5 Common Mistakes to Avoid When Buying Life Insurance

Learn about the most frequent errors people make when purchasing life insurance and how to avoid them.

Learn about the most frequent errors people make when purchasing life insurance and how to avoid them.

5 Common Mistakes to Avoid When Buying Life Insurance

Understanding Life Insurance The Basics and Why It Matters

Life insurance. It's one of those things many people know they *should* have, but often put off or find confusing. Think of it as a financial safety net for your loved ones. If something unexpected happens to you, your life insurance policy can provide a lump sum of money to your beneficiaries. This money can be used for anything from covering daily living expenses, paying off debts like mortgages or car loans, funding a child's education, or even covering funeral costs. It's about ensuring that even if you're no longer there to provide, your family's financial future remains secure. For families in the US, this can mean maintaining their lifestyle and avoiding financial hardship. In Southeast Asia, where social safety nets might be different, life insurance can be an even more critical tool for family protection and wealth transfer.

But here's the thing: buying life insurance isn't always straightforward. There are different types of policies, various terms, and a lot of jargon that can make your head spin. Because of this complexity, it's easy to make mistakes that could cost you money, leave your family underinsured, or even result in a policy that doesn't meet your needs at all. This article will walk you through five of the most common pitfalls people encounter when buying life insurance and, more importantly, how you can steer clear of them. We'll also touch on specific product recommendations and scenarios to help you make informed decisions.

Mistake 1 Not Buying Enough Life Insurance Coverage

This is perhaps the most prevalent mistake. Many people underestimate how much coverage their family would truly need to maintain their lifestyle if they were no longer around. It's not just about replacing your income for a few years; it's about covering all potential expenses and future financial goals.

Calculating Your Life Insurance Needs The DIME Method and Beyond

So, how do you figure out the right amount? A popular and easy-to-remember method is the DIME method:

* D - Debt: Add up all your outstanding debts, including your mortgage, car loans, credit card debt, and any personal loans. You want to ensure your family isn't burdened by these.

* I - Income: Multiply your annual income by the number of years your family would need financial support. A common recommendation is 5 to 10 times your annual salary, but this can vary greatly depending on your family's specific situation and future needs. Consider how long your children will be dependent or how long your spouse might need support to adjust.

* M - Mortgage: Include the full outstanding balance of your mortgage. For many families, this is their largest debt, and paying it off can provide immense peace of mind.

* E - Education: Factor in future education costs for your children, whether it's college tuition, private school, or vocational training. Education costs can be substantial, especially in the US.

Beyond DIME, also consider:

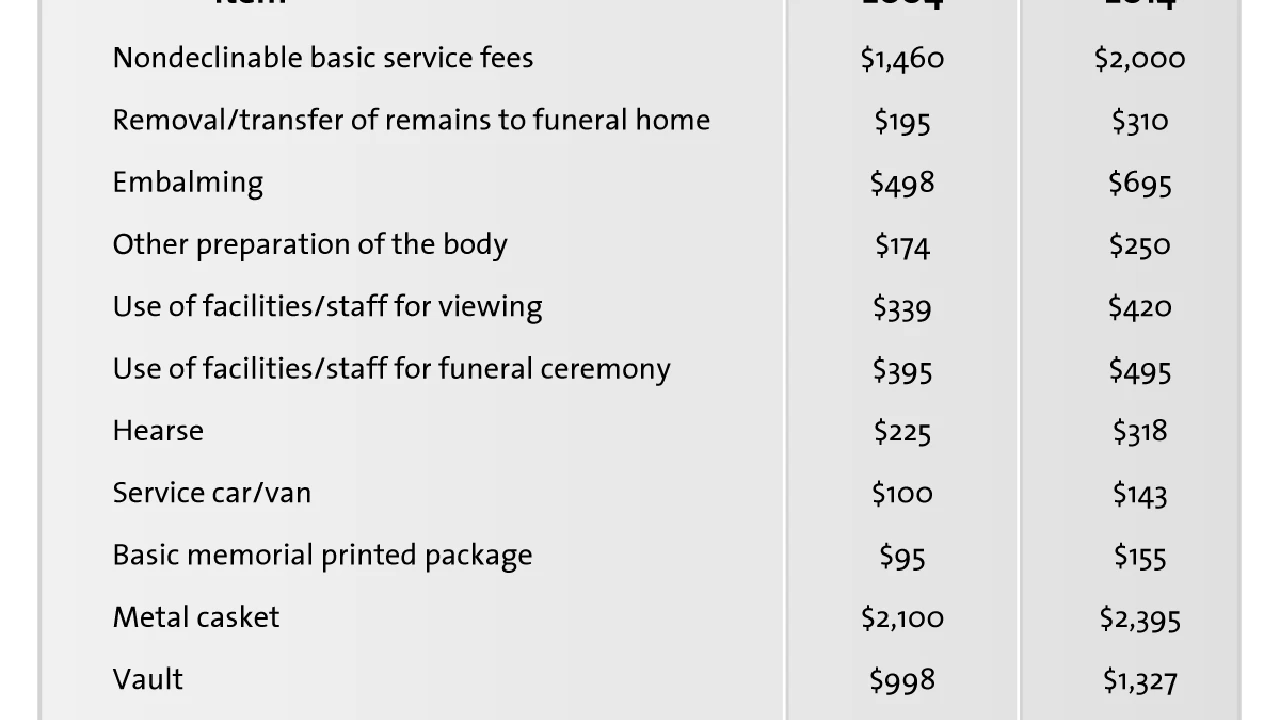

* Final Expenses: Funeral costs, medical bills not covered by health insurance, and estate settlement fees can quickly add up. A typical funeral in the US can cost between $7,000 and $12,000.

* Emergency Fund: Your family might need a buffer for unexpected expenses or a period of adjustment.

* Inflation: The cost of living tends to increase over time, so factor in a bit extra to account for future purchasing power.

Real World Scenarios and Product Recommendations for Adequate Coverage

Let's look at a couple of scenarios:

* **Scenario A: Young Family with a Mortgage and Young Children (US)**

* **Needs:** Replace income for 20 years, pay off a $300,000 mortgage, fund two children's college education ($100,000 each), cover $15,000 in other debts, and $10,000 for final expenses. If your annual income is $70,000, you might need: ($70,000 x 15 years = $1,050,000) + $300,000 (mortgage) + $200,000 (education) + $15,000 (debts) + $10,000 (final expenses) = **$1,575,000 in coverage.**

* **Recommended Product:** A 20-year or 30-year **Term Life Insurance** policy would be ideal here. It's generally the most affordable way to get a large amount of coverage for a specific period when your financial obligations are highest. Companies like **Haven Life** (backed by MassMutual) or **Ladder Life** offer straightforward online applications and competitive rates for term policies in the US. For a healthy 35-year-old, a $1.5 million 20-year term policy could range from $60-$100 per month, depending on health and specific provider.

* **Scenario B: Mid-Career Professional with Dependents and Business Interests (Southeast Asia)**

* **Needs:** Similar to Scenario A but with additional considerations for business continuity or succession. Perhaps a 15-year income replacement, a smaller mortgage, and significant education funds for children, plus a buffer for business partners. Let's say $1,000,000 in total.

* **Recommended Product:** Depending on the country, **Term Life Insurance** is still a strong contender for its affordability. However, some might consider a **Universal Life (UL) policy** for its flexibility, allowing adjustments to premiums and death benefits, which can be useful for evolving business needs. Companies like **Prudential**, **AIA**, or **Manulife** are prominent in Southeast Asia and offer a range of term and universal life products. A $1 million 20-year term policy for a healthy 40-year-old in Singapore might be around S$100-S$150 per month, while a UL policy would be significantly higher due to its cash value component.

Mistake 2 Choosing the Wrong Type of Life Insurance Policy

Life insurance isn't a one-size-fits-all product. There are two main categories: term life and permanent life (which includes whole life and universal life). Each serves different purposes, and picking the wrong one can lead to unnecessary costs or inadequate coverage.

Term Life Insurance Understanding Its Advantages and Use Cases

**Term life insurance** is straightforward: it covers you for a specific period (the 'term'), typically 10, 20, or 30 years. If you pass away within that term, your beneficiaries receive the death benefit. If you outlive the term, the policy expires, and there's no payout. It's like renting insurance.

* **Pros:** Generally much more affordable than permanent life insurance, allowing you to get a larger death benefit for your money. Simple to understand.

* **Cons:** No cash value accumulation. Coverage ends after the term.

* **Best for:** Young families, individuals with temporary financial obligations (like a mortgage or raising children), or those who want maximum coverage for the lowest premium.

Permanent Life Insurance Whole Life and Universal Life Explained

**Permanent life insurance** covers you for your entire life, as long as premiums are paid. It also includes a cash value component that grows over time on a tax-deferred basis. You can borrow against this cash value or withdraw from it.

* **Whole Life Insurance:** Premiums are typically fixed for life, and the cash value grows at a guaranteed rate. It's the most predictable type of permanent insurance.

* **Pros:** Guaranteed death benefit, guaranteed cash value growth, fixed premiums.

* **Cons:** Most expensive type of life insurance, less flexible.

* **Best for:** Estate planning, individuals seeking guaranteed cash value growth, or those who want lifelong coverage with predictable costs.

* **Universal Life (UL) Insurance:** Offers more flexibility than whole life. You can adjust your premium payments and death benefit (within certain limits). The cash value growth is not always guaranteed and can vary based on market performance (Indexed UL) or interest rates (Traditional UL).

* **Pros:** Flexible premiums and death benefit, cash value growth potential.

* **Cons:** More complex, cash value growth can be less predictable, potential for policy lapse if not managed properly.

* **Best for:** Individuals who need lifelong coverage but desire flexibility in payments, or those looking for additional cash value growth potential.

Comparing Products and Scenarios Term vs Whole vs Universal Life

* **Scenario C: Individual Focused on Estate Planning and Wealth Transfer (US/Southeast Asia)**

* **Needs:** Lifelong coverage to ensure a legacy for heirs, potentially to cover estate taxes or provide an inheritance. Cash value growth is a bonus.

* **Recommended Product:** **Whole Life Insurance** or **Guaranteed Universal Life (GUL)**. Whole life offers guaranteed growth and predictability. GUL offers lifelong coverage with fixed premiums but typically less cash value growth than traditional UL. For whole life, consider mutual companies like **Northwestern Mutual** or **Guardian Life** in the US, known for their strong dividends. In Southeast Asia, **Great Eastern** or **NTUC Income** (Singapore) offer robust whole life plans. A $500,000 whole life policy for a healthy 45-year-old could be $400-$700+ per month, significantly higher than term, but it's a different financial tool.

* **Scenario D: Business Owner Needing Flexible Coverage (US/Southeast Asia)**

* **Needs:** Coverage that can adapt to changing business fortunes, potentially using cash value for business opportunities, and lifelong protection.

* **Recommended Product:** **Universal Life Insurance**, particularly **Indexed Universal Life (IUL)**. IUL policies offer cash value growth linked to a market index (like the S&P 500) but with downside protection (a floor). This offers growth potential without direct market risk. Companies like **Pacific Life** or **National Life Group** are prominent IUL providers in the US. In Southeast Asia, providers like **AIA** and **Manulife** also offer IUL products. A $1 million IUL policy for a healthy 40-year-old might have premiums starting around $300-$500 per month, depending on the desired funding level and riders.

Mistake 3 Delaying the Purchase of Life Insurance

This is a classic. 'I'll get around to it next year.' The problem? Life insurance gets more expensive as you get older, and your health can change unexpectedly. The younger and healthier you are, the lower your premiums will be.

The Cost of Waiting How Age and Health Impact Premiums

Life insurance companies base your premiums largely on your life expectancy. As you age, your life expectancy naturally decreases, and the risk of health issues increases. This translates directly into higher premiums.

* **Age:** A 30-year-old will pay significantly less for the same coverage than a 40-year-old, and a 40-year-old will pay less than a 50-year-old. The difference can be hundreds or even thousands of dollars annually over the life of the policy.

* **Health:** If you develop a serious health condition (e.g., diabetes, heart disease, cancer) before applying, you might face much higher premiums, be rated (meaning you pay more due to higher risk), or even be denied coverage altogether. Even minor health changes can impact your rates.

Why Early Purchase is a Smart Financial Move

* **Lower Premiums:** Lock in lower rates when you're young and healthy. These rates are often guaranteed for the term of the policy (for term life) or for life (for whole life).

* **Guaranteed Insurability:** Once you have a policy, your insurability is generally locked in. Even if your health declines later, your existing policy remains in force (as long as premiums are paid).

* **Peace of Mind:** The sooner you have coverage, the sooner your family is protected. This peace of mind is invaluable.

Example of Cost Difference

Consider a healthy non-smoking male seeking a $500,000 20-year term policy:

* **Age 30:** Approximately $25-$35 per month.

* **Age 40:** Approximately $40-$60 per month.

* **Age 50:** Approximately $90-$130 per month.

As you can see, waiting just 10 years can nearly double your monthly premium. Over a 20-year term, that's a substantial difference in total cost.

Mistake 4 Not Reviewing Your Life Insurance Policy Regularly

Life isn't static, and neither should your life insurance policy be. What was adequate coverage five or ten years ago might not be sufficient today. Many people 'set it and forget it,' which can leave their loved ones vulnerable.

Life Changes That Warrant a Policy Review

Your life insurance needs are directly tied to your financial obligations and family structure. Significant life events should trigger a policy review:

* **Marriage or Divorce:** A new spouse might need to be added as a beneficiary, or an ex-spouse removed. Financial obligations change dramatically.

* **Birth or Adoption of a Child:** This is a huge one. New dependents mean significantly increased financial responsibilities, especially for education and daily care.

* **Purchasing a Home:** A new mortgage is a major debt that needs to be covered.

* **Significant Salary Increase or Decrease:** Your income replacement needs will change.

* **Starting a Business:** Business owners often need specialized coverage (like key person insurance) or need to ensure their business debts are covered.

* **Children Becoming Independent:** As children grow up and become financially independent, your income replacement needs might decrease, potentially allowing you to reduce coverage or shift focus.

* **Retirement:** Your financial obligations typically change in retirement. You might no longer need income replacement, but still need coverage for final expenses or estate planning.

* **Changes in Health:** While you can't change your existing policy's rates based on improved health, if you have a convertible term policy, you might consider converting it to permanent coverage while you're still relatively healthy.

How to Conduct a Policy Review and What to Look For

* **Check Beneficiaries:** Are they up to date? Are the percentages correct? This is crucial. An outdated beneficiary designation can lead to your death benefit going to the wrong person or getting tied up in probate.

* **Review Coverage Amount:** Does it still align with your current debts, income replacement needs, and future financial goals? Use the DIME method again.

* **Assess Policy Type:** Is term still appropriate, or have your needs shifted towards permanent coverage for estate planning? If you have a term policy nearing its end, what are your options for renewal or conversion?

* **Understand Riders:** Do you have any riders (e.g., waiver of premium, accelerated death benefit, child rider) that are still relevant or that you might need to add?

* **Compare Premiums:** While you can't change your existing policy's rates, it's worth occasionally checking current market rates for similar coverage. If your health has significantly improved, or if you have a very old policy, you might find better rates elsewhere, though be cautious about canceling an existing policy before a new one is in force.

Product Recommendations for Policy Adjustments

* **Scenario E: Growing Family with Increased Income (US/Southeast Asia)**

* **Needs:** Initially had a $500,000 term policy, but now have a larger mortgage, another child, and higher income. Need to increase coverage.

* **Recommended Action:** You can often **purchase an additional term policy** to layer on top of your existing one. For example, if you have a 10-year term for $500,000, you could buy another 20-year term for $1,000,000. This is often more cost-effective than replacing the entire policy. Alternatively, if your existing policy has a **Guaranteed Insurability Rider**, you can increase coverage without a new medical exam. Companies like **State Farm** or **New York Life** in the US, and **AIA** or **Prudential** in Southeast Asia, offer such riders.

* **Scenario F: Approaching Retirement, Kids are Grown (US/Southeast Asia)**

* **Needs:** Income replacement is less critical, but still want to cover final expenses and leave a small inheritance. Current term policy is expiring.

* **Recommended Action:** Consider converting your existing term policy to a **Whole Life** or **Guaranteed Universal Life (GUL)** policy if your term policy has a conversion option. This allows you to secure lifelong coverage without a new medical exam, often at a more favorable rate than buying a new permanent policy outright. If conversion isn't an option or is too expensive, a smaller **Final Expense Life Insurance** policy might be suitable. Providers like **Mutual of Omaha** (US) or local insurers in Southeast Asia offer these simplified issue policies.

Mistake 5 Not Being Honest on Your Application

This is a critical mistake that can have severe consequences. It might seem tempting to omit a minor health issue or a risky hobby to get a lower premium, but it's a dangerous gamble.

The Importance of Full Disclosure Underwriting and Contestability

Life insurance applications require you to provide accurate information about your health, lifestyle, and medical history. This information is used by underwriters to assess your risk and determine your premium.

* **Underwriting:** This is the process where the insurer evaluates your application. They look at your medical exam results, medical records (via an Attending Physician's Statement or APS), prescription history, driving record, and sometimes even your credit history. They are thorough.

* **Contestability Period:** Almost all life insurance policies have a 'contestability period,' typically the first two years after the policy is issued. During this time, if you pass away, the insurer has the right to investigate your application for any misrepresentations. If they find that you provided false or misleading information, they can deny the claim and refuse to pay the death benefit to your beneficiaries. This means your family, whom you intended to protect, would receive nothing.

* **Material Misrepresentation:** Even after the contestability period, if the insurer can prove 'material misrepresentation' (meaning the false information was significant enough to have affected their decision to issue the policy or the premium charged), they can still deny a claim.

Consequences of Misrepresentation for Your Beneficiaries

Imagine paying premiums for years, believing your family is protected, only for them to be denied the death benefit when they need it most. This is the devastating outcome of being dishonest on your application. It defeats the entire purpose of having life insurance.

Tips for a Smooth Application Process

* **Be Completely Honest:** Disclose all health conditions, medications, past medical treatments, smoking habits, and risky hobbies. It's always better to be upfront. The insurer will likely find out anyway through medical records or other checks.

* **Work with a Reputable Agent:** A good life insurance agent can help you navigate the application process, understand the questions, and ensure all information is accurately provided. They can also help you find insurers that are more lenient with certain conditions.

* **Gather Your Information:** Have your medical history, doctor's contact information, and any relevant dates (diagnoses, treatments) ready before you apply.

Specific Product Considerations for Health Conditions

* **Scenario G: Individual with a Controlled Pre-Existing Condition (US/Southeast Asia)**

* **Needs:** Needs life insurance but is concerned about higher premiums due to a condition like well-managed diabetes or high blood pressure.

* **Recommended Action:** Be honest. Many insurers specialize in or are more favorable towards certain conditions. For example, some companies like **John Hancock** (US) offer programs that reward healthy living, even with pre-existing conditions. In Southeast Asia, local insurers are increasingly offering more tailored products. You might get a 'rated' policy (higher premium), but it's better than no coverage or a denied claim. If traditional underwriting is too challenging, consider **Simplified Issue Life Insurance** or **Guaranteed Issue Life Insurance** (often for final expenses), which have fewer health questions but typically higher premiums and lower coverage limits. Companies like **AIG** or **Gerber Life** (US) offer simplified options.

By avoiding these five common mistakes, you'll be well on your way to securing a life insurance policy that truly protects your loved ones and provides the financial security you intend.

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)