Understanding Whole Life Insurance Its Benefits and Features

A comprehensive overview of whole life insurance, explaining its permanent coverage, cash value, and other key benefits.

A comprehensive overview of whole life insurance, explaining its permanent coverage, cash value, and other key benefits.

Understanding Whole Life Insurance Its Benefits and Features

Life insurance is a cornerstone of sound financial planning, offering peace of mind and financial security for your loved ones. Among the various types of life insurance, whole life insurance stands out as a permanent solution, designed to provide coverage for your entire lifetime. Unlike term life insurance, which covers you for a specific period, whole life insurance offers a guaranteed death benefit and, perhaps its most distinctive feature, a cash value component that grows over time. This article will delve deep into the world of whole life insurance, exploring its core mechanics, key benefits, and essential features. We'll also compare it with other popular options, recommend specific products, and discuss pricing to help you make an informed decision.

What is Whole Life Insurance Exploring Permanent Coverage

At its heart, whole life insurance is a type of permanent life insurance. This means that as long as you pay your premiums, the policy remains in force for your entire life, regardless of your age or health changes. This permanence is a significant advantage for many individuals and families, ensuring that a death benefit will eventually be paid out to your beneficiaries. The death benefit is typically tax-free for your beneficiaries, providing a crucial financial safety net for expenses like funeral costs, outstanding debts, and ongoing living expenses.

The concept of permanent coverage is particularly appealing for long-term financial planning. Imagine you purchase a whole life policy in your 30s. As you age, your health might decline, making it difficult or expensive to obtain new life insurance. With a whole life policy, your coverage is locked in, providing continuous protection without the need for re-qualification or increasing premiums due to age or health deterioration. This predictability is a major draw for those seeking stability in their financial future.

The Cash Value Component Unlocking Financial Growth

One of the most compelling features of whole life insurance is its cash value component. A portion of each premium payment you make goes towards building this cash value, which grows on a tax-deferred basis over the life of the policy. This cash value is not just a savings account; it's a living benefit that you can access during your lifetime. Think of it as a financial reservoir that accumulates over time, offering a range of flexible options.

The growth of the cash value is typically guaranteed by the insurance company, often at a conservative but consistent rate. This predictability contrasts with investment vehicles that are subject to market fluctuations. While the growth might not be as aggressive as some stock market investments, the guaranteed nature provides a stable and reliable source of funds.

Accessing Your Cash Value Loans and Withdrawals

The cash value component offers incredible flexibility. You can access it in several ways:

- Policy Loans: You can borrow against your policy's cash value. The interest rates on these loans are often competitive, and you typically don't need to qualify for them based on your credit score. While the loan reduces the death benefit if not repaid, it offers a convenient and often tax-advantaged way to access funds for various needs, such as a down payment on a home, college tuition, or unexpected emergencies.

- Withdrawals: You can also make withdrawals from your cash value. Unlike loans, withdrawals directly reduce the death benefit and the remaining cash value. If you withdraw more than you've paid in premiums, the excess could be subject to income tax.

- Surrender the Policy: If you decide you no longer need the coverage, you can surrender the policy and receive the accumulated cash value, minus any surrender charges. This option effectively terminates the policy.

The ability to access your cash value provides a powerful financial tool, offering liquidity and flexibility that traditional term life insurance simply cannot match. It transforms your life insurance policy from a simple death benefit into a multi-faceted financial asset.

Guaranteed Premiums and Death Benefit Stability You Can Count On

Another significant benefit of whole life insurance is the predictability it offers. Once you purchase a whole life policy, your premiums are typically fixed and guaranteed for the life of the policy. This means you won't experience unexpected premium increases as you age or if your health deteriorates. This stability makes budgeting easier and provides long-term financial certainty.

Similarly, the death benefit is also guaranteed. Your beneficiaries will receive the stated death benefit amount, provided the policy is in force. This guarantee provides immense peace of mind, knowing that your loved ones will be financially protected, regardless of future circumstances. This contrasts sharply with term life insurance, where the death benefit is only paid if you pass away within the specified term.

Participating vs Non-Participating Whole Life Insurance Understanding Dividends

When exploring whole life insurance, you'll often encounter the terms 'participating' and 'non-participating' policies. This distinction is crucial for understanding how your policy might generate additional value.

- Participating Whole Life Insurance: These policies are offered by mutual insurance companies, which are owned by their policyholders. If the company performs well financially, it may distribute a portion of its profits to policyholders in the form of dividends. These dividends are not guaranteed but can significantly enhance the policy's value over time. Dividends can be used in several ways: to purchase paid-up additions (which increase both the death benefit and cash value), to reduce future premiums, to be taken as cash, or to repay policy loans.

- Non-Participating Whole Life Insurance: These policies are typically offered by stock insurance companies, which are owned by shareholders. They do not pay dividends to policyholders. While they might offer slightly lower initial premiums, they lack the potential for additional growth through dividends.

For many, the potential for dividends from a participating policy is a strong draw, as it can accelerate cash value growth and increase the overall death benefit, providing an additional layer of financial benefit.

Key Features and Riders Customizing Your Whole Life Policy

Whole life insurance policies can be customized with various riders to enhance their coverage and flexibility. These riders allow you to tailor the policy to your specific needs and circumstances. Some common riders include:

- Waiver of Premium Rider: This rider waives your premium payments if you become totally and permanently disabled, ensuring your policy remains in force even if you can't work.

- Accidental Death Benefit Rider: This rider pays an additional death benefit if your death is due to an accident.

- Guaranteed Insurability Rider: This rider allows you to purchase additional coverage at specified future dates without undergoing further medical examinations, regardless of your health.

- Long-Term Care Rider: Some whole life policies offer riders that allow you to access a portion of your death benefit early to cover long-term care expenses. This can be a valuable feature for addressing potential healthcare costs in later life.

- Child Rider: This rider provides a small amount of term life insurance coverage for your children, which can often be converted to a permanent policy later.

Understanding the available riders is crucial for maximizing the value and utility of your whole life insurance policy. They can transform a basic policy into a comprehensive financial tool that addresses a wider range of potential needs.

Whole Life Insurance in Action Practical Use Cases and Scenarios

Whole life insurance is a versatile financial product that can serve various purposes beyond just providing a death benefit. Here are some practical scenarios where whole life insurance shines:

Estate Planning and Wealth Transfer Securing Your Legacy

For individuals focused on estate planning, whole life insurance is an invaluable tool. The guaranteed death benefit can be used to cover estate taxes, ensuring that your heirs receive the full inheritance you intend without having to liquidate other assets. It can also be used to create an immediate estate, providing a substantial sum to your beneficiaries even if you haven't had time to accumulate significant wealth through other means. The tax-free nature of the death benefit further enhances its appeal for wealth transfer.

Business Succession Planning Ensuring Continuity

Business owners can leverage whole life insurance for business succession planning. For example, in a buy-sell agreement, whole life policies can fund the purchase of a deceased partner's share, ensuring a smooth transition and preventing financial disruption for the surviving partners and the business itself. It provides the necessary liquidity to execute the agreement without straining the company's finances.

Supplemental Retirement Income Enhancing Your Golden Years

While not primarily a retirement vehicle, the cash value of a whole life policy can serve as a supplemental source of income during retirement. By taking policy loans or withdrawals, you can access tax-free funds to supplement your other retirement savings. This can be particularly attractive for those seeking an additional layer of financial security and flexibility in their retirement years, especially if other investment vehicles underperform.

Charitable Giving Making a Lasting Impact

Whole life insurance can also be a powerful tool for charitable giving. You can name a charity as the beneficiary of your policy, ensuring a significant donation upon your passing. Alternatively, you can transfer ownership of the policy to a charity, potentially receiving an immediate tax deduction for the cash value and future premium payments.

Comparing Whole Life Insurance with Other Policy Types Making the Right Choice

To truly appreciate the value of whole life insurance, it's helpful to compare it with other common life insurance types:

Whole Life vs Term Life Insurance Permanent vs Temporary Protection

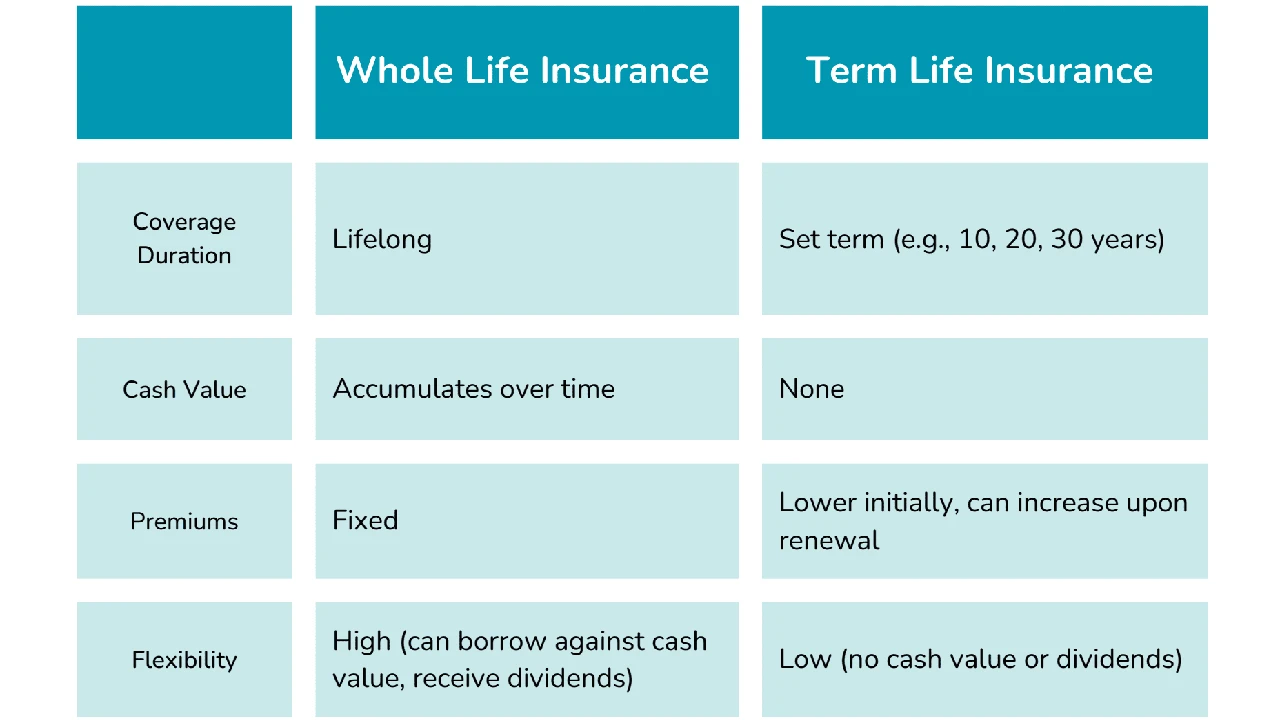

This is perhaps the most fundamental comparison. Term life insurance provides coverage for a specific period (e.g., 10, 20, or 30 years). It's generally more affordable in the short term and is ideal for covering temporary financial obligations like a mortgage or raising young children. However, it has no cash value, and coverage ends when the term expires. Whole life, on the other hand, offers lifelong coverage, guaranteed premiums, and a growing cash value, but comes with higher premiums.

Whole Life vs Universal Life Insurance Fixed vs Flexible Premiums

Universal life insurance is another type of permanent life insurance, but it offers more flexibility than whole life. With universal life, you can often adjust your premium payments and death benefit. The cash value growth is also more variable, often tied to interest rates. While this flexibility can be appealing, it also introduces more complexity and potential for policy lapse if not managed carefully. Whole life offers greater predictability with its fixed premiums and guaranteed cash value growth.

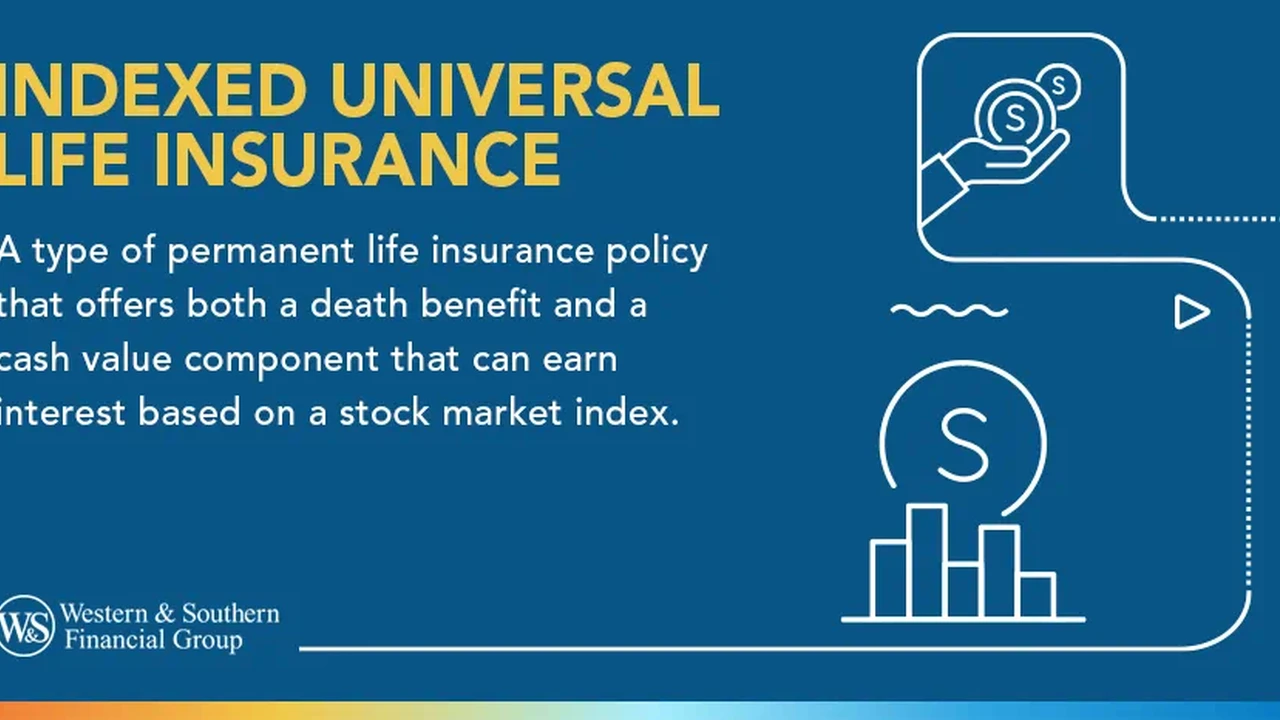

Whole Life vs Indexed Universal Life Insurance Guaranteed vs Market Linked Growth

Indexed universal life (IUL) insurance is a type of universal life policy where the cash value growth is linked to a stock market index (like the S&P 500), but with a floor (guaranteed minimum return) and a cap (maximum return). This offers the potential for higher cash value growth than whole life, but also introduces more volatility and complexity. Whole life provides guaranteed, albeit more conservative, growth, which appeals to those who prioritize stability over potentially higher, but riskier, returns.

Recommended Whole Life Insurance Products and Providers A Look at the Market

Choosing the right whole life insurance policy involves considering various factors, including the insurer's financial strength, customer service, dividend history (for participating policies), and available riders. Here are a few highly-rated providers and their notable whole life offerings, keeping in mind that specific product names and features can vary by state and region:

Northwestern Mutual Whole Life Insurance

- Key Features: Northwestern Mutual is a mutual company known for its strong financial ratings and consistent dividend payouts. Their whole life policies are highly regarded for their robust cash value growth and long-term stability. They offer a range of policies with various payment structures and riders.

- Use Case: Excellent for individuals seeking a reliable, long-term financial asset with strong dividend potential and a focus on wealth accumulation and estate planning.

- Pricing: Generally considered to be on the higher end of the premium spectrum, reflecting the strong guarantees and dividend performance.

MassMutual Whole Life Insurance

- Key Features: Another leading mutual company with a long history of strong financial performance and competitive dividends. MassMutual offers flexible whole life options, including policies with accelerated death benefit riders for critical or chronic illness.

- Use Case: Ideal for those who value a strong, stable company with a history of paying dividends and who might be interested in riders that provide living benefits.

- Pricing: Competitive within the participating whole life market, offering good value for the guarantees and potential dividends.

Guardian Whole Life Insurance

- Key Features: Guardian is a well-respected mutual company known for its personalized service and strong whole life products. They offer a variety of whole life policies designed to meet different financial goals, with a focus on guaranteed growth and dividend potential.

- Use Case: Suited for individuals and families looking for a personalized approach to financial planning with a focus on guaranteed growth and a strong customer service experience.

- Pricing: Premiums are generally in line with other top-tier mutual companies, reflecting the quality of the product and service.

New York Life Whole Life Insurance

- Key Features: New York Life is one of the largest and oldest mutual life insurance companies in the US, with an impeccable financial strength rating. Their whole life policies are known for their strong guarantees, consistent dividend performance, and a wide array of riders.

- Use Case: An excellent choice for individuals seeking maximum financial security and a proven track record of performance, particularly for long-term wealth accumulation and estate planning.

- Pricing: Premiums are competitive for the level of guarantees and dividend potential offered by a company of New York Life's stature.

Important Note on Pricing: The actual cost of a whole life insurance policy depends on numerous factors, including your age, health, gender, lifestyle, the death benefit amount, and any riders you choose. It's crucial to obtain personalized quotes from multiple providers to get an accurate understanding of your potential premiums. Generally, whole life insurance premiums are higher than term life insurance premiums for the same death benefit, due to the permanent coverage and cash value component.

Factors Influencing Whole Life Insurance Premiums Understanding the Cost

Several factors determine the premium you'll pay for a whole life insurance policy. Understanding these can help you anticipate costs and potentially find ways to manage them:

- Age: The younger you are when you purchase a policy, the lower your premiums will generally be. This is because the insurer has a longer period to collect premiums and the risk of payout is further in the future.

- Health: Your current health status, medical history, and family health history play a significant role. Healthier individuals typically receive lower premiums.

- Gender: Statistically, women tend to live longer than men, so they often pay lower life insurance premiums.

- Lifestyle: Factors like smoking, alcohol consumption, and participation in high-risk hobbies (e.g., skydiving, scuba diving) can increase your premiums.

- Death Benefit Amount: The higher the death benefit you choose, the higher your premiums will be.

- Riders: Adding riders to your policy will increase the premium, as they provide additional benefits or coverage.

- Insurance Company: Different insurance companies have different underwriting guidelines and pricing structures, leading to variations in premiums for similar coverage.

It's always advisable to work with a qualified financial advisor or insurance agent who can help you navigate these factors and find a policy that aligns with your budget and financial goals.

The Role of Whole Life Insurance in a Diversified Financial Portfolio Long-Term Strategy

While whole life insurance offers guaranteed growth and stability, it's important to view it as one component of a diversified financial portfolio. It's not typically designed to be your sole investment vehicle, but rather a complementary asset that provides unique benefits.

For many, whole life insurance serves as a conservative, long-term savings vehicle with guaranteed returns, offering a counterbalance to more volatile investments like stocks. Its tax-deferred cash value growth and tax-free death benefit make it an attractive option for those seeking to build a secure financial foundation and protect their legacy. When integrated thoughtfully into a broader financial plan, whole life insurance can provide unparalleled peace of mind and financial resilience for you and your loved ones.

Ultimately, whole life insurance is a powerful and enduring financial tool. Its permanent coverage, guaranteed premiums, and growing cash value offer a unique blend of protection and financial flexibility. By understanding its benefits, features, and how it compares to other options, you can determine if whole life insurance is the right choice to secure your financial future and provide lasting peace of mind for your family.

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)