Variable Universal Life Insurance Understanding the Risks

An in-depth look at variable universal life insurance, its investment component, and associated market risks.

An in-depth look at variable universal life insurance, its investment component, and associated market risks.

Hey there! So, you've been hearing about Variable Universal Life (VUL) insurance, and it sounds pretty intriguing, right? It's often pitched as a life insurance policy that can also help you grow your wealth through investments. But like anything that promises both protection and potential growth, there's a lot to unpack. This isn't your grandma's whole life policy; VUL comes with a unique set of features, benefits, and, crucially, risks that you absolutely need to understand before diving in. Let's break it down, piece by piece, so you can make an informed decision about whether VUL is the right fit for your financial journey.

H2 What is Variable Universal Life Insurance VUL Basics

At its core, Variable Universal Life insurance is a type of permanent life insurance. This means it's designed to last your entire life, as long as premiums are paid. It has two main components: a death benefit and a cash value component. The death benefit is the amount paid to your beneficiaries when you pass away. The cash value is a savings or investment component that grows over time and can be accessed during your lifetime. What makes VUL 'variable' and 'universal' is where things get interesting.

The 'universal' part means it offers flexibility. Unlike traditional whole life insurance with fixed premiums, VUL allows you to adjust your premium payments and even your death benefit amount within certain limits. If you have a good year financially, you might pay more to boost your cash value. If things are tight, you might pay less, or even skip a payment, as long as your cash value can cover the policy's costs. This flexibility can be a huge plus for people whose incomes fluctuate or who want more control over their policy.

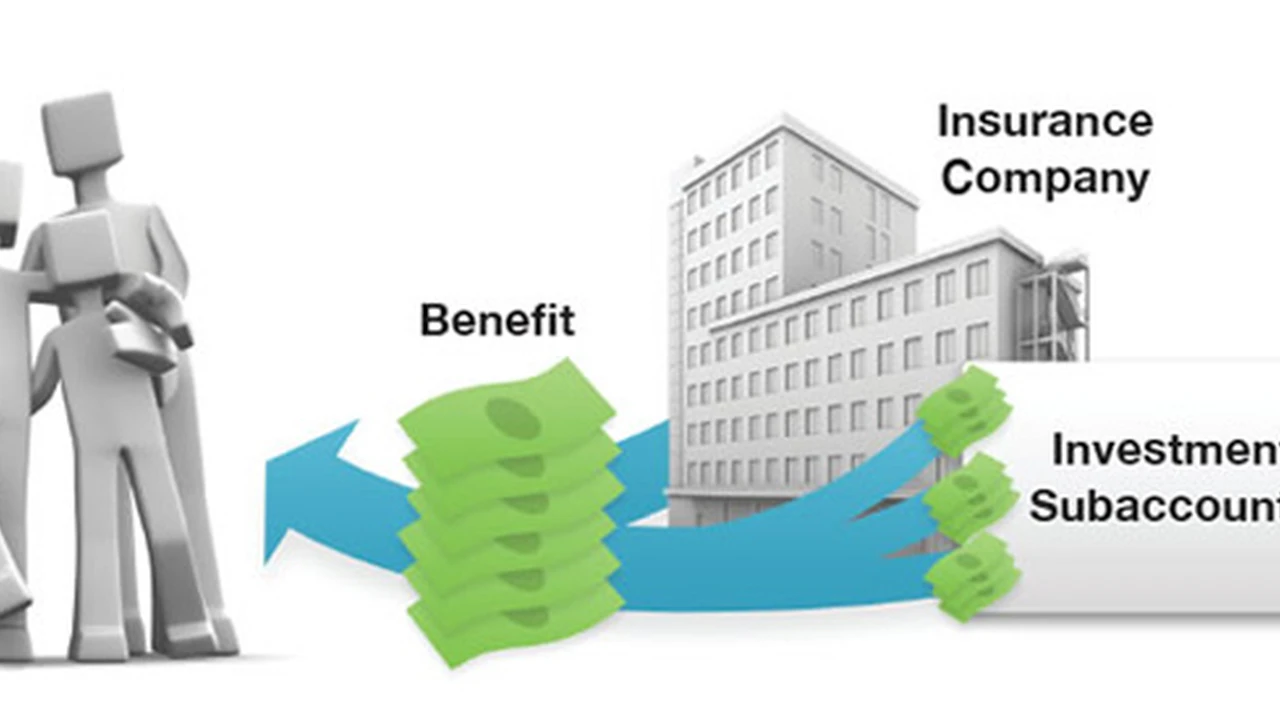

Now, the 'variable' aspect is where the investment component comes into play, and it's also where the primary risks lie. With VUL, the cash value is invested in sub-accounts, which are similar to mutual funds. You, the policyholder, get to choose how your cash value is allocated among these sub-accounts. These can include stock funds, bond funds, money market funds, and more. The performance of these sub-accounts directly impacts your cash value. If your chosen investments perform well, your cash value grows. If they perform poorly, your cash value can decrease, and in some cases, even disappear, potentially causing your policy to lapse.

H2 How VUL Differs from Other Life Insurance Types VUL vs Whole Life vs Indexed Universal Life

To truly grasp VUL, it's helpful to compare it to its cousins in the permanent life insurance family:

H3 VUL vs Whole Life Insurance

Whole life insurance offers guaranteed growth of its cash value and a guaranteed death benefit. Premiums are typically fixed. You don't choose investments; the insurer manages them, and you receive a guaranteed interest rate (and sometimes dividends). This predictability is great for risk-averse individuals. VUL, on the other hand, offers potential for higher cash value growth due to its investment component, but with that comes market risk. Your cash value and even your death benefit (if it's not guaranteed) can fluctuate.

H3 VUL vs Indexed Universal Life IUL Insurance

IUL also offers flexible premiums and a cash value component tied to a market index (like the S&P 500), but it doesn't directly invest in the market. Instead, its growth is linked to the index's performance, usually with a cap on gains and a floor (often 0%) to protect against losses. This offers a middle ground: more growth potential than whole life, but less risk and less direct market exposure than VUL. With VUL, you're directly invested in sub-accounts, meaning you can experience both uncapped gains and uncapped losses.

H2 The Investment Component of VUL Understanding Sub Accounts and Market Exposure

The investment component is the defining characteristic of VUL. When you pay your premiums, a portion goes towards covering the cost of insurance (COI), administrative fees, and other charges. The remainder is allocated to the sub-accounts you've selected. These sub-accounts are professionally managed portfolios, similar to mutual funds, and they invest in various asset classes like stocks, bonds, and money market instruments.

You typically have a wide range of sub-account options to choose from, allowing you to tailor your investment strategy to your risk tolerance and financial goals. For example, you might choose aggressive growth funds if you're comfortable with higher risk for potentially higher returns, or more conservative bond funds if you prioritize stability. This direct control over investments is a major draw for many, but it also means you bear the investment risk.

The performance of these sub-accounts directly impacts your cash value. If the market performs well, your cash value can grow significantly, potentially increasing your death benefit (if you choose an option that allows for this) or providing a larger pool of money you can access. Conversely, if the market declines, your cash value will also decrease. This is the core risk: you could lose money in your cash value, and if it drops too low, it might not be enough to cover the policy's fees, leading to a policy lapse.

H2 The Risks Associated with Variable Universal Life Insurance VUL Drawbacks

While VUL offers exciting potential, it's crucial to be aware of its inherent risks:

H3 Market Risk and Cash Value Fluctuations

This is the biggest one. Since your cash value is directly invested in the market, it's subject to market volatility. There's no guarantee of returns, and you could lose a significant portion, or even all, of your cash value if your investments perform poorly. This can be particularly problematic if you're relying on the cash value for future income or to cover policy costs.

H3 Policy Lapse Risk

If your cash value declines due to poor investment performance and isn't sufficient to cover the policy's ongoing charges (cost of insurance, administrative fees, etc.), your policy could lapse. This means you'd lose your coverage and any accumulated cash value. To prevent this, you might need to pay higher premiums than initially planned, especially during market downturns.

H3 High Fees and Charges

VUL policies often come with a complex structure of fees and charges that can eat into your returns. These can include:

- Mortality and Expense (M&E) Charges: These cover the cost of insurance and administrative expenses.

- Investment Management Fees: Fees charged by the sub-account managers.

- Administrative Fees: For policy maintenance.

- Surrender Charges: If you cancel the policy in its early years, you'll likely pay a significant fee.

- Rider Fees: If you add optional benefits to your policy.

These fees can be substantial and can significantly impact the growth of your cash value, especially in the early years of the policy.

H3 Complexity and Management Responsibility

VUL policies are more complex than other types of life insurance. You need to actively manage your sub-account allocations, monitor market performance, and understand how fees impact your policy. This requires a certain level of financial literacy and ongoing engagement. If you're not comfortable with this level of involvement, VUL might not be the best choice.

H3 Potential for Lower Death Benefit

While some VUL policies offer an increasing death benefit option (where the death benefit equals the initial face amount plus the cash value), others might have a level death benefit. If your cash value declines significantly, and you have a level death benefit, the policy's internal costs might increase, potentially requiring higher premiums to maintain the coverage.

H2 Who is Variable Universal Life Insurance Best Suited For Ideal Candidates

Given its unique characteristics, VUL isn't for everyone. It's generally best suited for individuals who:

- Have a high risk tolerance: You need to be comfortable with the possibility of losing money in your cash value due to market fluctuations.

- Are financially savvy and engaged: You should be willing and able to actively manage your investment sub-accounts and monitor your policy's performance.

- Have a long-term time horizon: VUL policies are designed for the long haul. The longer you hold the policy, the more time your investments have to recover from market downturns and potentially grow.

- Have maximized other tax-advantaged investment vehicles: If you've already maxed out contributions to 401(k)s, IRAs, and other tax-advantaged accounts, VUL can offer another avenue for tax-deferred growth.

- Seek flexible premiums and death benefit options: If your income or financial needs might change over time, the flexibility of VUL can be appealing.

- Are looking for a combination of life insurance protection and investment potential: You want the security of a death benefit but also the opportunity for wealth accumulation.

H2 Specific VUL Products and Providers A Comparative Look

When considering VUL, it's important to look at specific products and providers, as features, fees, and sub-account options can vary significantly. Here are a few examples of major players in the VUL market, along with general characteristics you might find:

H3 Northwestern Mutual VUL

- General Features: Northwestern Mutual is known for its financial strength and a wide array of investment options. Their VUL products typically offer a diverse selection of sub-accounts managed by various reputable investment firms. They often emphasize personalized financial planning.

- Use Case: Ideal for individuals seeking a strong, established insurer with a broad range of investment choices and who value comprehensive financial advice.

- Comparison Point: Often seen as a more traditional, advice-driven approach to VUL, potentially with higher service levels but also potentially higher fees.

- Pricing: Varies widely based on age, health, death benefit, and investment choices. Expect competitive but not necessarily the lowest premiums due to their service model.

H3 Pacific Life VUL

- General Features: Pacific Life is known for its innovative product designs and competitive pricing. Their VUL offerings often include a good selection of sub-accounts and may feature more modern policy designs with various riders for added flexibility (e.g., long-term care riders).

- Use Case: Suitable for those looking for a balance of strong investment options and potentially more flexible policy features, often appealing to those who are comfortable with a more self-directed investment approach within the policy.

- Comparison Point: Often compared to other large insurers, Pacific Life aims to offer a strong value proposition with a good blend of features and cost-effectiveness.

- Pricing: Generally competitive, with options to customize the policy to manage premium costs.

H3 Lincoln Financial Group VUL

- General Features: Lincoln Financial offers a robust suite of VUL products, often with a focus on diverse investment platforms and tools. They might provide access to a wide range of proprietary and third-party sub-accounts, catering to various investment philosophies.

- Use Case: Excellent for investors who want extensive control over their sub-account allocations and access to a broad spectrum of investment choices. Good for those who are actively involved in managing their investment portfolio.

- Comparison Point: Known for its strong investment platform, making it a good choice for those prioritizing the investment aspect of VUL.

- Pricing: Can be competitive, but the overall cost will depend heavily on the chosen sub-accounts and their associated management fees.

H3 AXA Equitable VUL (now Equitable Holdings)

- General Features: Equitable has a long history in the variable products market. Their VUL policies typically offer a wide selection of investment options, including specialized funds. They often focus on providing tools and resources for policyholders to manage their investments effectively.

- Use Case: Appealing to individuals who appreciate a wide range of investment choices and potentially more sophisticated investment strategies within their VUL policy.

- Comparison Point: Often seen as a strong contender for those who prioritize the investment growth potential and are comfortable with active management.

- Pricing: Varies, but generally aligns with other major VUL providers, with fees tied to the complexity of the investment options.

H3 Prudential VUL

- General Features: Prudential offers VUL products that often emphasize strong guarantees on the death benefit, even while the cash value is variable. They typically provide a solid selection of sub-accounts and may have features designed to help manage market risk.

- Use Case: Good for individuals who want the investment potential of VUL but also value the security of a strong, reliable insurer and potentially some built-in risk management features.

- Comparison Point: Often highlights its financial strength and ability to provide long-term security, even with the variable component.

- Pricing: Competitive, with options to balance investment risk and premium stability.

Important Note on Pricing: It's impossible to give exact 'prices' for VUL policies here because they are highly individualized. Premiums depend on factors like your age, health, gender, desired death benefit, chosen riders, and the specific investment allocations. The cost of insurance (COI) also increases with age. Always get personalized quotes from a qualified financial advisor.

H2 Accessing Your Cash Value How to Use VUL for Financial Needs

One of the attractive features of permanent life insurance, including VUL, is the ability to access your cash value during your lifetime. There are generally three ways to do this:

H3 Policy Loans

You can borrow against your cash value. The loan is not taxable, and you don't have to pay it back on a strict schedule, though interest will accrue. If you die with an outstanding loan, the death benefit paid to your beneficiaries will be reduced by the loan amount plus any accrued interest. The cash value continues to be invested, but the portion used as collateral for the loan may earn a lower interest rate or be subject to different investment rules.

H3 Withdrawals

You can withdraw money directly from your cash value. Withdrawals are generally tax-free up to your 'cost basis' (the total amount of premiums you've paid into the policy). Any withdrawals above your cost basis are typically taxed as ordinary income. Withdrawals reduce both your cash value and your death benefit.

H3 Surrender the Policy

You can surrender (cancel) the policy and receive the cash surrender value, which is your cash value minus any surrender charges and outstanding loans. If the cash surrender value is greater than your cost basis, the difference will be taxed as ordinary income. This option means you lose your life insurance coverage.

It's crucial to understand that accessing your cash value, especially through withdrawals or loans, can impact the long-term performance and even the solvency of your policy. Always consult with a financial advisor before making these decisions.

H2 Tax Implications of Variable Universal Life Insurance VUL and Taxes

VUL policies offer some attractive tax advantages:

- Tax-Deferred Cash Value Growth: The earnings within your sub-accounts grow on a tax-deferred basis. You don't pay taxes on these gains until you withdraw them or surrender the policy.

- Tax-Free Death Benefit: The death benefit paid to your beneficiaries is generally income tax-free.

- Tax-Free Policy Loans: As mentioned, loans taken against your cash value are typically tax-free, as long as the policy remains in force.

However, there are important considerations:

- Modified Endowment Contract (MEC): If your policy is 'overfunded' (you pay too much premium too quickly), it can be classified as a Modified Endowment Contract (MEC). MECs lose some of the tax advantages, particularly regarding policy loans and withdrawals, which become subject to 'last-in, first-out' (LIFO) taxation and potential penalties if taken before age 59½.

- Withdrawals: While withdrawals up to your cost basis are tax-free, anything above that is taxable as ordinary income.

- Surrender: If you surrender the policy and the cash value exceeds your cost basis, the gain is taxable.

Always work with a qualified tax advisor to understand the specific tax implications for your situation.

H2 Making an Informed Decision Is VUL Right for You

Deciding on VUL requires careful consideration of your financial goals, risk tolerance, and willingness to be actively involved in managing your policy. Here's a quick checklist to help you think it through:

- Do you need permanent life insurance? If your need for coverage is temporary, term life insurance is likely a more cost-effective solution.

- Are you comfortable with market risk? Can you handle the possibility of your cash value decreasing due to investment performance?

- Are you willing to actively manage your investments? VUL isn't a 'set it and forget it' product.

- Have you maximized other tax-advantaged savings? If not, consider 401(k)s, IRAs, and HSAs first.

- Do you understand the fees and charges? Make sure you get a clear breakdown of all costs.

- Do you have a long-term financial plan? VUL works best as part of a comprehensive, long-term strategy.

If you're looking for a life insurance policy that offers lifelong coverage, flexible premiums, and the potential for significant cash value growth through market-linked investments, and you're comfortable with the associated risks and management responsibilities, VUL could be a powerful tool in your financial arsenal. However, if you prefer guarantees, simplicity, or are risk-averse, other permanent life insurance options like whole life or indexed universal life might be a better fit. Always consult with a trusted, independent financial advisor who can assess your individual circumstances and help you navigate the complexities of VUL to determine if it aligns with your overall financial strategy.

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)