Indexed Universal Life Insurance Explained Its Potential

Learn about indexed universal life insurance, how its cash value grows, and its potential for market-linked returns.

Learn about indexed universal life insurance, how its cash value grows, and its potential for market-linked returns.

Indexed Universal Life Insurance Explained Its Potential

Hey there! So, you've heard about life insurance, right? Probably the basic stuff like term life or whole life. But then there's this other type that sounds a bit more complex, a bit more intriguing: Indexed Universal Life (IUL) insurance. Don't let the fancy name scare you off. It's actually a pretty cool financial tool that combines the death benefit of traditional life insurance with a cash value component that can grow based on a market index, without directly investing in the stock market. Sounds like a sweet spot between security and growth, doesn't it? Let's dive in and break down what IUL is, how it works, and why it might be a smart move for your financial future, especially if you're looking for both protection and potential wealth accumulation.

What is Indexed Universal Life Insurance Understanding IUL Basics

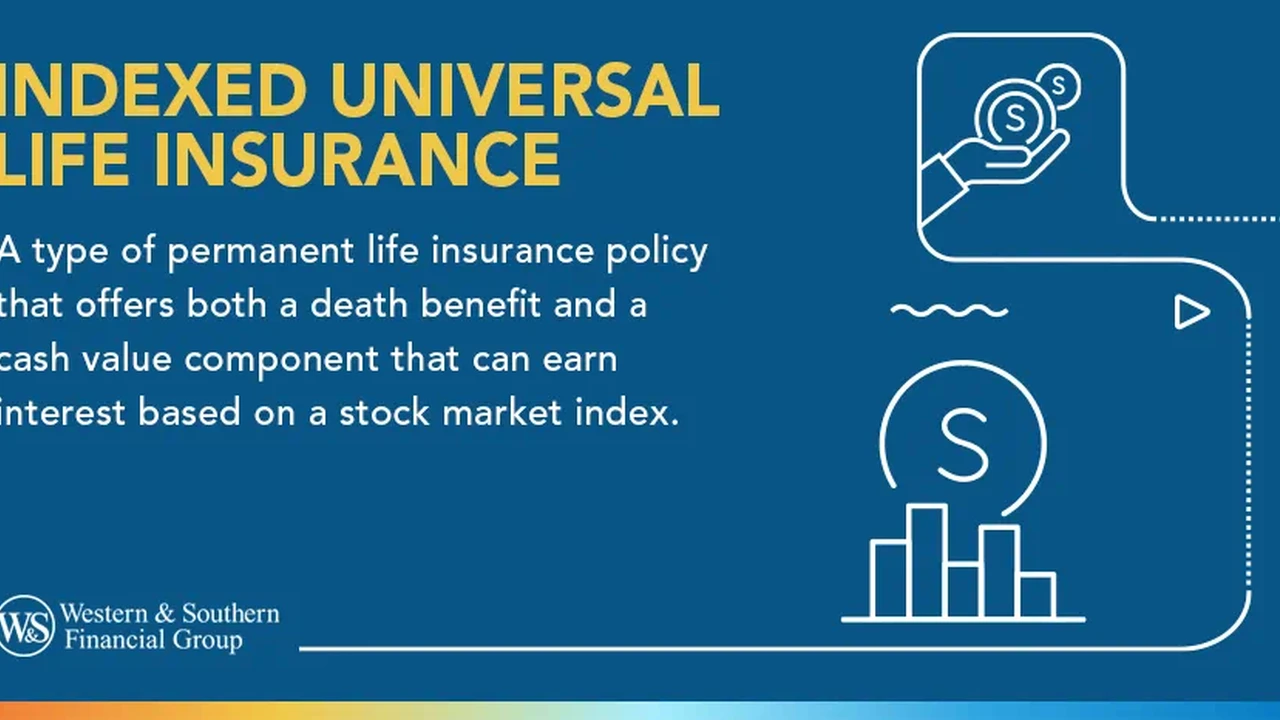

At its core, Indexed Universal Life insurance is a type of permanent life insurance. This means it's designed to last your entire life, as long as you pay the premiums. Unlike term life, which expires after a set period, IUL offers lifelong coverage. But here's where it gets interesting: it has a cash value component that grows over time. This cash value isn't just sitting there; it's linked to the performance of a specific market index, like the S&P 500 or the NASDAQ 100. The cool part? You get to participate in some of the market's upside potential without directly investing in stocks, which also means you're protected from market downturns. How? Well, IUL policies typically have a 'floor' – a guaranteed minimum interest rate, often 0% or 1%. So, if the market index performs poorly, your cash value won't lose money due to market fluctuations. On the flip side, there's usually a 'cap' – a maximum interest rate you can earn. This cap limits your upside, but it's the trade-off for that downside protection. Think of it as a balanced approach: you get some of the market's gains, but you're shielded from its losses. This makes IUL a pretty attractive option for those who want growth potential but are also risk-averse.

How IUL Cash Value Grows Exploring Index Linking and Protection

The cash value growth in an IUL policy is what really sets it apart. Instead of earning a fixed interest rate (like in whole life) or directly investing in sub-accounts (like in variable universal life), your cash value growth is tied to a market index. Let's say your policy is linked to the S&P 500. The insurance company doesn't actually invest your money directly into the S&P 500. Instead, they use a portion of your premium to buy options on the index. This strategy allows them to credit interest to your cash value based on the index's performance, up to a certain cap, and ensures that your cash value won't drop below the floor, even if the index tanks. This protection from market losses is a huge selling point for many people. Imagine the stock market crashing, but your IUL cash value remains stable or continues to grow at its guaranteed minimum. That's a pretty comforting thought, right? The growth is also tax-deferred, meaning you don't pay taxes on the gains until you withdraw or borrow from the cash value. This tax-advantaged growth can be a powerful tool for long-term wealth accumulation.

Key Features and Benefits of Indexed Universal Life Insurance Flexibility and Tax Advantages

IUL policies come with a bunch of features that make them super flexible and appealing. First off, you have flexibility with your premiums. Unlike whole life, where premiums are usually fixed, with IUL, you can often adjust your premium payments within certain limits. If you have a good year financially, you might pay more to boost your cash value. If things are tight, you might pay less, as long as there's enough cash value to cover the policy's costs. This flexibility is a big plus for people whose income might fluctuate. Another major benefit is the ability to access your cash value. You can take out loans or withdrawals from your cash value, often tax-free, as long as the policy remains in force. This can be a fantastic resource for things like supplementing retirement income, paying for a child's education, or even covering unexpected emergencies. The death benefit is also adjustable, meaning you can increase or decrease it over time to match your changing needs. Plus, the death benefit is generally paid out tax-free to your beneficiaries, providing a significant financial safety net for your loved ones. These combined features make IUL a versatile tool for both protection and financial planning.

Indexed Universal Life Insurance for Retirement Planning A Smart Strategy

Many people are turning to IUL as a component of their retirement planning strategy, and for good reason. The tax-deferred growth of the cash value, coupled with the ability to access it tax-free through policy loans, makes it an attractive option for creating a supplemental income stream in retirement. Imagine having a source of income that isn't subject to market volatility and can be accessed without immediate tax consequences. That's the power of IUL. It can complement your 401(k)s and IRAs, providing diversification and an additional layer of financial security. Plus, if you live a long, healthy life, the cash value can continue to grow, providing a substantial resource. And if you pass away prematurely, your beneficiaries receive a tax-free death benefit, ensuring your family's financial well-being. It's like having a financial safety net that also has the potential to grow your wealth for your golden years.

Comparing IUL with Other Life Insurance Types Making the Right Choice

So, how does IUL stack up against other types of life insurance? Let's do a quick comparison:

IUL vs Term Life Insurance Flexibility and Cash Value

Term life is straightforward: it covers you for a specific period, and if you die within that term, your beneficiaries get a payout. It's generally the most affordable option for a large death benefit. IUL, on the other hand, is permanent and builds cash value. While term life is great for temporary needs (like covering a mortgage), IUL offers lifelong coverage and the potential for wealth accumulation. If you want coverage that lasts your whole life and offers a savings component, IUL is the clear winner here.

IUL vs Whole Life Insurance Growth Potential and Control

Whole life insurance is also permanent and has a cash value that grows at a guaranteed, fixed rate. It's very predictable and stable. IUL, however, offers the potential for higher cash value growth because it's linked to a market index. While whole life provides certainty, IUL offers the chance for greater returns, albeit with a cap. You also typically have more flexibility with premiums in an IUL policy compared to the fixed premiums of whole life. If you're comfortable with a bit more market exposure for potentially higher returns, IUL might be a better fit.

IUL vs Variable Universal Life Insurance Risk and Protection

Variable Universal Life (VUL) insurance also has a cash value component that can grow, but it's directly invested in sub-accounts that are similar to mutual funds. This means you have the potential for unlimited upside, but also unlimited downside. If the market crashes, your cash value can lose money. IUL, with its floor, protects your cash value from market losses. So, if you want market-linked growth but are wary of direct investment risk, IUL offers a more conservative approach than VUL.

Top Indexed Universal Life Insurance Products and Providers Exploring Your Options

When it comes to choosing an IUL policy, there are many reputable providers out there, each with slightly different features, caps, and floors. It's crucial to shop around and compare. Here are a few examples of well-regarded IUL products and providers, keeping in mind that specific features and availability can vary by state and individual circumstances. Always consult with a qualified financial advisor to get personalized recommendations.

National Life Group FlexLife II A Strong Contender

National Life Group is a well-known name in the insurance industry, and their FlexLife II IUL product is often highlighted for its competitive features. It typically offers a strong cap rate, which means more potential for cash value growth when the market performs well. They also often have a 0% floor, ensuring your cash value won't lose money due to market downturns. FlexLife II is known for its flexibility in premium payments and access to cash value through loans. It's often recommended for individuals looking for robust cash value accumulation and strong living benefits, which can include riders for chronic, critical, and terminal illness. The cost can vary significantly based on age, health, and desired death benefit, but generally, IUL policies are more expensive than term life due to their permanent nature and cash value component. For a healthy 35-year-old male seeking a $500,000 death benefit, premiums could range from $300 to $600 per month, depending on the funding strategy and specific riders chosen.

Pacific Life Pacific Discovery Xelerator IUL A Focus on Growth

Pacific Life is another major player, and their Pacific Discovery Xelerator IUL is designed with a strong emphasis on cash value growth. This product often features competitive cap rates and participation rates, which determine how much of the index's performance is credited to your policy. It's known for its strong historical performance in cash value accumulation. Pacific Life also offers various riders, including those for long-term care, which can be a significant benefit. This product is often suitable for those prioritizing long-term wealth accumulation and potential tax-free income in retirement. Pricing would be similar to National Life Group, with monthly premiums for a healthy 35-year-old male for a $500,000 death benefit likely falling in the $350-$650 range, again depending on customization.

Transamerica Financial Foundation IUL Versatility and Options

Transamerica offers the Financial Foundation IUL, which is praised for its versatility and wide range of indexing options. They often provide multiple index choices, allowing policyholders to diversify how their cash value grows. This product also typically includes strong living benefits riders, providing financial protection in case of critical, chronic, or terminal illness. Transamerica's IUL is often a good fit for individuals who want a customizable policy with various options for cash value growth and comprehensive living benefits. The cost structure would be comparable to other top-tier IUL products, with premiums for a healthy 35-year-old male for a $500,000 death benefit in the ballpark of $320-$620 per month.

John Hancock Accumulation IUL A Reputable Choice

John Hancock is a long-standing and highly respected insurance company. Their Accumulation IUL product is known for its solid performance and strong financial backing. It typically offers competitive cap rates and a reliable 0% floor. John Hancock also provides various riders, including those for chronic illness, which can be a valuable addition. This product is often chosen by those who value a strong, established company with a history of financial stability and a well-rounded IUL offering. Expect similar pricing to the other examples, with monthly premiums for a healthy 35-year-old male for a $500,000 death benefit in the $340-$640 range.

Global Atlantic ForeCertain IUL A Newer Entrant with Strong Features

Global Atlantic is a relatively newer but rapidly growing player in the IUL market, and their ForeCertain IUL has gained attention for its competitive features. It often boasts attractive cap rates and a 0% floor, making it a strong contender for cash value growth. They also offer various riders and a focus on customer service. This product might appeal to those looking for a modern IUL solution with competitive growth potential. Pricing would be in line with the other major providers, with monthly premiums for a healthy 35-year-old male for a $500,000 death benefit likely between $330-$630.

Remember, these are just examples, and the best product for you will depend on your individual financial goals, risk tolerance, health, and budget. It's essential to work with an independent financial advisor who can compare multiple policies and illustrate their potential performance based on your specific situation.

Who Should Consider Indexed Universal Life Insurance Ideal Scenarios

IUL isn't for everyone, but it can be an excellent fit for certain individuals and families. Here are some scenarios where IUL really shines:

Individuals Seeking Permanent Coverage and Cash Value Growth

If you need lifelong life insurance coverage and want a policy that also has the potential to grow a significant cash value, IUL is definitely worth looking into. It's a great alternative to whole life if you want more growth potential than a fixed interest rate can offer, but without the direct market risk of VUL.

Those Looking for Tax-Advantaged Retirement Income

As we discussed, the ability to access cash value tax-free through policy loans makes IUL a powerful tool for supplementing retirement income. If you've maxed out your 401(k)s and IRAs and are looking for another tax-efficient way to save for retirement, IUL can be a fantastic option.

People Who Value Flexibility in Premiums and Death Benefit

Life happens, and your financial situation can change. If you appreciate the ability to adjust your premium payments and even your death benefit over time, IUL's flexibility will be a major advantage for you.

Business Owners and High Net Worth Individuals

For business owners, IUL can be used for executive bonus plans, key person insurance, or even buy-sell agreements. High net worth individuals often use IUL for estate planning, wealth transfer, and creating a tax-efficient asset that can be accessed during their lifetime. The tax advantages and potential for significant cash value growth make it a sophisticated financial planning tool.

Individuals Concerned About Market Volatility but Want Growth

If you're nervous about the stock market's ups and downs but still want your money to have the potential for growth beyond traditional savings accounts, the indexed nature of IUL with its floor protection is a perfect compromise.

Potential Downsides and Considerations for IUL Understanding the Trade-offs

While IUL offers many benefits, it's not without its considerations. It's important to understand the potential downsides before committing to a policy.

Caps on Growth Limiting Upside Potential

The biggest trade-off for the downside protection (the floor) is the cap on your growth. When the market performs exceptionally well, your IUL policy won't capture all of those gains. This can be frustrating for some who see the market soaring but their IUL cash value growth limited by the cap. It's a balance between risk and reward.

Fees and Charges Impacting Cash Value

IUL policies, like most permanent life insurance, come with various fees and charges. These can include administrative fees, cost of insurance (COI) charges, and surrender charges if you cancel the policy early. These fees can eat into your cash value, especially in the early years of the policy. It's crucial to understand the fee structure and how it impacts your net cash value growth.

Complexity and Understanding the Mechanics

IUL policies can be more complex than simpler term or whole life policies. Understanding how the index linking works, the caps, floors, participation rates, and various riders requires a bit of education. It's not a set-it-and-forget-it product, and you'll want to regularly review its performance and ensure it's meeting your goals.

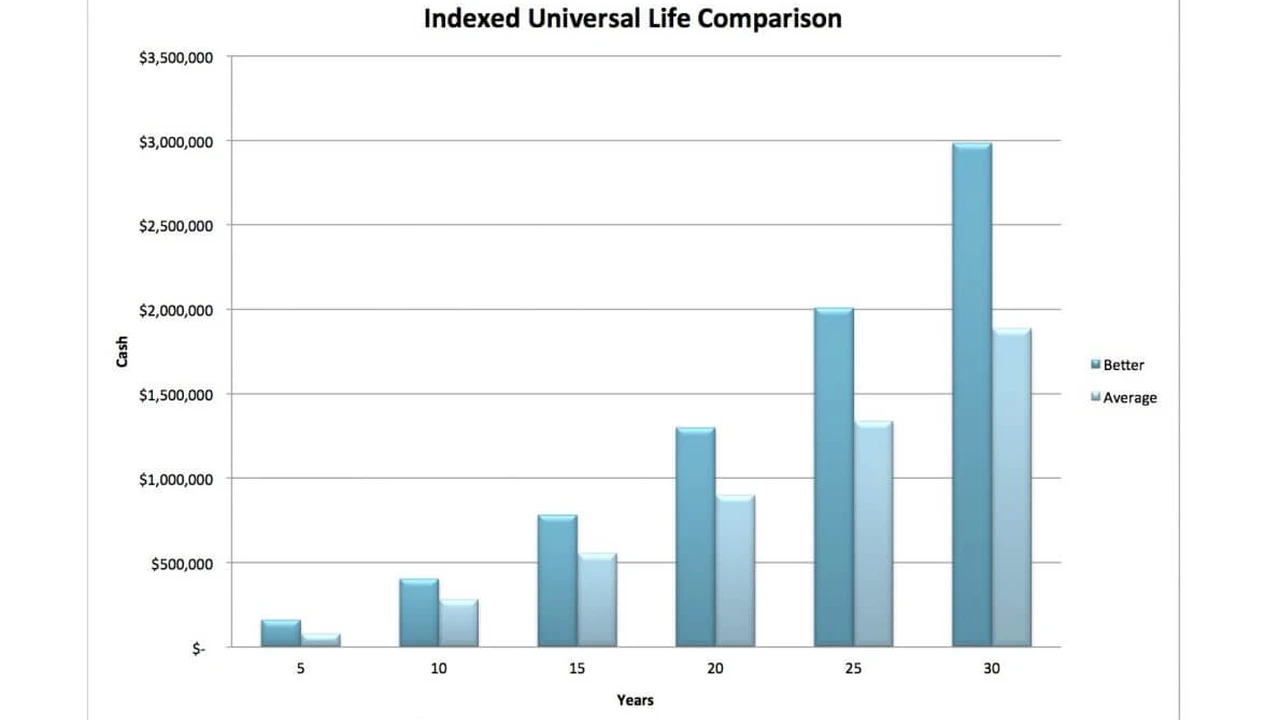

Illustrations vs Actual Performance Realistic Expectations

When you're presented with an IUL illustration, it will show projected cash value growth based on certain assumptions about future index performance. It's important to remember that these are illustrations, not guarantees (beyond the floor). Actual performance can vary, and it's wise to be conservative in your expectations and understand the difference between guaranteed and non-guaranteed values.

Maximizing Your Indexed Universal Life Insurance Policy Smart Strategies

If you decide IUL is right for you, there are ways to optimize its performance and get the most out of your policy.

Funding Your Policy Appropriately Consistent Contributions

To maximize cash value growth, it's generally recommended to fund your IUL policy consistently and adequately, especially in the early years. Over-funding (within IRS limits) can accelerate cash value accumulation, giving it more time to grow tax-deferred.

Understanding and Utilizing Riders Enhancing Coverage

Many IUL policies offer various riders that can enhance your coverage. These might include living benefits riders (for chronic, critical, or terminal illness), waiver of premium riders, or guaranteed insurability riders. Understand what's available and choose riders that align with your specific needs and concerns.

Regular Policy Reviews Staying on Track

Don't just buy an IUL policy and forget about it. Regularly review its performance with your financial advisor. Check the cash value growth, ensure your premiums are still appropriate, and make sure the policy continues to align with your evolving financial goals. Market conditions and your personal circumstances can change, so periodic adjustments might be necessary.

Leveraging Tax-Free Loans Strategic Access to Cash

One of the most powerful features of IUL is the ability to take tax-free loans from your cash value. Learn how to strategically use these loans, especially in retirement, to create a supplemental income stream without triggering immediate tax liabilities. Be mindful that loans reduce the death benefit if not repaid, and interest accrues on the loan.

The Future of Indexed Universal Life Insurance Trends and Innovations

The IUL market is constantly evolving, with new products and features being introduced regularly. Insurers are always looking for ways to make their IUL offerings more competitive, whether through higher caps, more attractive indexing strategies, or enhanced living benefits. We're seeing a trend towards more personalized policies, leveraging data and technology to better match products to individual needs. The focus on living benefits is also growing, as people want their life insurance to provide financial support not just upon death, but also during their lifetime if they face a serious illness. As financial planning becomes more complex, IUL is likely to continue to be a popular tool for those seeking a blend of protection, growth potential, and tax advantages.

So, there you have it – a deep dive into Indexed Universal Life insurance. It's a sophisticated financial product that offers a unique combination of lifelong protection, market-linked cash value growth with downside protection, and significant tax advantages. While it might seem a bit complex at first, understanding its mechanics and benefits can open up new possibilities for your financial planning. Whether you're looking to secure your family's future, build tax-advantaged wealth, or create a supplemental income stream for retirement, IUL could be a powerful tool in your financial arsenal. Just remember to do your homework, compare different products, and work with a trusted financial advisor to ensure it's the right fit for your unique situation. Happy planning!

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)