Whole Life Insurance Premiums What to Expect

An explanation of how whole life insurance premiums are calculated and what factors influence their cost.

An explanation of how whole life insurance premiums are calculated and what factors influence their cost.

Whole Life Insurance Premiums What to Expect

So, you're looking into whole life insurance, huh? That's a smart move for long-term financial security. But let's be real, one of the first things on everyone's mind is, 'How much is this going to cost me?' Whole life insurance premiums can seem a bit mysterious, but once you understand how they're calculated and what factors play a role, it all becomes much clearer. We're going to break down everything you need to know about whole life insurance premiums, from the basics of how they're set to the specific things that can make them go up or down. We'll even look at some real-world examples and popular products to give you a better idea of what to expect.

Understanding the Basics of Whole Life Insurance Premiums

Unlike term life insurance, which covers you for a specific period, whole life insurance provides coverage for your entire life. This permanence is a big reason why whole life premiums are generally higher than term premiums for the same death benefit. But here's the cool part: whole life premiums are typically fixed. That means once you lock in your rate, it usually stays the same for as long as you pay it. No surprises down the road! This predictability is a huge draw for many people, especially those who like to budget and plan for the long haul.

So, what exactly are you paying for with a whole life premium? It's not just the death benefit. A portion of your premium goes towards the cost of insurance, which covers the actual risk of paying out the death benefit. Another significant chunk goes into the policy's cash value. This cash value grows over time on a tax-deferred basis and can be accessed later through loans or withdrawals. Think of it as a savings component built right into your insurance policy. Finally, a small part of your premium covers administrative costs and commissions.

Key Factors Influencing Your Whole Life Insurance Premiums

When an insurance company calculates your whole life premium, they're essentially assessing the risk of insuring you. The higher the perceived risk, the higher your premium will likely be. Here are the main factors they consider:

Your Age and Whole Life Insurance Costs

This is probably the biggest factor. The younger you are when you purchase a whole life policy, the lower your premiums will be. Why? Because you're statistically less likely to pass away in the near future, giving the insurance company more time to collect premiums and for your cash value to grow. Waiting even a few years can significantly increase your premium, so if you're considering whole life, earlier is almost always better.

Your Health and Medical History Impact on Premiums

Your current health and medical history play a crucial role. Insurers will typically ask you to undergo a medical exam and review your medical records. They'll look for things like chronic conditions (diabetes, heart disease), past surgeries, and family medical history. The healthier you are, the lower your risk, and thus, the lower your premium. If you have pre-existing conditions, you might still get coverage, but your premiums will likely be higher to reflect the increased risk.

Gender and Whole Life Insurance Rates

Generally, women tend to have lower whole life insurance premiums than men. This isn't about discrimination; it's based on actuarial data showing that women, on average, have a longer life expectancy than men. So, from an insurer's perspective, they'll be collecting premiums from women for a longer period.

Lifestyle Choices and Whole Life Premiums

Your lifestyle habits can definitely impact your premiums. Smoking is a huge one – smokers almost always pay significantly more for life insurance. Other factors like heavy alcohol consumption, participation in dangerous hobbies (skydiving, car racing), or even certain occupations can lead to higher premiums. Insurers want to know if you're taking on extra risks in your daily life.

The Death Benefit Amount Your Coverage Level

This one is pretty straightforward: the more coverage you want (i.e., the higher the death benefit), the higher your premium will be. A $500,000 policy will cost more than a $250,000 policy, assuming all other factors are equal. It's important to calculate how much coverage you truly need to avoid overpaying or being underinsured.

Riders and Additional Features Customizing Your Policy

Whole life policies can often be customized with riders, which are optional add-ons that provide extra benefits. Common riders include a waiver of premium (if you become disabled, the insurer pays your premiums), an accidental death benefit, or a long-term care rider. While these can add valuable protection, they will also increase your premium. It's a trade-off between comprehensive coverage and cost.

The Insurance Company You Choose Provider Differences

Not all insurance companies are created equal, and their pricing models can vary. Some companies might specialize in certain demographics or have different underwriting guidelines, leading to variations in premiums for the same coverage. It's always a good idea to get quotes from multiple reputable insurers to compare rates.

How Whole Life Premiums Are Calculated A Deeper Dive

Let's get a little more technical, but still keep it easy to understand. Insurance companies use complex actuarial tables and statistical models to determine premiums. They essentially look at a large pool of people with similar characteristics (age, health, gender) and calculate the probability of a death occurring within that group. This helps them determine the 'cost of insurance' component.

Then, they factor in the investment component. A portion of your premium is invested by the insurance company, and the returns from these investments help offset the cost of insurance and contribute to your cash value growth. This is why whole life policies often come with guaranteed cash value growth rates.

Finally, they add in their operating expenses, such as administrative costs, marketing, and agent commissions. All these pieces come together to form your fixed, level premium. The goal is to set a premium that is sufficient to cover future claims, grow the cash value, and cover operational costs, while still being competitive in the market.

Comparing Whole Life Insurance Products and Premiums

To give you a better idea, let's look at some popular whole life insurance products and how their premiums might compare. Keep in mind these are illustrative examples, and actual premiums will vary based on your specific profile.

Mutual of Omaha Whole Life Insurance

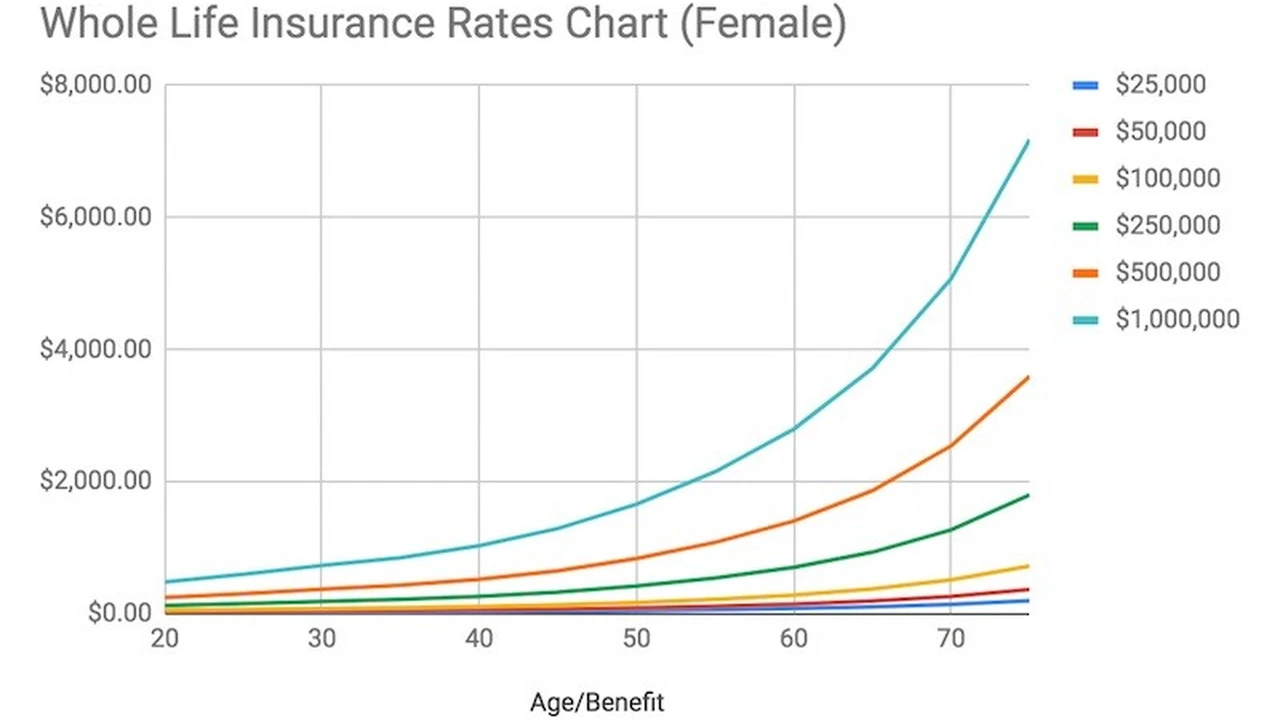

Mutual of Omaha is a well-known provider, especially for guaranteed whole life options. Their 'Living Promise Whole Life Insurance' is often marketed towards seniors or those looking for simplified underwriting. For a 60-year-old non-smoking male in good health, a $25,000 policy might have a monthly premium in the range of $80-$120. For a 30-year-old non-smoking female, a $100,000 policy could be around $70-$100 per month. The key here is the 'guaranteed' aspect, meaning less stringent health questions, which can sometimes lead to slightly higher premiums compared to fully underwritten policies for younger, healthier individuals, but offers accessibility for others.

MassMutual Whole Life Insurance

MassMutual is a mutual company, meaning it's owned by its policyholders, and they are known for their participating whole life policies that pay dividends. These dividends can be used to reduce premiums, purchase paid-up additions (which increase your death benefit and cash value), or taken as cash. For a 35-year-old non-smoking male in excellent health, a $250,000 participating whole life policy might start with a monthly premium of $250-$350. While the initial premium might seem higher, the potential for dividends to offset costs or grow your policy value is a significant benefit. This type of policy is often favored by those looking for long-term wealth accumulation and stability.

New York Life Whole Life Insurance

Another strong mutual company, New York Life also offers participating whole life insurance with a strong track record of paying dividends. Their policies are often praised for their financial strength and guarantees. For a 40-year-old non-smoking female in good health, a $500,000 whole life policy could have a monthly premium ranging from $500-$700. Again, the dividend potential is a key feature here, allowing policyholders to benefit from the company's financial performance. These policies are often chosen by individuals focused on estate planning, business succession, or maximizing tax-advantaged cash value growth.

Northwestern Mutual Whole Life Insurance

Northwestern Mutual is consistently ranked among the top life insurance companies for financial strength and customer satisfaction. They also offer participating whole life policies with a long history of strong dividend payouts. For a 25-year-old non-smoking male in excellent health, a $1,000,000 whole life policy might have a monthly premium of $700-$1,000. This higher coverage amount reflects a common use case for Northwestern Mutual policies – significant wealth transfer and long-term financial planning. The focus here is on maximizing guaranteed growth and dividend potential over many decades.

Guardian Life Whole Life Insurance

Guardian is another mutual company known for its robust whole life products and competitive dividends. They offer various whole life options, including those with enhanced cash value growth. For a 50-year-old non-smoking male in good health, a $200,000 whole life policy might have a monthly premium of $300-$450. Guardian's policies are often chosen for their strong guarantees and the ability to customize with various riders, making them suitable for a range of financial goals, from basic protection to advanced estate planning.

Strategies to Potentially Lower Your Whole Life Premiums

While whole life premiums are fixed, there are things you can do to ensure you're getting the best possible rate when you apply:

Apply When You Are Younger and Healthier

As we discussed, age and health are paramount. The earlier you apply, the lower your premiums will be for life. If you're in your 20s or 30s and considering whole life, now is likely the best time to lock in those lower rates.

Maintain a Healthy Lifestyle for Better Rates

Quitting smoking, maintaining a healthy weight, and managing any existing health conditions can significantly improve your health rating and reduce your premiums. Even if you're not perfectly healthy, showing a commitment to improving your health can sometimes lead to better offers.

Shop Around and Compare Quotes from Multiple Insurers

Don't just go with the first quote you get. Different companies have different underwriting philosophies and pricing structures. Working with an independent agent who can shop multiple carriers for you is often the best way to find the most competitive rates for your specific situation.

Consider a Smaller Death Benefit if Appropriate

While you want adequate coverage, don't over-insure yourself. Calculate your actual needs carefully. A smaller death benefit will naturally lead to lower premiums. You can always add more coverage later if your needs change, though new policies will be based on your age and health at that time.

Explore Participating vs Non-Participating Policies

Participating policies (offered by mutual companies) pay dividends, which can effectively reduce your out-of-pocket premium costs over time if you choose to use the dividends for that purpose. Non-participating policies typically have lower initial premiums but don't offer dividends. Consider which structure aligns better with your financial goals.

The Long-Term Value of Fixed Whole Life Premiums

One of the most compelling aspects of whole life insurance is the fixed premium. In a world where costs for almost everything seem to constantly rise, knowing that your life insurance premium will never increase provides incredible peace of mind. This predictability makes budgeting easier and ensures that your coverage remains affordable throughout your lifetime, even as you age and your health might decline. It's a long-term commitment, but one that offers significant stability and guaranteed benefits.

Beyond the fixed premium, the cash value component of whole life insurance is a powerful tool. It grows steadily, tax-deferred, and can be accessed for various needs – whether it's for a down payment on a house, funding a child's education, or supplementing retirement income. The ability to borrow against your policy's cash value, often at favorable rates and without impacting your credit score, adds another layer of financial flexibility that many other financial products don't offer.

So, while the initial premiums for whole life insurance might seem higher than term insurance, it's crucial to look at the bigger picture. You're not just buying a death benefit; you're investing in a financial product with guaranteed growth, tax advantages, and lifelong coverage. Understanding how these premiums are calculated and what factors influence them empowers you to make an informed decision that aligns with your long-term financial goals.

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)