Whole Life Insurance for Estate Planning in the US

Discover how whole life insurance can be effectively used for estate planning purposes in the United States.

Discover how whole life insurance can be effectively used for estate planning purposes in the United States. It's a powerful tool, offering guaranteed growth, tax advantages, and liquidity for your heirs. Let's dive into how this financial product can secure your legacy.

Whole Life Insurance for Estate Planning in the US

Understanding Whole Life Insurance The Foundation of Your Estate Plan

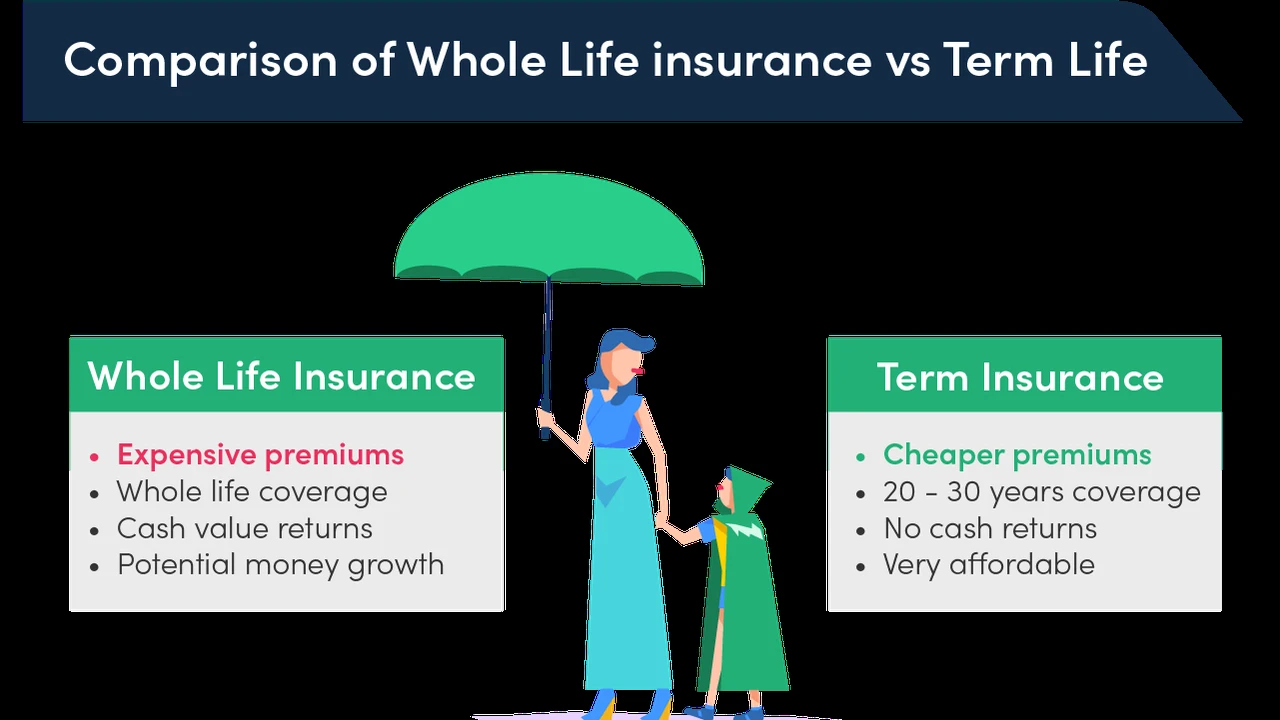

Whole life insurance is a type of permanent life insurance that provides coverage for your entire life, as long as premiums are paid. Unlike term life insurance, which covers you for a specific period, whole life policies build cash value over time. This cash value grows on a tax-deferred basis and can be accessed during your lifetime through loans or withdrawals. The death benefit, which is typically tax-free for beneficiaries, is guaranteed to be paid out upon your passing. This combination of guaranteed death benefit, cash value growth, and tax advantages makes whole life insurance a cornerstone for many estate plans in the US.

Guaranteed Death Benefit Ensuring Your Legacy

The primary benefit of whole life insurance in estate planning is its guaranteed death benefit. This means that no matter when you pass away, your beneficiaries will receive a predetermined sum of money. This is crucial for estate planning because it provides immediate liquidity to your heirs. They can use this money to cover estate taxes, pay off debts, or simply provide financial support, ensuring your legacy is protected and your wishes are fulfilled without burdening them with financial stress. For example, if you have a large estate that might be subject to federal estate taxes (which can be substantial), a whole life policy can provide the funds to pay these taxes, preventing your heirs from having to sell off assets, like a family business or real estate, to cover the tax bill.

Cash Value Growth A Living Benefit for Your Estate

Beyond the death benefit, the cash value component of whole life insurance offers significant advantages for estate planning. This cash value grows at a guaranteed rate, providing a predictable and stable asset within your estate. You can access this cash value during your lifetime for various purposes, such as supplementing retirement income, funding a child's education, or even starting a business. While accessing the cash value reduces the death benefit, it provides a flexible financial resource that can be strategically used to enhance your overall estate plan. For instance, if you face unexpected medical expenses late in life, you can tap into the cash value rather than depleting other estate assets.

Tax Advantages Maximizing Your Estate's Value

Whole life insurance offers several tax advantages that are highly beneficial for estate planning in the US. The cash value grows tax-deferred, meaning you don't pay taxes on the growth until you withdraw it. Furthermore, the death benefit is generally paid out to your beneficiaries income tax-free. This can be a significant advantage, especially for larger estates where minimizing tax liabilities is a key concern. By strategically structuring your whole life policy, you can ensure that more of your wealth is passed on to your heirs, rather than being eroded by taxes.

Specific Use Cases for Whole Life Insurance in US Estate Planning

Whole life insurance isn't a one-size-fits-all solution, but its versatility makes it suitable for various estate planning scenarios. Let's explore some common and effective ways it's utilized.

Covering Estate Taxes and Debts Providing Liquidity

One of the most common and critical uses of whole life insurance in estate planning is to provide liquidity for estate taxes and other final expenses. When a person with a substantial estate passes away, their heirs may face significant federal and state estate taxes, as well as other costs like probate fees, legal expenses, and outstanding debts. Without sufficient liquid assets, heirs might be forced to sell valuable assets, such as real estate, a family business, or cherished heirlooms, often at a discount, to cover these costs. A whole life insurance policy, with its guaranteed tax-free death benefit, can provide the immediate cash needed to pay these expenses, preserving the integrity of the estate and ensuring that assets are passed down as intended. This is particularly important for illiquid estates, where most of the wealth is tied up in non-cash assets.

Equalizing Inheritances Fair Distribution for All Heirs

In situations where an estate includes a family business or a primary residence that one child wishes to inherit, while other children are not interested or involved, whole life insurance can be used to equalize inheritances. For example, if one child is taking over the family business, which represents a significant portion of the estate's value, a whole life policy can be purchased to provide a death benefit equal to the value of the business for the other children. This ensures that all heirs receive a fair share of the estate, preventing potential family disputes and maintaining harmony. It allows for the smooth transition of specific assets to specific heirs without creating an imbalance in overall inheritance.

Charitable Giving Leaving a Lasting Impact

Whole life insurance can be an excellent tool for charitable giving, allowing you to leave a substantial legacy to your favorite causes. You can name a charity as the beneficiary of your whole life policy, ensuring they receive a significant donation upon your passing. Alternatively, you can transfer ownership of an existing policy to a charity, potentially receiving an immediate income tax deduction for the cash value and future premium payments. This strategy allows you to make a larger gift than you might be able to afford during your lifetime, amplifying your philanthropic impact. It's a way to support causes you care about deeply, long after you're gone.

Funding a Special Needs Trust Protecting Vulnerable Loved Ones

For individuals with special needs dependents, whole life insurance can be used to fund a special needs trust. A special needs trust is designed to provide for the financial needs of a disabled individual without jeopardizing their eligibility for government benefits like Medicaid or Supplemental Security Income (SSI). By naming the special needs trust as the beneficiary of a whole life policy, you can ensure that a substantial sum of money is available to the trust upon your death, providing ongoing care and support for your loved one without disrupting their essential benefits. This offers peace of mind, knowing that your vulnerable family member will be cared for financially.

Business Succession Planning Ensuring Continuity

For business owners, whole life insurance plays a vital role in succession planning. It can be used to fund buy-sell agreements, which are contracts that dictate how a deceased or disabled owner's share of a business will be bought out by the remaining partners or the business itself. The death benefit from a whole life policy provides the necessary funds to execute the buy-sell agreement, ensuring a smooth transition of ownership, preventing financial strain on the surviving partners, and providing fair compensation to the deceased owner's family. This is crucial for maintaining business continuity and stability.

Comparing Whole Life Insurance Products for Estate Planning

When considering whole life insurance for estate planning, it's important to look at different providers and their offerings. While the core features are similar, variations in dividends, riders, and customer service can make a difference. Here are a few prominent providers and what they bring to the table, along with hypothetical pricing scenarios. Please note that actual premiums will vary significantly based on age, health, policy amount, and other factors. These are illustrative examples.

Northwestern Mutual Whole Life Insurance

Northwestern Mutual is renowned for its strong financial ratings and consistent dividend payments. Their whole life policies are participating, meaning policyholders can receive dividends, which can be used to reduce premiums, purchase paid-up additions (increasing cash value and death benefit), or taken as cash. This dividend feature can significantly enhance the long-term value of the policy for estate planning.

* **Key Features for Estate Planning:** Strong dividend history, guaranteed cash value growth, excellent financial strength, personalized service.

* **Use Case:** Ideal for individuals seeking a highly stable and reliable policy with potential for enhanced growth through dividends, especially for large estates requiring substantial liquidity.

* **Hypothetical Scenario (Illustrative):** A healthy 45-year-old male seeking a $1,000,000 whole life policy might pay around $10,000 - $12,000 annually. Over 20 years, the cash value could grow significantly, and the death benefit would be guaranteed. Dividends could further increase the death benefit or reduce out-of-pocket costs.

MassMutual Whole Life Insurance

MassMutual is another highly-rated mutual company known for its competitive whole life products and strong dividend performance. They offer a variety of riders that can be customized to specific estate planning needs, such as a long-term care rider or a waiver of premium rider.

* **Key Features for Estate Planning:** Competitive dividends, strong financial stability, flexible riders, focus on policyholder value.

* **Use Case:** Suitable for those who value a mutual company structure and want options to customize their policy with riders that address potential future needs, such as long-term care, while securing their estate.

* **Hypothetical Scenario (Illustrative):** A healthy 45-year-old male seeking a $1,000,000 whole life policy might pay around $9,800 - $11,800 annually. Their dividend scale is also very competitive, contributing to robust cash value and death benefit growth.

Guardian Whole Life Insurance

Guardian is a mutual company with a long history of financial strength and a focus on providing value to policyholders. Their whole life policies are known for their strong guarantees and competitive dividend rates, making them a solid choice for long-term estate planning.

* **Key Features for Estate Planning:** Strong guarantees, competitive dividends, excellent customer service, robust financial health.

* **Use Case:** A good fit for individuals prioritizing strong guarantees and a reliable company for their estate planning needs, especially if they anticipate needing policy loans in the future due to favorable loan terms.

* **Hypothetical Scenario (Illustrative):** A healthy 45-year-old male seeking a $1,000,000 whole life policy might pay around $9,900 - $11,900 annually. Guardian's policies are often praised for their predictable performance.

New York Life Whole Life Insurance

New York Life is one of the largest and most respected mutual life insurance companies in the US. They offer a range of whole life products designed to meet various financial goals, including estate planning. Their policies are known for their strong guarantees and consistent performance.

* **Key Features for Estate Planning:** High financial strength ratings, guaranteed cash value and death benefit, consistent dividend payments, wide range of policy options.

* **Use Case:** Excellent for those seeking the utmost security and reliability from a top-tier mutual company, particularly for complex estate plans requiring sophisticated solutions.

* **Hypothetical Scenario (Illustrative):** A healthy 45-year-old male seeking a $1,000,000 whole life policy might pay around $10,100 - $12,100 annually. New York Life's reputation for stability is a major draw for estate planners.

State Farm Whole Life Insurance

State Farm, while also known for its property and casualty insurance, offers competitive whole life insurance products. They are a good option for those who prefer to consolidate their insurance needs with a single, well-known provider and value local agent support.

* **Key Features for Estate Planning:** Strong brand recognition, local agent support, guaranteed cash value and death benefit, straightforward policy options.

* **Use Case:** Ideal for individuals who prefer working with a local agent and want a reliable, easy-to-understand whole life policy as part of their broader financial and estate plan.

* **Hypothetical Scenario (Illustrative):** A healthy 45-year-old male seeking a $1,000,000 whole life policy might pay around $10,500 - $12,500 annually. While not a mutual company, State Farm offers competitive rates and strong service.

Advanced Strategies Integrating Whole Life Insurance into Your Estate Plan

Beyond the basic applications, whole life insurance can be integrated into more sophisticated estate planning strategies to maximize its benefits.

Irrevocable Life Insurance Trusts ILITs for Tax Efficiency

One of the most powerful estate planning tools involving whole life insurance is the Irrevocable Life Insurance Trust (ILIT). An ILIT is an irrevocable trust that owns your life insurance policy. When you place a whole life policy into an ILIT, the death benefit is removed from your taxable estate. This means that upon your death, the death benefit is paid directly to the trust, and then distributed to your beneficiaries according to the trust's terms, completely free of estate taxes. This can save your heirs a significant amount of money, especially for large estates that would otherwise face substantial estate tax liabilities. The ILIT also provides creditor protection for the policy's cash value and death benefit. It's a sophisticated strategy that requires careful planning with an estate attorney.

Wealth Transfer Strategies Leveraging Cash Value

Whole life insurance can be used in various wealth transfer strategies. For instance, you can use the cash value of a policy to make tax-free gifts to heirs during your lifetime, reducing the size of your taxable estate. Alternatively, the policy itself can be gifted to an heir, transferring the future death benefit and cash value growth. These strategies, when implemented correctly, can help you transfer wealth efficiently and minimize future tax burdens for your beneficiaries. It's about using the policy's features to your advantage to move assets across generations.

Generation Skipping Transfer GST Tax Planning

For individuals looking to transfer wealth to grandchildren or later generations, whole life insurance can be a component of Generation-Skipping Transfer (GST) tax planning. By structuring policies within trusts designed to skip a generation, you can potentially avoid estate taxes at each generational level, maximizing the amount of wealth that ultimately reaches your intended beneficiaries. This is a complex area of tax law, and professional guidance is essential to ensure compliance and effectiveness.

Important Considerations When Using Whole Life Insurance for Estate Planning

While whole life insurance offers numerous benefits for estate planning, it's crucial to be aware of certain considerations to ensure it aligns with your overall financial goals.

Cost of Premiums Long Term Commitment

Whole life insurance premiums are generally higher than those for term life insurance, especially in the initial years. This is because whole life policies offer lifelong coverage and build cash value. It's important to ensure that you can comfortably afford the premiums for the long term, as lapsing a policy can lead to financial losses. Consider your budget and long-term financial stability before committing to a whole life policy.

Complexity and Professional Advice Navigating the Nuances

Estate planning, especially when incorporating whole life insurance and trusts like ILITs, can be complex. It's highly recommended to work with a qualified financial advisor, an estate planning attorney, and a tax professional. These experts can help you assess your specific needs, design a comprehensive estate plan, choose the right whole life policy, and ensure that all legal and tax implications are properly addressed. Don't try to navigate these waters alone.

Inflation and Rate of Return Keeping Pace with the Economy

While whole life insurance offers guaranteed cash value growth, the rate of return might be lower compared to other investment vehicles, especially during periods of high inflation. It's important to view whole life insurance as a foundational component of your estate plan, providing guarantees and liquidity, rather than solely as a high-growth investment. A balanced approach, combining whole life with other investments, is often the most effective strategy.

Policy Riders Customizing Your Coverage

Many whole life policies offer various riders that can enhance or customize your coverage. For estate planning, riders like a waiver of premium (which waives premiums if you become disabled) or a guaranteed insurability rider (allowing you to purchase additional coverage without further medical exams) can be valuable. Discuss available riders with your advisor to see which ones best fit your estate planning objectives.

Making Whole Life Insurance Work for Your Estate

Whole life insurance is a powerful and versatile tool for estate planning in the United States. Its guaranteed death benefit provides essential liquidity for estate taxes and debts, ensuring your legacy is preserved. The tax-deferred cash value growth offers a living benefit that can be accessed during your lifetime, while its tax-free death benefit maximizes the wealth passed to your heirs. Whether you're looking to equalize inheritances, fund a special needs trust, or implement advanced tax-efficient strategies with an ILIT, whole life insurance can play a crucial role. Remember to work with experienced professionals to tailor a plan that meets your unique needs and secures your family's financial future.

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)