Life Insurance with Long Term Care Riders A Dual Benefit

Explore life insurance policies that include long-term care riders, offering both death benefit and care coverage.

Explore life insurance policies that include long-term care riders, offering both death benefit and care coverage.

Life Insurance with Long Term Care Riders A Dual Benefit

Life insurance is a cornerstone of financial planning, primarily designed to provide a financial safety net for your loved ones after you're gone. Long-term care (LTC) insurance, on the other hand, addresses the significant costs associated with extended care services, such as nursing home care, assisted living, or in-home care, which can quickly deplete savings. What if you could combine the benefits of both into a single, comprehensive policy? That's precisely what life insurance with long-term care riders offers: a dual benefit solution designed to protect your family's financial future while also safeguarding your assets against the potentially devastating costs of long-term care.

In today's world, the need for long-term care is a growing concern. Statistics show that a significant percentage of individuals over age 65 will require some form of long-term care during their lifetime. The costs associated with this care can be astronomical, often exceeding hundreds of thousands of dollars. Traditional long-term care insurance can be expensive, and many people are hesitant to pay premiums for a benefit they might never use. This is where the hybrid approach of life insurance with an LTC rider becomes incredibly appealing. It offers a solution that ensures your premiums aren't 'wasted' – either you use the LTC benefits, or your beneficiaries receive a death benefit.

This article will delve deep into the world of life insurance with long-term care riders. We'll explore how these policies work, their various types, the benefits they offer, and crucial considerations for anyone contemplating this dual-purpose financial tool. We'll also compare specific products, discuss their suitability for different scenarios, and provide insights into pricing and features to help you make an informed decision for your financial future in both the US and Southeast Asian markets.

Understanding Life Insurance with Long Term Care Riders How They Work

At its core, a life insurance policy with a long-term care rider is a traditional life insurance policy (often universal life or whole life) that includes an optional add-on, or 'rider,' allowing you to access a portion of your death benefit while you're still alive to cover qualified long-term care expenses. This means that if you need long-term care, the policy can pay out a monthly or annual benefit to cover those costs. If you never need long-term care, the full death benefit (or a slightly reduced one, depending on the policy structure) will be paid to your beneficiaries upon your passing.

The mechanism typically involves an 'acceleration of death benefit' for long-term care. When you qualify for long-term care benefits (usually by being unable to perform two out of six Activities of Daily Living – ADLs – or having a severe cognitive impairment), the policy begins to pay out a portion of your death benefit each month. This payout reduces the remaining death benefit. Some policies offer a 'dollar-for-dollar' reduction, meaning every dollar used for LTC reduces the death benefit by a dollar. Others might offer a 'leverage' feature, where the LTC benefit is greater than the amount by which the death benefit is reduced, effectively providing more LTC coverage than the face value of the policy.

It's important to distinguish these hybrid policies from standalone long-term care insurance. Standalone LTC policies are 'use it or lose it' – if you never need care, your premiums are not returned. Hybrid policies, however, guarantee a payout, either for long-term care or as a death benefit. This guarantee is a significant draw for many individuals who are wary of paying for a standalone LTC policy they might never utilize.

Key Benefits of Hybrid Life LTC Policies Financial Security and Peace of Mind

The advantages of combining life insurance with long-term care riders are numerous, offering a compelling solution for comprehensive financial planning:

Guaranteed Payout Life Insurance and Long Term Care

Unlike traditional long-term care insurance, which can feel like a gamble, hybrid policies guarantee a payout. Whether you need long-term care or not, the policy will provide a benefit. This eliminates the 'use it or lose it' concern, making it a more attractive option for many.

Asset Protection Against Long Term Care Costs

Long-term care costs can quickly decimate retirement savings and other assets. These policies act as a shield, protecting your wealth from being eroded by care expenses, ensuring your legacy remains intact for your beneficiaries.

Tax Advantages of Life Insurance and LTC Riders

In many jurisdictions, including the US, the death benefit of a life insurance policy is generally income tax-free. Furthermore, qualified long-term care benefits paid from these hybrid policies are often received income tax-free. This can provide significant tax efficiencies compared to drawing from taxable retirement accounts for care.

Simplified Underwriting for Combined Coverage

While underwriting is still required, some hybrid policies may have a more streamlined underwriting process compared to standalone long-term care insurance, especially for certain types of policies or riders. This can make it easier for individuals who might have difficulty qualifying for traditional LTC insurance.

Flexible Premium Payment Options for Hybrid Policies

Many hybrid policies offer flexible premium payment structures. You might be able to pay premiums over a set number of years (e.g., 10 or 20 years), pay a single lump sum, or pay premiums for the life of the policy. This flexibility allows you to tailor payments to your financial situation.

Inflation Protection for Future Care Needs

Many policies offer an inflation protection rider, which increases your long-term care benefit over time to keep pace with rising care costs. This is a crucial feature, as the cost of care is expected to continue to climb significantly in the coming decades.

Types of Life Insurance with Long Term Care Riders Policy Structures

While the core concept remains the same, these hybrid policies can be structured in a few different ways, primarily built upon either universal life or whole life insurance platforms:

Universal Life Insurance with Long Term Care Rider

This is perhaps the most common type of hybrid policy. Universal life insurance offers flexibility in premiums and death benefits. When combined with an LTC rider, it allows you to access a portion of the death benefit for long-term care. The cash value component of the universal life policy can also grow on a tax-deferred basis, providing an additional layer of financial benefit.

Whole Life Insurance with Long Term Care Rider

Whole life insurance provides guaranteed premiums, a guaranteed death benefit, and guaranteed cash value growth. Adding an LTC rider to a whole life policy offers the same dual benefit, but with the added predictability and guarantees inherent in whole life insurance. This can be appealing to those who prefer stability and fixed costs.

Single Premium Life Insurance with Long Term Care

For individuals with a lump sum of cash they wish to protect and leverage for future care, a single premium life insurance policy with an LTC rider can be an excellent option. You pay one large premium upfront, and the policy immediately provides both a death benefit and access to long-term care funds. This is often attractive to older individuals or those who have recently received an inheritance.

Comparing Specific Products and Providers US Market Focus

The US market offers a robust selection of life insurance policies with long-term care riders. Here, we'll highlight a few prominent providers and their offerings, keeping in mind that product availability and features can vary by state and individual circumstances. It's crucial to consult with a qualified financial advisor to determine the best fit for your specific needs.

Nationwide CareMatters II Hybrid Life LTC

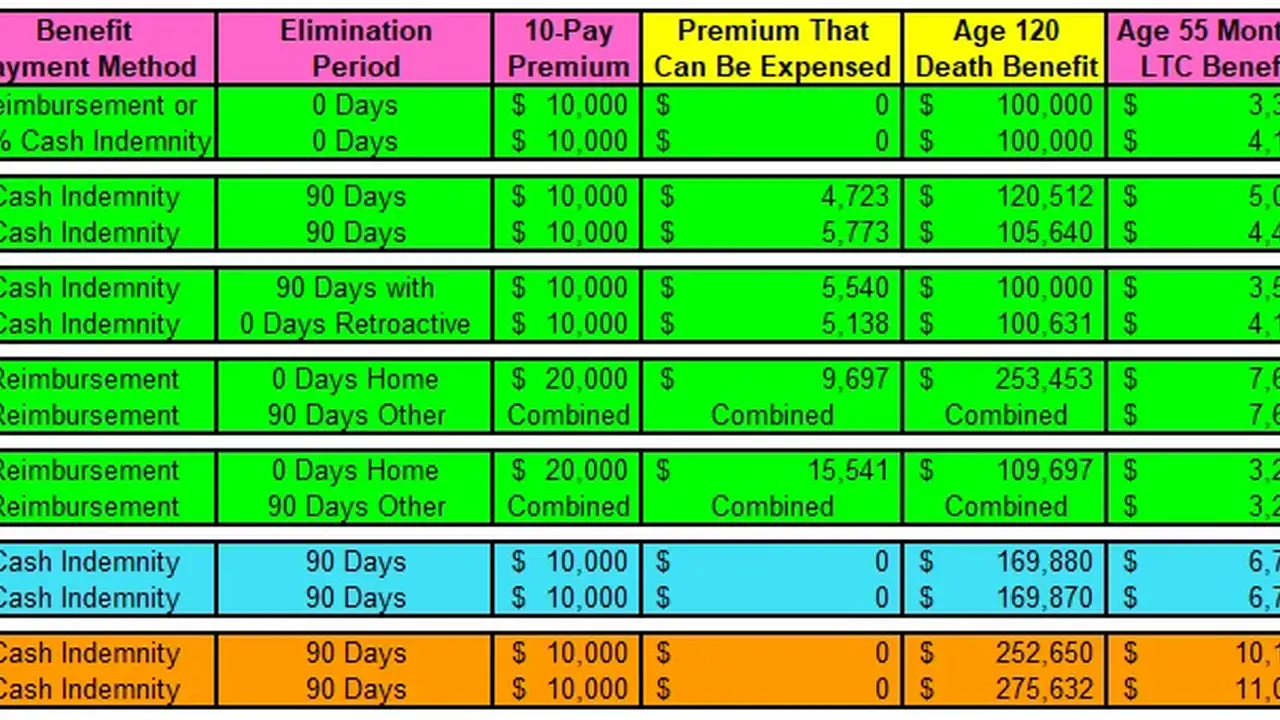

Product Overview: Nationwide's CareMatters II is a popular choice, known for its comprehensive long-term care benefits. It's a universal life insurance policy with a built-in long-term care rider. A key feature is its 'continuation of benefits' option, which can extend LTC payments beyond the initial death benefit amount, effectively providing more long-term care coverage than the policy's face value. It also offers a 'cash indemnity' benefit, meaning you receive a monthly cash payment for qualified care, with no need to submit receipts for reimbursement, offering greater flexibility.

Use Cases: Ideal for individuals seeking extensive long-term care coverage with the flexibility of cash indemnity. It's particularly suitable for those who want to ensure their care costs are covered even if they exceed the initial death benefit. Good for individuals looking for a strong balance between life insurance and robust LTC benefits.

Pricing Considerations: Premiums vary significantly based on age, health, gender, and desired benefit amounts. For a healthy 55-year-old male in the US, a policy with a $200,000 death benefit and a $4,000 monthly LTC benefit (with a 3% compound inflation rider) could range from $5,000 to $8,000 annually, or a single premium of $80,000 to $120,000. The continuation of benefits feature will add to the cost.

Lincoln MoneyGuard Solutions Hybrid Life LTC

Product Overview: Lincoln Financial Group's MoneyGuard Solutions series (e.g., MoneyGuard II, MoneyGuard Market Advantage) are also universal life policies with integrated long-term care benefits. They are known for their strong long-term care focus and often offer a 'return of premium' feature, guaranteeing that if you cancel the policy, you'll receive a portion of your premiums back. MoneyGuard Market Advantage, in particular, links cash value growth to market performance, offering potential for higher returns.

Use Cases: Excellent for those who prioritize long-term care coverage and appreciate the option of a return of premium. MoneyGuard Market Advantage appeals to individuals comfortable with some market exposure for potential cash value growth, while still having a guaranteed death benefit and LTC coverage. Suitable for those who want a robust LTC benefit with some liquidity options.

Pricing Considerations: Similar to Nationwide, premiums depend on various factors. For a healthy 60-year-old female, a policy with a $150,000 death benefit and a $3,000 monthly LTC benefit (with a 5% simple inflation rider) might cost $4,500 to $7,000 annually, or a single premium of $70,000 to $100,000. The market-linked options can have more variable pricing.

OneAmerica Asset Care Hybrid Life LTC

Product Overview: OneAmerica's Asset Care is a flexible hybrid product that can be structured as a single premium, 10-pay, or ongoing pay policy. It's often praised for its strong long-term care benefits and the ability to cover two lives (e.g., a married couple) under one policy, which can be more cost-effective. It also offers a 'shared care' option, allowing spouses to share their combined LTC benefits.

Use Cases: Particularly well-suited for couples looking for joint long-term care coverage. The shared care feature is a significant advantage for married individuals. Also a good option for those who prefer to pay a single premium or a limited number of premiums to get coverage in place quickly.

Pricing Considerations: For a healthy couple, both 60 years old, a joint policy with a combined $300,000 death benefit and a $6,000 monthly LTC benefit (with a 3% compound inflation rider) could have a single premium ranging from $150,000 to $250,000, or annual premiums of $10,000 to $18,000 for a 10-pay option.

Comparing Specific Products and Providers Southeast Asia Market Focus

The Southeast Asian market for hybrid life and long-term care products is evolving, with increasing demand for comprehensive solutions. While specific product names and features might differ from the US, the underlying principles remain similar. Local regulations and market conditions play a significant role. Here are some general insights and examples of types of products you might find:

Prudential PRULink Assurance Account with Health Riders

Product Overview: In many Southeast Asian countries like Singapore, Malaysia, and Indonesia, insurers like Prudential offer investment-linked life insurance plans (similar to universal life) that can be customized with various health and critical illness riders. While not always a direct 'long-term care' rider as seen in the US, these riders often provide benefits for severe illnesses, disability, or loss of independence, which can indirectly cover long-term care needs. Some newer products are emerging with more explicit LTC benefits.

Use Cases: Suitable for individuals seeking flexible life coverage with the option to add comprehensive health protection. Good for those who want to combine investment growth potential with protection against critical health events that could lead to long-term care needs. Appeals to those who prefer a single policy for multiple protection needs.

Pricing Considerations: Premiums are highly variable based on the investment component, sum assured, and the specific riders chosen. For a healthy 40-year-old in Singapore, a basic investment-linked policy with critical illness and disability riders could start from S$150-S$300 per month, with higher premiums for more extensive coverage and investment allocation.

Great Eastern GREAT Life Advantage with Care Riders

Product Overview: Great Eastern, a prominent insurer in Singapore and Malaysia, offers whole life or universal life plans that can be enhanced with riders for critical illness, total and permanent disability (TPD), and sometimes specific long-term care benefits. Their 'GREAT CareShield' in Singapore, for example, is a supplement to the national CareShield Life scheme, providing additional payouts for severe disability, which directly addresses long-term care costs.

Use Cases: Ideal for individuals who want guaranteed life coverage with robust protection against critical health events and disability. The integration with national schemes like CareShield Life makes it particularly relevant for Singaporean residents looking to top up their basic coverage. Good for those who prefer a more traditional, guaranteed approach to life insurance with added health benefits.

Pricing Considerations: For a healthy 45-year-old in Malaysia, a whole life policy with TPD and critical illness riders might cost RM300-RM600 per month, depending on the sum assured and number of critical illnesses covered. Specific long-term care riders or supplements would add to this cost.

AIA Power Critical Cover with Long Term Care Options

Product Overview: AIA, with a strong presence across Southeast Asia, offers various life insurance solutions that can be bundled with critical illness and disability riders. Some of their newer products are designed to provide payouts upon diagnosis of severe conditions or loss of independence, which can be used to fund long-term care. They often emphasize comprehensive coverage for a wide range of critical illnesses.

Use Cases: Suitable for individuals who want extensive critical illness coverage that can indirectly support long-term care needs. Appeals to those who value broad protection against a multitude of health risks. Good for individuals who prefer a single policy that addresses both life protection and health contingencies.

Pricing Considerations: For a healthy 50-year-old in Thailand, a life policy with comprehensive critical illness riders could range from THB 3,000-THB 6,000 per month, depending on the level of coverage and the number of critical illnesses included. Explicit long-term care benefits, if available as a rider, would increase the premium.

Important Considerations When Choosing a Hybrid Policy Key Factors

Selecting the right life insurance policy with a long-term care rider requires careful consideration of several factors:

Your Health and Age Underwriting for Hybrid Policies

Your current health and age will significantly impact your eligibility and premium costs. The younger and healthier you are, the more likely you are to qualify for better rates and more comprehensive coverage. Don't wait until health issues arise, as this can make coverage more expensive or even unobtainable.

Amount of Long Term Care Coverage Needed

Research the average cost of long-term care in your area (US or Southeast Asia). Consider how much monthly benefit you would need to cover these costs. Factor in inflation protection to ensure your benefit keeps pace with rising expenses over time. A common rule of thumb is to aim for coverage that would pay for at least 3-5 years of care.

Inflation Protection Rider Essential for Future Care Costs

This is a critical feature. Without inflation protection, a monthly benefit that seems adequate today could be woefully insufficient in 20 or 30 years. Look for policies offering at least 3% compound inflation protection.

Elimination Period Waiting Period for Benefits

This is the period (e.g., 30, 60, or 90 days) you must pay for long-term care out of pocket before the policy begins to pay benefits. A longer elimination period typically results in lower premiums, but means more initial out-of-pocket expense.

Benefit Period Duration of Long Term Care Payouts

This refers to how long the policy will pay out long-term care benefits. Some policies offer a fixed number of years (e.g., 3, 5, or 7 years), while others might offer a lifetime benefit or a 'pool of money' that can be drawn upon until exhausted. Consider your family history and potential longevity when choosing a benefit period.

Cash Indemnity vs Reimbursement Benefits

Some policies offer 'cash indemnity,' meaning they pay a fixed monthly amount once you qualify for care, regardless of your actual expenses. Others are 'reimbursement' policies, requiring you to submit receipts for qualified expenses. Cash indemnity offers greater flexibility but might be more expensive.

Return of Premium Feature Policy Liquidity

Some hybrid policies offer a return of premium feature, meaning if you decide to cancel the policy, you can get back a portion or even all of the premiums you've paid. This adds a layer of liquidity and reduces the 'use it or lose it' concern even further.

Financial Strength of the Insurer Company Stability

Always choose an insurance company with a strong financial rating from independent agencies like A.M. Best, Standard & Poor's, or Moody's. You want to be confident that the company will be around to pay claims decades down the line.

Policy Riders and Customization Options

Explore other available riders, such as waiver of premium (waives premiums if you're receiving LTC benefits), spousal riders, or non-forfeiture benefits. These can customize the policy to better fit your needs.

The Application Process for Hybrid Life LTC Policies What to Expect

Applying for a life insurance policy with a long-term care rider typically involves a more thorough underwriting process than a simple term life policy, as the insurer is assessing two types of risk. Here's a general overview:

Initial Consultation with a Financial Advisor

Start by discussing your needs and financial goals with a qualified financial advisor specializing in life insurance and long-term care. They can help you understand your options and recommend suitable products.

Application Submission Detailed Information Required

You'll complete a detailed application form, providing personal information, medical history, lifestyle details, and financial information. Be prepared to disclose any pre-existing conditions or medications.

Medical Exam and Health Questionnaire

Most policies will require a medical exam, which may include blood and urine tests, blood pressure readings, and a physical assessment. You'll also likely complete a comprehensive health questionnaire.

Cognitive Assessment for Long Term Care Eligibility

For the long-term care component, some insurers may conduct a cognitive assessment, especially for older applicants, to evaluate memory and cognitive function.

Review of Medical Records and Prescription History

The insurer will typically request access to your medical records from your physicians and review your prescription history to get a complete picture of your health.

Underwriting Decision and Policy Offer

Based on all the gathered information, the underwriter will assess your risk and determine your eligibility and premium rates. They will then issue a policy offer, which you can accept or decline.

Policy Delivery and Review Final Steps

Once you accept the offer and pay the initial premium, the policy will be delivered. It's crucial to review the policy document carefully to ensure all details are accurate and that you understand the terms and conditions.

Who Should Consider Life Insurance with Long Term Care Riders Ideal Candidates

This type of hybrid policy is not for everyone, but it can be an excellent solution for specific individuals and families:

Individuals Concerned About Long Term Care Costs

If you're worried about the financial burden of long-term care but are hesitant about traditional LTC insurance, a hybrid policy offers a compelling alternative.

Those Seeking a Guaranteed Payout for Life Insurance

If the 'use it or lose it' aspect of standalone LTC insurance is a deterrent, the guaranteed payout (either for care or as a death benefit) of a hybrid policy can provide peace of mind.

People with Existing Assets to Protect from Care Expenses

If you have significant assets you wish to preserve for your heirs, a hybrid policy can act as a protective shield against the high costs of long-term care.

Individuals Looking for Tax Efficient Wealth Transfer

The tax-free nature of death benefits and often LTC benefits can make these policies an attractive tool for estate planning and wealth transfer.

Younger Individuals Planning for Future Care Needs

Starting younger means lower premiums and more time for cash value growth. It's an excellent way to proactively address future long-term care needs while also securing life insurance.

Couples Seeking Joint Long Term Care Coverage

Many hybrid policies offer joint coverage options, which can be more cost-effective for couples looking to protect both spouses against long-term care expenses.

Common Misconceptions About Hybrid Life LTC Policies Clarifications

Despite their growing popularity, several misconceptions about life insurance with long-term care riders persist:

Myth 1 Hybrid Policies Are Too Expensive

While they can be more expensive than a basic term life policy, they often provide better value than buying separate life insurance and standalone LTC policies, especially when considering the guaranteed payout.

Myth 2 They Only Cover Nursing Home Care

Most modern hybrid policies cover a wide range of qualified long-term care services, including assisted living facilities, adult day care, and in-home care, offering flexibility in where and how you receive care.

Myth 3 You Lose Your Life Insurance if You Use LTC Benefits

While using LTC benefits reduces the death benefit, it doesn't eliminate it entirely unless the full death benefit amount is exhausted by care costs. A residual death benefit often remains.

Myth 4 They Are Only for the Wealthy

While they can be a sophisticated financial tool, hybrid policies are becoming more accessible to a broader range of income levels, especially with flexible premium options. They are a valuable tool for anyone looking to protect their assets from care costs.

Myth 5 Underwriting is Impossible for Older Individuals

While underwriting becomes stricter with age and health conditions, many insurers still offer options for older applicants, sometimes with modified benefits or higher premiums. It's always worth exploring.

The Future of Long Term Care Planning Evolving Solutions

The landscape of long-term care planning is continuously evolving. As healthcare costs rise and populations age, innovative solutions like hybrid life insurance with long-term care riders are becoming increasingly vital. We can expect to see more customization, integration with digital health platforms, and potentially more simplified underwriting processes in the future. The focus will remain on providing comprehensive, flexible, and financially sound options for individuals to protect themselves and their families against the uncertainties of long-term care needs.

Ultimately, the decision to purchase a life insurance policy with a long-term care rider is a personal one, deeply intertwined with your financial goals, health status, and risk tolerance. By understanding how these policies work, comparing available products, and considering the crucial factors outlined above, you can make an informed choice that provides significant financial security and peace of mind for years to come. Don't hesitate to engage with a knowledgeable financial professional who can guide you through the complexities and help you tailor a solution that perfectly fits your unique circumstances.

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)