The Best Life Insurance for Single Parents Protecting Your Family

Find suitable life insurance options for single parents to ensure their children's financial security.

Find suitable life insurance options for single parents to ensure their children's financial security.

The Best Life Insurance for Single Parents Protecting Your Family

Why Life Insurance is Crucial for Single Parents Financial Security

Being a single parent is a monumental task, filled with love, challenges, and an unwavering commitment to your children's well-being. You are often the sole provider, caregiver, and emotional anchor. This unique position makes life insurance not just a good idea, but an absolute necessity. If something were to happen to you, who would step in to cover the costs of raising your children, their education, daily expenses, and future dreams? Life insurance provides that critical safety net, ensuring your children are financially protected, even if you're no longer there to provide for them directly.

Many single parents might think life insurance is an added expense they can't afford, or perhaps they believe their existing employer-provided coverage is sufficient. However, employer-sponsored plans are often basic and may not provide enough coverage for a single-income household. Furthermore, they typically terminate if you leave your job. For single parents, the stakes are higher, and a comprehensive, personally owned life insurance policy is paramount. It offers peace of mind, knowing that your children's future is secure, regardless of life's unpredictable turns.

Understanding Your Life Insurance Needs Single Parent Edition

Determining how much life insurance you need as a single parent requires careful consideration of several factors. It's not just about covering immediate funeral costs; it's about replacing your income, funding future expenses, and ensuring your children's long-term financial stability. Here's a breakdown of what to consider:

Income Replacement and Daily Living Expenses

Your primary goal is to replace your income for the years your children will be dependent. Consider their current age and how many years they will need financial support for food, housing, clothing, transportation, and extracurricular activities. A common rule of thumb is to multiply your annual income by 10 to 15, but for single parents, it might be even higher due to the lack of a second income.

Education Costs Future Planning for Children

Education is a significant expense. Factor in the cost of college tuition, books, and living expenses. Even if your children are young, it's wise to estimate these future costs and include them in your coverage amount. A 529 plan or other college savings vehicles can be supplemented by life insurance proceeds.

Debt Obligations and Mortgage Protection

Do you have a mortgage, car loans, credit card debt, or other outstanding liabilities? Your life insurance should ideally cover these debts to prevent them from becoming a burden on your children or their future guardians. Ensuring your home is paid off can provide immense stability.

Childcare and Future Caregiver Costs

If you pass away, who will care for your children? The designated guardian will likely incur significant costs for childcare, especially if they need to reduce their work hours or hire additional help. Your policy should account for these potential expenses.

Funeral and Estate Settlement Costs

While often overlooked, funeral expenses can be substantial. Additionally, there might be legal fees associated with settling your estate. A portion of your life insurance should be allocated to cover these immediate costs.

Inflation and Future Financial Needs

Remember to factor in inflation. The cost of living and education will likely increase over time. It's prudent to add a buffer to your coverage amount to account for future economic changes.

Types of Life Insurance Best Suited for Single Parents

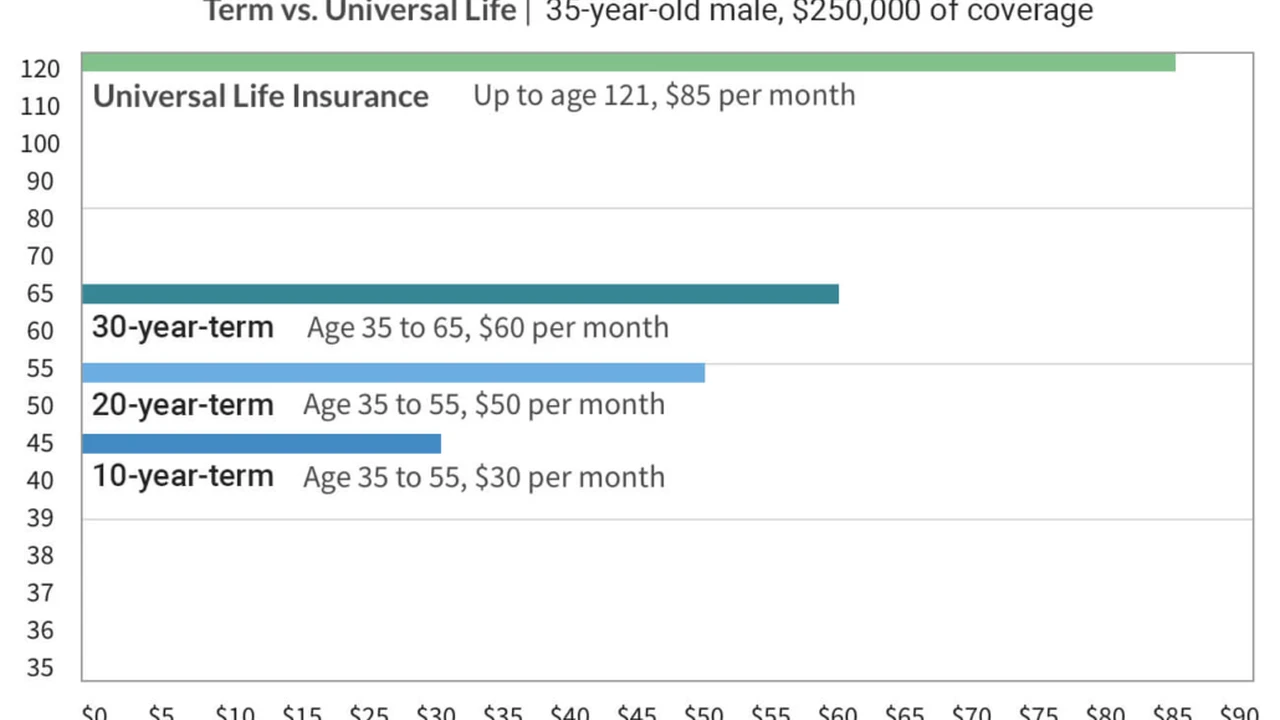

When it comes to life insurance, there are two main categories: term life and permanent life. Each has its advantages, and the best choice for you will depend on your specific circumstances, budget, and long-term goals.

Term Life Insurance Affordable Coverage for Specific Periods

Term life insurance is often the most recommended option for single parents due to its affordability and simplicity. It provides coverage for a specific period, or 'term,' typically 10, 20, or 30 years. If you pass away within that term, your beneficiaries receive a death benefit. If you outlive the term, the policy expires, and there's no payout. The main advantage is that you can secure a substantial amount of coverage for a relatively low premium, which is crucial for single-income households.

- Pros: Most affordable, easy to understand, can be tailored to cover the years your children are dependent.

- Cons: No cash value, coverage ends after the term, premiums increase if you renew at an older age.

- Best for: Single parents who need maximum coverage for the years their children are financially dependent, often until they graduate college or become self-sufficient.

Whole Life Insurance Permanent Coverage and Cash Value Growth

Whole life insurance is a type of permanent life insurance that provides coverage for your entire life, as long as premiums are paid. It also includes a cash value component that grows over time on a tax-deferred basis. You can borrow against this cash value or even surrender the policy for its cash value. While more expensive than term life, it offers lifelong protection and a savings component.

- Pros: Lifelong coverage, guaranteed cash value growth, potential for dividends, can be used for estate planning.

- Cons: Significantly more expensive than term life, less flexibility with premiums.

- Best for: Single parents who want lifelong coverage, a guaranteed savings component, and can afford higher premiums. It can also be beneficial for leaving a legacy or covering final expenses regardless of when you pass away.

Universal Life Insurance Flexible Permanent Coverage Options

Universal life (UL) insurance is another form of permanent life insurance, offering more flexibility than whole life. You can adjust your premium payments and death benefit over time, within certain limits. It also has a cash value component that grows, often tied to an interest rate. There are different types of UL, including Indexed Universal Life (IUL) and Variable Universal Life (VUL), which offer different ways for the cash value to grow, often with more risk and potential reward.

- Pros: Flexible premiums and death benefit, cash value growth, lifelong coverage.

- Cons: More complex than term or whole life, cash value growth can be less predictable, potential for policy lapse if not managed carefully.

- Best for: Single parents who need permanent coverage but desire more flexibility in premium payments and death benefits, and are comfortable with a bit more complexity.

Top Life Insurance Products for Single Parents Product Comparisons

Let's look at some specific products and providers that are often well-regarded for single parents, considering their needs for affordability, comprehensive coverage, and ease of application. Please note that specific rates and features can vary based on age, health, location, and underwriting.

1. Policygenius Term Life Insurance Marketplace

Product Type: Term Life Insurance (marketplace for various carriers)

Why it's great for single parents: Policygenius isn't an insurer itself, but an independent marketplace that allows you to compare quotes from multiple top-rated insurance companies. This is incredibly valuable for single parents who need to find the most affordable rates for substantial coverage. They simplify the application process and have licensed agents to guide you.

Key Features:

- Compares quotes from over a dozen A-rated insurers.

- Offers terms from 10 to 30 years.

- Streamlined online application process.

- Access to no-medical-exam options for quicker approval.

Typical Use Case: A single parent in their 30s or 40s with young children, looking for a 20- or 30-year term policy to cover their income and future education costs until their children are independent. They want to ensure they get the best possible rate by comparing multiple providers.

Estimated Cost: For a healthy 35-year-old single parent seeking $500,000 in 20-year term coverage, premiums could range from $25-$40 per month, depending on the insurer and health rating. For $1,000,000 in coverage, it might be $40-$70 per month.

2. Haven Life Term Life Insurance

Product Type: Term Life Insurance (issued by MassMutual or C.M. Life, a MassMutual subsidiary)

Why it's great for single parents: Haven Life offers a fully online application process, often providing an instant decision for healthy applicants. This speed and convenience are a huge plus for busy single parents. They offer competitive rates and a straightforward product.

Key Features:

- Instant online quotes and decisions for eligible applicants.

- Coverage up to $3 million.

- Terms from 10 to 30 years.

- Haven Term policy may require a medical exam, but Haven Simple offers no-medical-exam options for smaller coverage amounts.

Typical Use Case: A single parent who needs quick, reliable term coverage and prefers a digital-first experience. They are generally healthy and want to secure a policy without extensive paperwork or multiple appointments.

Estimated Cost: A healthy 40-year-old single parent applying for $750,000 in 20-year term coverage might pay around $40-$60 per month. Rates are highly dependent on health and lifestyle factors.

3. Ladder Life Term Life Insurance

Product Type: Term Life Insurance

Why it's great for single parents: Ladder Life stands out for its flexibility, allowing policyholders to 'ladder up' or 'ladder down' their coverage amount as their needs change. This is ideal for single parents whose financial situation or family needs might evolve over time. For example, you might need more coverage when your children are young and less as they become adults.

Key Features:

- Ability to increase or decrease coverage online without reapplying for a new policy (subject to underwriting for increases).

- Instant decisions for many applicants.

- Coverage up to $8 million.

- Terms from 10 to 30 years.

Typical Use Case: A single parent whose income or debt levels might fluctuate, or who anticipates their financial responsibilities decreasing as their children grow older. They appreciate the ability to adjust their policy without hassle.

Estimated Cost: Similar to Haven Life, a healthy 38-year-old single parent seeking $600,000 in 25-year term coverage could expect premiums in the $35-$55 per month range.

4. Northwestern Mutual Whole Life Insurance

Product Type: Whole Life Insurance

Why it's great for single parents: While more expensive, Northwestern Mutual is consistently top-rated for its financial strength and dividend payouts on participating whole life policies. For single parents who prioritize lifelong coverage, guaranteed cash value growth, and the potential for dividends, this can be a strong option, especially if they have a stable income and want to build a legacy.

Key Features:

- Guaranteed level premiums and death benefit for life.

- Guaranteed cash value growth.

- Participating policies may pay dividends, which can increase cash value or reduce premiums.

- Strong financial ratings and customer service.

Typical Use Case: A single parent with a higher, stable income who wants to ensure lifelong financial protection for their children (even as adults), build a tax-deferred cash reserve, and potentially leave a significant legacy. They are looking for a long-term financial tool beyond just income replacement.

Estimated Cost: Whole life premiums are significantly higher. For a healthy 35-year-old single parent seeking $250,000 in whole life coverage, premiums could easily be $200-$400+ per month, depending on various factors. The higher cost reflects the lifelong coverage and cash value component.

5. Guardian Life Insurance Company of America Universal Life Insurance

Product Type: Universal Life Insurance

Why it's great for single parents: Guardian offers various universal life products, including guaranteed universal life (GUL) which provides lifelong coverage with fixed premiums, similar to whole life but often at a lower cost. Their flexible UL options can be beneficial for single parents who need permanent coverage but might need to adjust premiums or death benefits in the future due to changing financial circumstances.

Key Features:

- Flexible premiums and death benefits.

- Cash value growth (rate varies by policy type).

- Option for guaranteed universal life for fixed, lifelong coverage.

- Strong financial stability.

Typical Use Case: A single parent who wants permanent coverage but needs more flexibility than whole life offers. They might anticipate periods where they need to pay less into the policy or want the option to increase coverage later. GUL is particularly attractive for those who want lifelong coverage without the higher cost of whole life.

Estimated Cost: For a healthy 40-year-old single parent seeking $500,000 in guaranteed universal life coverage, premiums could be in the range of $100-$200+ per month, depending on the specific policy and guarantees. Non-guaranteed UL policies might start lower but have more variable costs.

Key Considerations for Single Parents When Buying Life Insurance

Beyond choosing the type of policy, there are several other critical aspects single parents should pay close attention to:

Naming Beneficiaries and Contingent Beneficiaries

This is perhaps the most important step. You'll name your children as primary beneficiaries, but since they are minors, the death benefit cannot be paid directly to them. You must designate a trusted adult (the same person you'd likely name as their guardian) as the trustee of the funds for your children. It's also crucial to name contingent beneficiaries in case your primary beneficiaries are unable to receive the funds. Consult with an estate planning attorney to set up a trust for your children, which will manage the life insurance proceeds according to your wishes.

Appointing a Legal Guardian for Your Children

Your life insurance policy provides financial protection, but it doesn't appoint a guardian for your children. This is a separate, but equally vital, step. You need to legally designate a guardian in your will. This person will be responsible for raising your children and managing their daily lives. Ensure this person is aware of your wishes and is willing and able to take on this responsibility.

Reviewing Your Policy Regularly Life Changes

Life insurance isn't a set-it-and-forget-it product, especially for single parents. Your needs will change as your children grow, your income fluctuates, or your debt levels change. Review your policy annually or whenever there's a significant life event (e.g., a new job, a pay raise, a child starting college) to ensure your coverage still aligns with your family's needs.

Riders and Additional Coverage Options

Consider adding riders to your policy to enhance its coverage. Some common riders beneficial for single parents include:

- Waiver of Premium Rider: If you become disabled and can't work, this rider waives your premiums, keeping your policy in force.

- Child Rider: Provides a small amount of coverage for each of your children, often convertible to a permanent policy later.

- Accidental Death Benefit Rider: Pays an additional death benefit if your death is due to an accident.

- Guaranteed Insurability Rider: Allows you to purchase additional coverage in the future without a new medical exam, useful if your income or family grows.

The Application Process for Single Parents What to Expect

Applying for life insurance can seem daunting, but understanding the process can make it smoother:

Online Quotes and Initial Application

Start by getting online quotes from various providers or using a marketplace like Policygenius. This will give you an idea of potential costs. The initial application will ask for basic personal information, health history, and lifestyle details.

Medical Exam and Underwriting

Most traditional life insurance policies require a medical exam, which is typically free and conducted by a paramedical professional at your home or office. They'll take blood and urine samples, measure blood pressure, height, and weight. The insurer's underwriters will then review your medical history, lifestyle, and other factors to determine your risk class and premium.

No Medical Exam Options: For busy single parents, no-medical-exam policies (like simplified issue or guaranteed issue) can be appealing for their speed. However, they often come with higher premiums or lower coverage limits. They can be a good option if you need coverage quickly or have health issues that make traditional underwriting difficult.

Policy Issuance and Acceptance

Once underwriting is complete, the insurer will offer you a policy with a specific premium. Review the policy carefully to ensure it meets your expectations before accepting it. Once accepted, you'll start paying premiums, and your coverage will be in force.

Common Mistakes Single Parents Make and How to Avoid Them

Being proactive can save you and your children from potential pitfalls:

Underinsuring Your Family

The biggest mistake is not buying enough coverage. Use a life insurance calculator and be realistic about all future expenses your children will incur. It's better to be slightly over-insured than significantly under-insured.

Not Naming a Legal Guardian

Life insurance provides money, but not a parent. Failing to legally appoint a guardian in your will can lead to court battles and uncertainty for your children.

Forgetting Contingent Beneficiaries

Always name contingent beneficiaries. If your primary beneficiaries (your children's trustee) are unable to receive the funds, the contingent beneficiaries will step in, preventing the proceeds from going into your estate and potentially through probate.

Delaying the Purchase

The younger and healthier you are, the cheaper life insurance will be. Don't put it off. Every year you wait, premiums typically increase, and health issues can arise that make coverage more expensive or harder to obtain.

Not Reviewing Your Policy

Your life changes, and so should your policy. Regularly review and update your beneficiaries, coverage amounts, and contact information.

Empowering Your Children's Future with Life Insurance

As a single parent, your dedication to your children is boundless. Life insurance is a tangible expression of that love, a promise that their future will be protected, no matter what. It's an investment in their education, their dreams, and their stability. By taking the time to understand your needs, explore your options, and secure the right policy, you're building a lasting legacy of care and financial security for the most important people in your life.

Don't let the complexities deter you. Start by getting a few quotes, speak with a reputable financial advisor or insurance agent, and make an informed decision. The peace of mind that comes with knowing your children are protected is truly invaluable. Take this crucial step today to safeguard their tomorrow.

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)