Top 4 Universal Life Insurance Policies for Flexibility

Compare the best universal life insurance policies offering flexible premiums and adjustable death benefits.

Compare the best universal life insurance policies offering flexible premiums and adjustable death benefits. Universal Life (UL) insurance is a type of permanent life insurance that offers both a death benefit and a cash value component, much like whole life insurance. However, UL policies stand out due to their remarkable flexibility. Unlike whole life, which typically has fixed premiums and a guaranteed cash value growth rate, universal life allows policyholders to adjust their premium payments and death benefit amounts within certain limits. This adaptability makes it an attractive option for individuals whose financial situations or insurance needs may change over time. If you're looking for a life insurance policy that can evolve with you, universal life might be the perfect fit. But with so many options out there, how do you choose the best one? This comprehensive guide will help you navigate the landscape of universal life insurance, highlighting the top policies for flexibility, comparing their features, and discussing their suitability for various scenarios.

Top 4 Universal Life Insurance Policies for Flexibility

Understanding Universal Life Insurance Key Features and Benefits

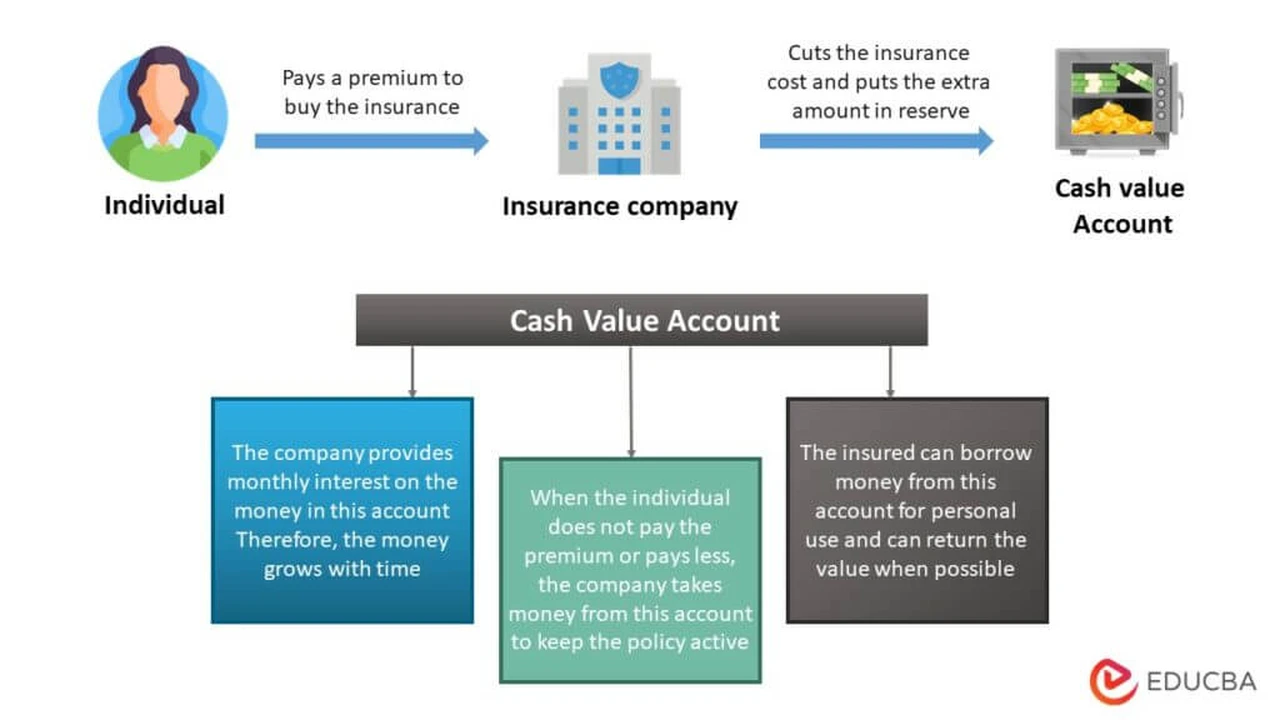

Before diving into specific policies, let's solidify our understanding of what makes universal life insurance so unique. At its core, a UL policy provides lifelong coverage, meaning it doesn't expire as long as premiums are paid. It also accumulates cash value on a tax-deferred basis, which you can access during your lifetime through withdrawals or loans. The real game-changer, however, is its flexibility. You can often adjust your premium payments – within certain limits – to suit your current financial situation. For instance, if you have a particularly good year financially, you might pay more to accelerate cash value growth. Conversely, if times are tough, you might pay less, or even skip a payment, using your accumulated cash value to cover the policy's costs. Similarly, you can often increase or decrease your death benefit, subject to underwriting, to match your evolving protection needs. This adaptability is a significant advantage for many policyholders, especially those with unpredictable incomes or changing family responsibilities.

Types of Universal Life Insurance Exploring Your Options

It's important to note that 'Universal Life' isn't a monolithic product. There are several variations, each with its own nuances:

- Guaranteed Universal Life (GUL): This type prioritizes a guaranteed death benefit and fixed premiums, often for a specified period or even for life, as long as premiums are paid. It offers less cash value growth potential but provides certainty.

- Indexed Universal Life (IUL): IUL policies link their cash value growth to a stock market index (like the S&P 500) without directly investing in the market. This offers potential for higher returns than traditional UL, often with a floor to protect against market downturns and a cap on gains.

- Variable Universal Life (VUL): VUL policies allow you to invest your cash value in sub-accounts that are similar to mutual funds. This offers the highest potential for cash value growth but also carries the most risk, as you can lose money if the investments perform poorly.

- Current Assumption Universal Life (CAUL): This is the most basic form of UL, where the cash value grows based on an interest rate declared by the insurer, which can change over time.

For this article, we'll focus on policies that offer a good balance of flexibility in premiums and death benefits, often leaning towards IUL and CAUL, as GUL is more about guarantees and VUL is more about investment risk.

Top 4 Universal Life Insurance Policies for Flexibility A Detailed Comparison

Let's dive into some of the leading universal life insurance policies known for their flexibility. Please note that specific product names and features can vary by state and insurer, and it's always best to consult with a qualified financial advisor for personalized advice.

1. Pacific Life Pacific Discovery Xelerator IUL

Overview: Pacific Life is a well-respected insurer, and their Pacific Discovery Xelerator IUL is a strong contender for those seeking flexible cash value growth potential. This policy is designed to offer competitive indexed interest credits, allowing your cash value to grow based on the performance of a chosen market index, typically with a floor of 0% to protect against losses and a cap on gains.

Key Features for Flexibility:

- Adjustable Premiums: Policyholders have significant control over their premium payments. You can pay more in good years to maximize cash value accumulation or pay less (or even skip payments) by utilizing the policy's cash value to cover costs during leaner times.

- Flexible Death Benefit: You can increase or decrease your death benefit as your needs change, subject to underwriting for increases. This is ideal for individuals whose family responsibilities or financial obligations evolve.

- Indexed Growth Potential: The IUL component offers the potential for higher cash value growth compared to traditional UL, providing more funds for future flexibility in premium payments or withdrawals.

- Access to Cash Value: Policy loans and withdrawals allow you to access your cash value for various needs, such as supplementing retirement income, funding education, or covering unexpected expenses. This adds another layer of financial flexibility.

Ideal Use Cases:

- Individuals seeking long-term cash value growth with some market upside potential, but also protection against market downturns.

- Those with fluctuating incomes who need the ability to adjust premium payments.

- People looking for a policy that can serve as a supplemental retirement income stream.

- Families whose insurance needs may change over time, requiring adjustments to the death benefit.

Estimated Pricing (Illustrative, highly variable): For a healthy 35-year-old non-smoker, a $500,000 death benefit might have an initial annual premium ranging from $3,000 to $6,000, depending on the chosen index, participation rates, and cap rates. The actual cost will depend on individual health, age, and specific policy design.

2. Transamerica Financial Foundation IUL

Overview: Transamerica is another major player in the life insurance market, and their Financial Foundation IUL is known for its robust features and competitive indexed options. It aims to provide a balance of death benefit protection and cash value accumulation with the flexibility that universal life policies are known for.

Key Features for Flexibility:

- Premium Payment Flexibility: Similar to other IULs, Transamerica's policy allows for adjustable premium payments. You can overfund the policy to build cash value faster or reduce payments when necessary, relying on the cash value to maintain the policy.

- Adjustable Death Benefit: The ability to increase or decrease the death benefit provides crucial flexibility as life circumstances change. This is particularly useful for growing families or individuals whose financial obligations decrease over time.

- Multiple Index Options: Transamerica often offers a variety of index options, allowing policyholders to choose the one that best aligns with their risk tolerance and growth objectives. This customization enhances flexibility in how your cash value grows.

- Living Benefits Riders: Many Transamerica UL policies come with or offer optional living benefits riders (also known as accelerated death benefit riders) that allow you to access a portion of your death benefit early if you experience a qualifying critical, chronic, or terminal illness. This provides significant financial flexibility during challenging health events.

Ideal Use Cases:

- Individuals prioritizing living benefits alongside death benefit protection.

- Those who want control over their cash value growth strategy through various index choices.

- People seeking a policy that can adapt to changing financial situations and health needs.

- Families looking for a comprehensive policy that can provide financial security in multiple scenarios.

Estimated Pricing (Illustrative, highly variable): For a healthy 40-year-old non-smoker, a $750,000 death benefit might have an initial annual premium ranging from $4,500 to $8,000, depending on the chosen index, riders, and policy design. Again, personalized quotes are essential.

3. National Life Group FlexLife II IUL

Overview: National Life Group is well-regarded for its focus on living benefits, and their FlexLife II IUL is a prime example. This policy emphasizes not just the death benefit but also the ability to access funds during your lifetime, making it highly flexible for various life events.

Key Features for Flexibility:

- Strong Living Benefits: National Life Group is a leader in offering robust accelerated death benefit riders for critical, chronic, and terminal illnesses. This means you can access a significant portion of your death benefit while still alive, providing immense financial flexibility if you face a serious health crisis.

- Premium Payment Flexibility: Like other IULs, FlexLife II allows for flexible premium payments, enabling you to adjust contributions based on your financial capacity.

- Adjustable Death Benefit: The policy allows for modifications to the death benefit, ensuring your coverage remains appropriate for your current needs.

- Guaranteed Policy Value Account: This feature provides a guaranteed minimum interest rate on a portion of your cash value, offering a layer of security even with indexed growth potential.

Ideal Use Cases:

- Individuals who prioritize comprehensive living benefits and want the option to access their death benefit for health-related expenses.

- Those concerned about the financial impact of critical or chronic illnesses.

- People seeking a balance of cash value growth potential and guaranteed elements.

- Families looking for a policy that offers both death benefit protection and a safety net for health emergencies.

Estimated Pricing (Illustrative, highly variable): For a healthy 30-year-old non-smoker, a $1,000,000 death benefit might have an initial annual premium ranging from $5,000 to $9,000, depending on the chosen index, rider selections, and policy design. The inclusion of robust living benefits can sometimes influence the premium.

4. Penn Mutual Diversified Advantage UL

Overview: Penn Mutual is a mutual company, meaning it's owned by its policyholders, which often translates to a focus on long-term value and strong customer service. Their Diversified Advantage UL is a current assumption universal life policy that offers competitive interest rates and significant flexibility without the direct market linkage of an IUL.

Key Features for Flexibility:

- Flexible Premiums: This policy allows for highly flexible premium payments. You can pay more or less than the planned premium, or even skip payments, as long as the cash value is sufficient to cover policy charges. This is a hallmark of UL and Penn Mutual excels in this area.

- Adjustable Death Benefit: Policyholders can increase or decrease their death benefit to align with changing life circumstances, providing adaptability over the long term.

- Competitive Interest Rates: Penn Mutual is known for offering competitive declared interest rates on its current assumption UL policies, allowing for steady cash value growth without market volatility.

- Strong Financial Strength: As a mutual company with a long history, Penn Mutual offers a high degree of financial stability, which translates to confidence in the long-term performance and flexibility of their policies.

Ideal Use Cases:

- Individuals who prefer steady, predictable cash value growth over market-linked returns.

- Those who need maximum flexibility in premium payments due to variable income or financial planning needs.

- People looking for a reliable, long-term permanent life insurance solution from a financially strong mutual company.

- Families who value the ability to adjust coverage as their needs evolve without the complexities of indexed or variable options.

Estimated Pricing (Illustrative, highly variable): For a healthy 45-year-old non-smoker, a $600,000 death benefit might have an initial annual premium ranging from $4,000 to $7,500, depending on the declared interest rates and policy design. As always, a personalized quote is crucial.

Choosing the Right Universal Life Policy Factors to Consider

Selecting the best universal life insurance policy involves more than just looking at the top four. Here are crucial factors to weigh:

Your Financial Goals and Risk Tolerance

Are you primarily looking for a guaranteed death benefit, or do you want the potential for higher cash value growth? If you're risk-averse, a GUL or a CAUL with competitive declared rates might be better. If you're comfortable with some market exposure for potentially higher returns, an IUL could be a good fit. VUL is for those who are comfortable with direct investment risk.

Premium Flexibility Needs

How much variability do you anticipate in your income or financial obligations? If your income fluctuates significantly, a policy with maximum premium flexibility will be essential. Understand the minimum and maximum premium limits and how long you can sustain the policy by paying only the minimum or by using cash value to cover costs.

Cash Value Growth Expectations

Do you plan to use the cash value for future needs like retirement income or education funding? If so, the growth potential and access features (loans vs. withdrawals) are critical. Understand the crediting methods (declared interest, indexed, or investment sub-accounts) and their associated risks and rewards.

Living Benefits and Riders

Are living benefits important to you? Many UL policies offer riders for critical, chronic, or terminal illness, allowing early access to the death benefit. Consider if these features align with your health concerns and desire for financial protection during challenging times. Other riders, like a waiver of premium, can also add significant flexibility.

Insurer's Financial Strength and Reputation

Since universal life insurance is a long-term commitment, choose an insurer with a strong financial rating from agencies like A.M. Best, Standard & Poor's, and Moody's. A stable company is more likely to honor its commitments and maintain competitive policy features over decades.

Fees and Charges Understanding the Costs

Universal life policies come with various fees and charges, including mortality charges, administrative fees, and surrender charges. These can impact your cash value growth. Ask for an illustration that clearly breaks down all costs and how they affect your policy's performance over time. Understand the surrender charge schedule, as early termination can result in significant losses.

Policy Illustrations and Projections

Always request detailed policy illustrations from your agent. These projections show how your policy is expected to perform under different scenarios (e.g., current interest rates, guaranteed minimum rates, or various index performances). Pay close attention to the guaranteed values versus the projected values, and understand the assumptions used in the projections.

Universal Life Insurance in Southeast Asia Market Insights

While the policies discussed above are primarily US-centric, the principles of universal life insurance and its flexibility are highly relevant in Southeast Asian markets as well. Countries like Singapore, Malaysia, Thailand, and Vietnam have growing insurance sectors, and universal life products are becoming increasingly popular due to their adaptability.

Key Considerations for Southeast Asian Markets:

- Local Regulations: Insurance regulations vary significantly by country. Ensure any policy you consider complies with local laws and offers the protections you expect.

- Currency and Inflation: Consider the currency of the policy and how local inflation rates might impact the long-term value of the death benefit and cash value.

- Local Providers: While international insurers operate in the region, local providers often have a deeper understanding of the market and may offer tailored products. Research companies like AIA, Prudential, Great Eastern, and Manulife, which have strong presences in Southeast Asia.

- Tax Implications: Understand the tax treatment of life insurance death benefits and cash value growth in your specific country of residence.

- Product Availability: Not all types of universal life (e.g., VUL or specific IUL designs) may be available or as prevalent in every Southeast Asian market.

When exploring universal life insurance in Southeast Asia, focus on policies that offer similar flexibility in premium payments and death benefit adjustments, as these are the core advantages of UL. Look for policies with competitive interest crediting rates (for CAUL) or transparent index-linking mechanisms (for IUL) that align with your financial objectives.

The Bottom Line Is Universal Life Right for You

Universal life insurance, with its inherent flexibility, can be an excellent tool for long-term financial planning. It offers permanent coverage, a cash value component that can grow over time, and the ability to adapt to your changing life circumstances. Whether you're a young professional with an unpredictable income, a growing family needing adjustable coverage, or someone planning for retirement with a need for supplemental income, a UL policy can be tailored to fit. However, it's crucial to understand the different types of UL, compare policies carefully, and work with a knowledgeable financial advisor who can help you design a policy that truly meets your unique needs and goals. Don't just look at the death benefit; consider the cash value growth, the fees, the riders, and the long-term projections to ensure you're making an informed decision for your financial future.

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)