The Impact of Health on Term Life Insurance Premiums

Discover how your health status can affect term life insurance premiums and tips for getting the best rates.

Discover how your health status can affect term life insurance premiums and tips for getting the best rates. Ever wondered why your friend pays less for their term life insurance even though you're the same age? Chances are, it boils down to health. Your health status is one of the biggest factors insurance companies consider when calculating your premiums. It's not just about whether you're currently sick; they look at a whole picture of your well-being. Let's dive deep into how your health impacts those crucial term life insurance premiums and what you can do to potentially snag a better rate.

The Impact of Health on Term Life Insurance Premiums

Understanding Underwriting How Health Classifications Work

When you apply for term life insurance, the insurance company goes through a process called underwriting. This is where they assess your risk. They want to figure out how likely you are to pass away during the policy term. The healthier you are, the lower the risk, and generally, the lower your premiums will be. They categorize applicants into different 'health classes' or 'risk classes.' These classifications are the foundation of your premium rates. While the exact names might vary slightly between insurers, they generally fall into categories like:

- Preferred Plus/Super Preferred: This is the crème de la crème. You're in excellent health, have no family history of early death from major diseases, maintain a healthy weight, don't smoke, and have a clean driving record. You'll get the absolute best rates here.

- Preferred: Still very good health, but maybe a minor health issue that's well-controlled, or a slightly less perfect family health history. You'll still get great rates, just not the absolute lowest.

- Standard Plus: Good health, but perhaps a few minor health issues, or a slightly higher BMI, or a family history that's a bit more concerning. Rates will be higher than Preferred.

- Standard: Average health for your age. You might have some controlled chronic conditions, or a less-than-ideal family health history. This is a common classification, and rates are moderate.

- Substandard/Table Rated: This is for individuals with more significant health issues, such as a history of heart disease, cancer, or diabetes that isn't perfectly controlled. These applicants are assigned a 'table rating' (e.g., Table 2, Table 4), which means an additional percentage is added to the standard premium. The higher the table number, the higher the premium.

Your goal, of course, is to qualify for the highest health class possible to secure the lowest premiums. But what exactly do they look at?

Key Health Factors Influencing Term Life Insurance Costs

Insurance companies are pretty thorough when it comes to evaluating your health. Here's a breakdown of the major factors they scrutinize:

Medical History and Current Health Conditions

This is probably the most significant factor. Insurers will ask about your past and present medical conditions. They're looking for:

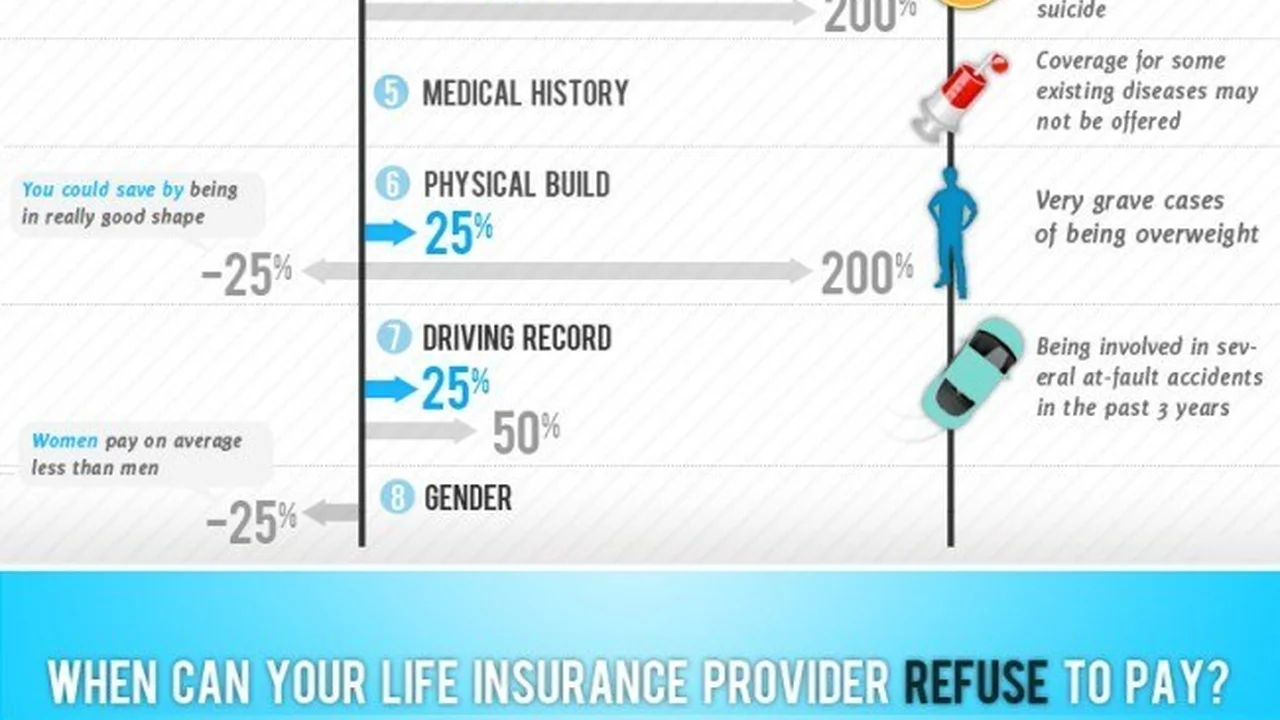

- Chronic Diseases: Conditions like diabetes, heart disease, high blood blood pressure, high cholesterol, asthma, and autoimmune disorders can significantly impact your rates. The severity, control, and duration of these conditions are all considered. For example, well-controlled Type 2 diabetes might lead to a Standard or Table rating, while uncontrolled Type 1 diabetes could result in higher Table ratings or even a decline.

- Major Illnesses: A history of cancer, stroke, or heart attack will definitely affect your premiums. The type of cancer, stage, treatment, and time since remission are all crucial. For instance, someone who had early-stage skin cancer removed five years ago might get a better rate than someone who recently completed treatment for aggressive lung cancer.

- Mental Health: Conditions like depression, anxiety, or bipolar disorder can also be a factor, especially if they've led to hospitalizations or significant medication use. Insurers want to understand the stability and management of these conditions.

- Medications: The types and dosages of medications you take provide clues about your health. Taking medication for high blood pressure is different from taking medication for a severe heart condition.

- Recent Surgeries or Hospitalizations: These can indicate underlying health issues or recovery periods that might affect your risk.

Family Medical History Genetic Predispositions

Yes, your family's health can affect your premiums! Insurers often ask about the health and causes of death of your parents and siblings, especially if they passed away before a certain age (often 60 or 65) due to conditions like heart disease, cancer, or stroke. A strong family history of these conditions can indicate a genetic predisposition, even if you're currently healthy. For example, if both your parents died of heart attacks in their 50s, you might not qualify for Preferred Plus rates, even if your own heart is currently in perfect shape.

Lifestyle Choices Smoking and Alcohol Consumption

These are huge. If you smoke or use any nicotine products (including vaping), expect to pay significantly more – often double or even triple the rates of a non-smoker. Insurers consider smokers to be a much higher risk due to the increased likelihood of various diseases. Similarly, excessive alcohol consumption or a history of alcohol abuse will lead to higher premiums or even a denial of coverage. They'll often ask about your drinking habits and may even check your liver enzymes during a medical exam.

Weight and Body Mass Index BMI

Your weight, specifically your Body Mass Index (BMI), is a key indicator of health. Being significantly overweight or obese increases your risk of heart disease, diabetes, and other health problems. Insurers have BMI charts they use to determine your health class. While a slightly elevated BMI might just move you from Preferred Plus to Preferred, a very high BMI could push you into a Standard or Table rating. Conversely, being underweight can also be a concern, as it might indicate underlying health issues.

Occupation and Hobbies High Risk Activities

While not strictly a 'health' factor, your job or hobbies can influence your risk profile. If you have a dangerous job (e.g., deep-sea fishing, skyscraper construction) or engage in high-risk hobbies (e.g., skydiving, rock climbing, car racing), insurers might charge higher premiums or even exclude coverage for deaths related to those activities. They see these as increasing your likelihood of accidental death.

Driving Record and Criminal History

Believe it or not, your driving record can impact your life insurance rates. A history of multiple speeding tickets, DUIs, or reckless driving indicates a higher risk-taking behavior, which insurers translate into a higher mortality risk. Similarly, a criminal record, especially for serious offenses, can also lead to higher premiums or denial.

The Medical Exam What to Expect

For most traditional term life insurance policies, especially for higher coverage amounts, you'll need to undergo a medical exam. This is usually done by a paramedical professional at your home or office and is paid for by the insurance company. The exam typically includes:

- Physical Measurements: Height, weight, blood pressure, and pulse.

- Blood and Urine Samples: These are tested for a wide range of indicators, including cholesterol levels, blood sugar (glucose), liver and kidney function, HIV, nicotine, and drug use.

- Medical History Questionnaire: You'll answer detailed questions about your personal and family medical history.

The results of this exam, combined with your application answers and potentially a review of your medical records (if authorized), form the basis of the underwriter's decision on your health class and premium.

Tips for Getting the Best Term Life Insurance Rates Despite Health Concerns

Even if you have some health issues, don't despair! There are strategies you can employ to try and secure the most favorable rates possible:

Improve Your Health Proactively

This is the most impactful long-term strategy. If you're considering life insurance, start making healthy changes now:

- Quit Smoking/Vaping: This is number one. If you quit and remain nicotine-free for at least 12 months (some insurers require longer), you can often qualify for non-smoker rates, which are significantly lower.

- Manage Chronic Conditions: Work with your doctor to get conditions like high blood pressure, diabetes, or high cholesterol under control. Show consistent adherence to medication and lifestyle recommendations. Well-managed conditions are viewed much more favorably.

- Achieve a Healthy Weight: Losing excess weight can improve your BMI and reduce your risk of various diseases, potentially moving you into a better health class.

- Regular Exercise and Healthy Diet: These contribute to overall health and can positively impact your blood pressure, cholesterol, and blood sugar levels.

Remember, insurers look at your health over time. Consistent healthy habits will pay off.

Be Honest and Thorough on Your Application

It might be tempting to omit minor details, but don't. Always be completely honest and accurate on your application. If you misrepresent your health, the policy could be contested or even voided later, leaving your beneficiaries without the payout they expect. Insurers have ways of verifying information, including accessing medical records (with your permission) and prescription databases.

Shop Around and Compare Multiple Insurers

This is crucial. Different insurance companies have different underwriting guidelines and risk appetites. One insurer might be more lenient on a particular health condition than another. For example, Company A might rate well-controlled diabetes as Standard, while Company B might offer Standard Plus. Getting quotes from several providers is the best way to find the one that offers you the most competitive rate for your specific health profile. An independent insurance agent or broker can be invaluable here, as they work with multiple carriers and can help you find the best fit.

Consider a Reconsideration After Health Improvement

If you've made significant health improvements after being approved for a policy (e.g., quit smoking, lost a lot of weight, got a chronic condition under much better control), you can often request a 'reconsideration' from your insurance company. They might re-evaluate your health class and lower your premiums. This usually involves another medical exam and updated medical records.

Explore No Medical Exam Options for Certain Situations

If your health is significantly compromised, or you simply want a quicker process, 'no medical exam' term life insurance policies are an option. These policies typically rely on a health questionnaire and database checks. However, they often come with higher premiums and lower coverage limits compared to fully underwritten policies. They can be a good solution for those who might struggle to qualify for traditional coverage or need coverage quickly. Examples include simplified issue or guaranteed issue policies, though guaranteed issue is usually for final expenses and has very low limits.

Specific Product Recommendations and Scenarios

Let's look at some hypothetical scenarios and how different products or strategies might apply, keeping in mind that actual rates depend on individual underwriting.

Scenario 1: The Healthy Young Professional

Profile: 30-year-old, non-smoker, excellent health, no family history of early disease, active lifestyle. Needs $1,000,000 for 20 years.

Recommendation: This individual is a prime candidate for Preferred Plus rates on a traditional fully underwritten term life policy. Companies like Haven Life (backed by MassMutual), Ethos (partners with various carriers), or traditional insurers like Northwestern Mutual or State Farm would likely offer excellent rates. They should definitely go through the full medical exam to secure the lowest possible premiums. For example, a 20-year, $1M policy might cost around $30-40 per month, depending on the insurer and exact health classification.

Scenario 2: The Individual with Well-Controlled Chronic Condition

Profile: 45-year-old, non-smoker, diagnosed with Type 2 diabetes 5 years ago, well-controlled with medication and diet, regular doctor visits, good A1C levels. Needs $750,000 for 20 years.

Recommendation: This person would likely fall into a Standard or Table 2-4 rating. It's crucial to shop around. Some insurers are more lenient with diabetes than others. Companies known for being more flexible with certain conditions include Prudential and John Hancock (especially with their Vitality program that rewards healthy living). They should be prepared for a medical exam and provide detailed medical records to demonstrate good control. A 20-year, $750K policy might range from $80-150 per month, depending on the insurer's specific underwriting for diabetes.

Scenario 3: The Former Smoker

Profile: 50-year-old, quit smoking 2 years ago, otherwise good health. Needs $500,000 for 15 years.

Recommendation: The key here is the 2-year mark. Many insurers require 12 months nicotine-free for non-smoker rates, but some prefer 2-5 years for the absolute best rates. This individual should apply for a fully underwritten policy and be honest about their smoking history and quit date. They will likely qualify for non-smoker rates, but perhaps not Preferred Plus immediately. Companies like Protective or Transamerica are often competitive. A 15-year, $500K policy might be in the $60-100 per month range, significantly less than if they were still smoking.

Scenario 4: The Individual with Significant Health Issues or Seeking Quick Coverage

Profile: 60-year-old, history of heart attack 3 years ago, takes multiple medications, wants coverage for final expenses and a small legacy. Needs $50,000 for 10 years.

Recommendation: A fully underwritten policy might be very expensive or difficult to obtain. This person should explore 'simplified issue' term life insurance or even 'guaranteed issue' whole life insurance (which is often used for final expenses but can be a term alternative for very high-risk individuals). Simplified issue policies from companies like Mutual of Omaha or Gerber Life (for smaller amounts) might be an option, requiring a health questionnaire but no medical exam. Guaranteed issue policies from companies like AARP (New York Life) or Colonial Penn are available but have very low coverage limits and high premiums for the amount of coverage. For a $50,000 simplified issue term policy, premiums could be $150-300+ per month, depending on the health questions answered. Guaranteed issue would be even higher for the same face amount, but often limited to $25,000 or less.

The Role of Independent Agents and Online Comparison Tools

Navigating the complexities of health classifications and finding the best rates can be daunting. This is where resources come in handy:

- Independent Insurance Agents: These professionals work with multiple insurance companies. They can assess your health profile and recommend insurers that are typically more favorable for your specific conditions. They can also help you prepare for the application and medical exam.

- Online Comparison Websites: Sites like Policygenius, SelectQuote, or Quotacy allow you to get quotes from numerous carriers by entering your health information. While these initial quotes are estimates, they give you a good starting point and can help you identify competitive insurers.

Final Thoughts on Health and Term Life Insurance

Your health is undeniably the most influential factor in determining your term life insurance premiums. While some factors like family history are beyond your control, many others, such as managing chronic conditions, quitting smoking, and maintaining a healthy weight, are within your power to improve. By taking proactive steps to enhance your well-being and diligently shopping around for the right insurer, you can significantly impact the cost of your coverage and ensure your loved ones are protected without breaking the bank. Don't let past health issues deter you; many options exist, and a little effort can lead to substantial savings.

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)