and allow dividends to be reinvested (especially into PUAs), the more significant the growth will be.

- Exponential Growth: Cash value and dividend growth tend to be slower in the early years but accelerate significantly in later years due to compounding.

- Increased Dividend Payouts: As your policy matures and its cash value grows, the dividend payouts themselves tend to increase, further fueling the compounding effect.

4. Regular Policy Reviews: Adapting to Changing Needs

While not directly a strategy for maximizing dividends, regularly reviewing your policy with your financial advisor is crucial. This ensures that your dividend option (cash, premium reduction, PUAs, etc.) still aligns with your current financial goals and life circumstances. For instance, if you initially chose to reduce premiums but now have surplus income, switching to PUAs might be a better strategy for long-term wealth building.

By strategically utilizing your whole life insurance dividends, particularly through the purchase of Paid-Up Additions and careful overfunding, you can transform your policy into a powerful financial tool for wealth accumulation, liquidity, and enhanced protection for your loved ones.

Case Studies and Real-World Applications of Whole Life Dividends

Understanding the theory behind whole life dividends is one thing, but seeing how they play out in real-world scenarios can really bring their value to life. Let's look at a few hypothetical case studies that illustrate how different individuals and families might leverage dividends to achieve their financial goals.

Case Study 1: The Young Professional Building Long-Term Wealth

- Client Profile: Sarah, a 30-year-old marketing manager, single, no dependents yet, earning a good income. She's already contributing to her 401(k) but wants another tax-advantaged savings vehicle that offers guarantees and liquidity.

- Policy Choice: Sarah purchases a $500,000 participating whole life policy from Northwestern Mutual with an annual premium of $4,500. She also adds a PUA rider and initially contributes an extra $2,000 annually to it.

- Dividend Strategy: Sarah chooses to use all her dividends to purchase Paid-Up Additions (PUAs).

- Outcome:

- Year 10: Sarah's policy has accumulated significant cash value, largely due to the PUAs and reinvested dividends. She decides to take a tax-free policy loan of $30,000 to help with a down payment on her first home. Her death benefit has also grown to approximately $650,000.

- Year 30 (Age 60): Sarah is nearing retirement. Her policy's cash value has grown substantially, now over $300,000, and her death benefit is well over $1,000,000. She begins taking tax-free income streams from her policy's cash value (via loans and withdrawals) to supplement her retirement income, without impacting her 401(k) or other investments. The remaining death benefit provides a legacy for her future family.

- Key Takeaway: By consistently reinvesting dividends into PUAs and utilizing the PUA rider, Sarah maximized her policy's cash value growth, providing a flexible source of funds for major life events and retirement, all while maintaining a growing death benefit.

Case Study 2: The Family Protecting Their Future and Managing Premiums

- Client Profile: David and Maria, both 40, with two young children. They want strong life insurance protection but are also mindful of their budget. They have a mortgage and other family expenses.

- Policy Choice: Each purchases a $750,000 participating whole life policy from MassMutual, with combined annual premiums of $15,000.

- Dividend Strategy: For the first 10 years, they choose to use their dividends to reduce their annual premiums, making the policies more affordable during a period of high expenses. After 10 years, as their income increases and children are older, they switch to using dividends to purchase PUAs.

- Outcome:

- Years 1-10: Dividends effectively lower their out-of-pocket premium payments by an average of 10-15% each year, freeing up cash flow for other family needs.

- Year 20 (Age 60): With 10 years of PUA reinvestment, their policies' cash values have grown significantly. David faces an unexpected medical expense not fully covered by health insurance. He takes a tax-free policy loan of $50,000 from his policy's cash value to cover the costs, avoiding dipping into their retirement savings. Their combined death benefit has also increased to over $1,800,000.

- Key Takeaway: Dividends offer flexibility. Initially using them to reduce premiums helped manage their budget, and later switching to PUAs allowed them to build substantial cash value for emergencies and increased their family's protection.

Case Study 3: The Business Owner Planning for Succession

- Client Profile: John, 55, owner of a successful manufacturing business. He wants to ensure his business can continue smoothly if something happens to him, and also provide for his family.

- Policy Choice: John purchases a $3,000,000 participating whole life policy from Guardian, with an annual premium of $40,000. The policy is structured to be owned by an Irrevocable Life Insurance Trust (ILIT) for estate tax efficiency.

- Dividend Strategy: John consistently uses his dividends to purchase Paid-Up Additions (PUAs).

- Outcome:

- Year 15 (Age 70): John decides to retire and sell his business. The policy's cash value, significantly boosted by PUAs and dividends, has grown to over $1,200,000. He uses a portion of this cash value (via tax-free loans) to supplement his retirement income and provide additional liquidity. The death benefit has grown to over $4,500,000, ensuring his family and estate have ample funds to cover potential estate taxes and provide a substantial inheritance, outside of his business assets.

- Key Takeaway: For business owners, whole life dividends, especially when reinvested into PUAs, can create a powerful, liquid asset that can be used for business succession, retirement income, and estate planning, providing a guaranteed and growing financial resource independent of business fluctuations.

These case studies highlight the versatility of whole life insurance dividends. Whether you're a young individual building wealth, a family managing expenses and protection, or a business owner planning for the future, understanding and strategically utilizing dividends can significantly enhance the value and utility of your whole life policy.

Common Misconceptions About Whole Life Insurance Dividends Clarifying the Facts

Whole life insurance, and particularly its dividend component, can sometimes be misunderstood. There are several common misconceptions that can lead to confusion or prevent people from fully appreciating the benefits of participating policies. Let's clear up some of these myths.

Misconception 1: Dividends are Guaranteed

- The Myth: Many people mistakenly believe that if a company pays dividends, they are guaranteed to receive them every year, and the amount will always be the same or increase.

- The Reality: As discussed earlier, dividends are NOT guaranteed. They are declared annually by the insurance company's board of directors and depend on the company's financial performance (investment returns, mortality experience, and operating expenses). While many mutual companies have a long history of consistent dividend payments, and often boast about never missing a payment for over a century, the amount can fluctuate year to year. It's a non-guaranteed feature, albeit a highly reliable one for financially strong mutual companies.

Misconception 2: Dividends are Taxable Income Like Stock Dividends

- The Myth: Because they're called 'dividends,' people often assume they are taxed in the same way as stock dividends, which are typically taxable income.

- The Reality: In most cases, whole life insurance dividends are considered a 'return of premium' by the IRS (and similar tax authorities). This means they are generally tax-free up to the amount of premiums you've paid into the policy. Only if the cumulative dividends received exceed your total premiums paid do they become taxable. This is a significant tax advantage compared to many other investment vehicles. The only exception is usually the interest earned on dividends left to accumulate at interest, which is typically taxable annually.

Misconception 3: Dividends are the Only Source of Growth in Whole Life Policies

- The Myth: Some believe that if a policy doesn't pay dividends, it won't grow, or that dividends are the sole driver of cash value growth.

- The Reality: Whole life policies have guaranteed cash value growth built into the contract, regardless of dividends. This guaranteed growth is based on a contractual interest rate. Dividends, when paid, provide an additional, non-guaranteed layer of growth on top of these guarantees. They accelerate the cash value accumulation and death benefit increase, but they are not the only source of growth.

Misconception 4: You Have to Take Dividends as Cash

- The Myth: Some policyholders might think their only option is to receive dividends as a cash payout.

- The Reality: As we've explored, policyholders have several flexible options for how to use their dividends: taking them as cash, using them to reduce premiums, letting them accumulate at interest, or, most powerfully, using them to purchase Paid-Up Additions (PUAs). The ability to choose how to apply dividends allows policyholders to tailor the policy's benefits to their evolving financial needs.

Misconception 5: Dividends are Only for the Wealthy

- The Myth: Whole life insurance, and by extension its dividends, is sometimes perceived as a product exclusively for high-net-worth individuals.

- The Reality: While whole life insurance can be a powerful tool for wealth management and estate planning for the affluent, it also serves as a foundational financial product for middle-income families. The guaranteed death benefit provides essential protection, and the cash value, enhanced by dividends, can be a reliable savings component for anyone looking for long-term financial security, liquidity, and tax advantages. The ability to use dividends to reduce premiums can even make policies more accessible over time.

Misconception 6: Dividends are Just a Marketing Gimmick

- The Myth: Some skeptics might view dividends as a way for insurance companies to make their policies seem more attractive without delivering real value.

- The Reality: For mutual insurance companies, dividends are a fundamental part of their business model and a direct reflection of their financial strength and efficiency. They represent a return of surplus to the policyholders who own the company. For many policyholders, especially those who choose to reinvest them, dividends significantly enhance the long-term value and performance of their whole life policies, making them a tangible and valuable benefit.

By understanding these clarifications, you can approach whole life insurance with a more informed perspective and make better decisions about how it fits into your overall financial strategy.

The Future of Whole Life Dividends and Policyholder Benefits

The landscape of financial products is always evolving, and whole life insurance is no exception. While the core principles of whole life – guaranteed death benefit, guaranteed cash value growth, and the potential for dividends – remain steadfast, it's worth considering what the future might hold for dividends and how they continue to benefit policyholders in an ever-changing economic environment.

Continued Relevance in a Low-Interest Rate Environment

For many years, we've seen a global trend of relatively low interest rates. This can impact the investment returns of insurance companies, which in turn can affect dividend scales. However, mutual companies with diversified, long-term investment strategies are often well-positioned to navigate these environments. Their conservative approach, focusing on stability rather than aggressive short-term gains, helps them maintain consistent performance. As such, whole life dividends are likely to remain a valuable component, offering a stable, albeit non-guaranteed, return that can be attractive when other guaranteed options yield very little.

Enhanced Focus on Policyholder Value

In a competitive market, mutual companies have a strong incentive to continue delivering value to their policyholders, as policyholders are their owners. This means a continued focus on efficient operations, prudent investment management, and strong underwriting practices, all of which contribute to the ability to pay dividends. The emphasis on policyholder benefits, including dividends, is a core differentiator for mutual whole life insurance.

Technological Advancements and Transparency

As technology advances, we might see even greater transparency and easier access to information regarding dividend performance and policy values. Digital platforms could make it simpler for policyholders to track their policy's growth, understand the impact of their dividend choices, and even adjust their dividend options with greater ease. This increased transparency can empower policyholders to make more informed decisions about their policies.

Integration with Broader Financial Planning

Whole life insurance, with its dividend-enhanced cash value, is increasingly being recognized as a versatile tool within a comprehensive financial plan. In the future, we might see even more sophisticated strategies for integrating whole life policies into retirement income planning, business succession, and wealth transfer, with dividends playing a crucial role in accelerating the growth and utility of these policies. Financial advisors are becoming more adept at illustrating how dividends can contribute to long-term financial goals, beyond just the death benefit.

Resilience Against Market Volatility

One of the enduring appeals of whole life insurance, particularly its guaranteed components and dividend potential, is its resilience during periods of market volatility. While other investments might fluctuate wildly, the cash value of a whole life policy continues to grow, and dividends, while not guaranteed, often provide a stable return. This characteristic is likely to remain highly valued, especially for those seeking a safe harbor within their financial portfolio.

The Role of Paid-Up Additions (PUAs)

The strategy of using dividends to purchase Paid-Up Additions (PUAs) is likely to continue to be a cornerstone for maximizing policyholder benefits. As policyholders become more financially savvy, the power of compounding through PUAs will remain a key driver for accelerating cash value and death benefit growth, making whole life policies even more attractive as a long-term savings and protection vehicle.

In essence, the future of whole life dividends looks promising for policyholders. While economic conditions and company performance will always play a role, the fundamental structure of mutual whole life insurance, combined with strategic dividend utilization, positions it as a robust and adaptable financial asset for generations to come. It continues to offer a unique blend of protection, guaranteed growth, and the potential for additional returns that can significantly enhance a policyholder's financial well-being.

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)