Whole Life vs Universal Life Insurance A Comparison

Explore the differences between whole life and universal life insurance to help you choose the best permanent coverage.

Explore the differences between whole life and universal life insurance to help you choose the best permanent coverage.

Whole Life vs Universal Life Insurance A Comparison

Navigating the world of life insurance can feel a bit like trying to solve a complex puzzle, especially when you're looking for permanent coverage. You've probably heard terms like 'whole life' and 'universal life' thrown around, and while they both offer lifelong protection, they're far from identical. Understanding their nuances is key to picking the policy that truly fits your financial goals and lifestyle. Let's dive deep into these two popular options, breaking down what makes them tick, how they differ, and which one might be your best bet.

Understanding Permanent Life Insurance What It Means for You

Before we get into the nitty-gritty of whole versus universal, let's clarify what 'permanent life insurance' actually means. Unlike term life insurance, which covers you for a specific period (say, 10, 20, or 30 years), permanent life insurance is designed to last your entire life, as long as premiums are paid. It also typically includes a cash value component that grows over time on a tax-deferred basis. This cash value can be accessed during your lifetime through loans or withdrawals, offering a living benefit that term insurance doesn't. This dual benefit – a death benefit for your loved ones and a cash value you can use – is a major draw for many people.

Whole Life Insurance The Traditional Choice for Stability and Guarantees

Whole life insurance is often considered the most traditional form of permanent life insurance. Think of it as the steady, predictable option. When you purchase a whole life policy, you're essentially locking in a level premium that will never change, regardless of your age or health. This predictability is a huge comfort for many policyholders. The death benefit is also guaranteed, meaning your beneficiaries will receive a predetermined amount when you pass away. But the guarantees don't stop there.

Guaranteed Cash Value Growth and Dividends Whole Life Benefits

A significant feature of whole life insurance is its guaranteed cash value growth. This cash value accumulates at a fixed, predetermined rate, and it's guaranteed not to decrease. This makes whole life a very low-risk savings vehicle. Additionally, many whole life policies are 'participating,' meaning they may pay dividends to policyholders. While dividends aren't guaranteed, they can be a nice bonus, and you typically have several options for how to use them: you can take them as cash, use them to reduce your premiums, let them accumulate with interest, or use them to purchase paid-up additions (which increase your death benefit and cash value).

Pros and Cons of Whole Life Insurance Is It Right for You

Pros:

- Guaranteed Premiums: Your premium payments remain the same for life.

- Guaranteed Death Benefit: Your beneficiaries are assured a specific payout.

- Guaranteed Cash Value Growth: The cash value grows at a fixed rate and is guaranteed.

- Potential for Dividends: Participating policies may offer additional returns.

- Simplicity: It's generally easier to understand and manage than more complex policies.

Cons:

- Less Flexible: Premiums and death benefits are fixed, offering little room for adjustment.

- Higher Initial Premiums: Often more expensive than universal life insurance in the early years.

- Lower Growth Potential: Cash value growth is conservative compared to market-linked options.

Universal Life Insurance The Flexible Option for Changing Needs

Universal life (UL) insurance, on the other hand, is known for its flexibility. If your financial situation or needs are likely to change over time, a UL policy might be more appealing. With UL, you have the ability to adjust your premium payments and even your death benefit, within certain limits. This adaptability is its defining characteristic.

Adjustable Premiums and Death Benefits Universal Life Flexibility

One of the biggest draws of universal life is the ability to vary your premium payments. As long as your cash value is sufficient to cover policy charges, you can pay more than the minimum premium (to build cash value faster) or less (even skipping payments if needed). You can also increase or decrease your death benefit, though increasing it usually requires additional underwriting. This flexibility can be incredibly valuable if you anticipate fluctuating income or changing family responsibilities.

Cash Value Growth in Universal Life How It Works

The cash value in a universal life policy typically grows based on an interest rate declared by the insurer. This rate can change over time, but there's usually a guaranteed minimum interest rate. Some UL policies, like Indexed Universal Life (IUL) or Variable Universal Life (VUL), offer more dynamic cash value growth potential, linked to market indices or investment sub-accounts, respectively. This can lead to higher returns but also comes with greater risk.

Pros and Cons of Universal Life Insurance Is It Your Best Fit

Pros:

- Flexible Premiums: Ability to adjust premium payments.

- Adjustable Death Benefit: Can increase or decrease coverage as needed.

- Potential for Higher Cash Value Growth: Especially with IUL or VUL policies.

- Transparency: Policy charges and interest rates are often clearly stated.

Cons:

- More Complex: Requires more active management and understanding.

- Interest Rate Risk: Cash value growth can fluctuate with declared interest rates (for traditional UL).

- Potential for Policy Lapse: If cash value isn't sufficient to cover charges, the policy could lapse.

- Higher Fees: Some UL policies, especially VUL, can have higher fees and charges.

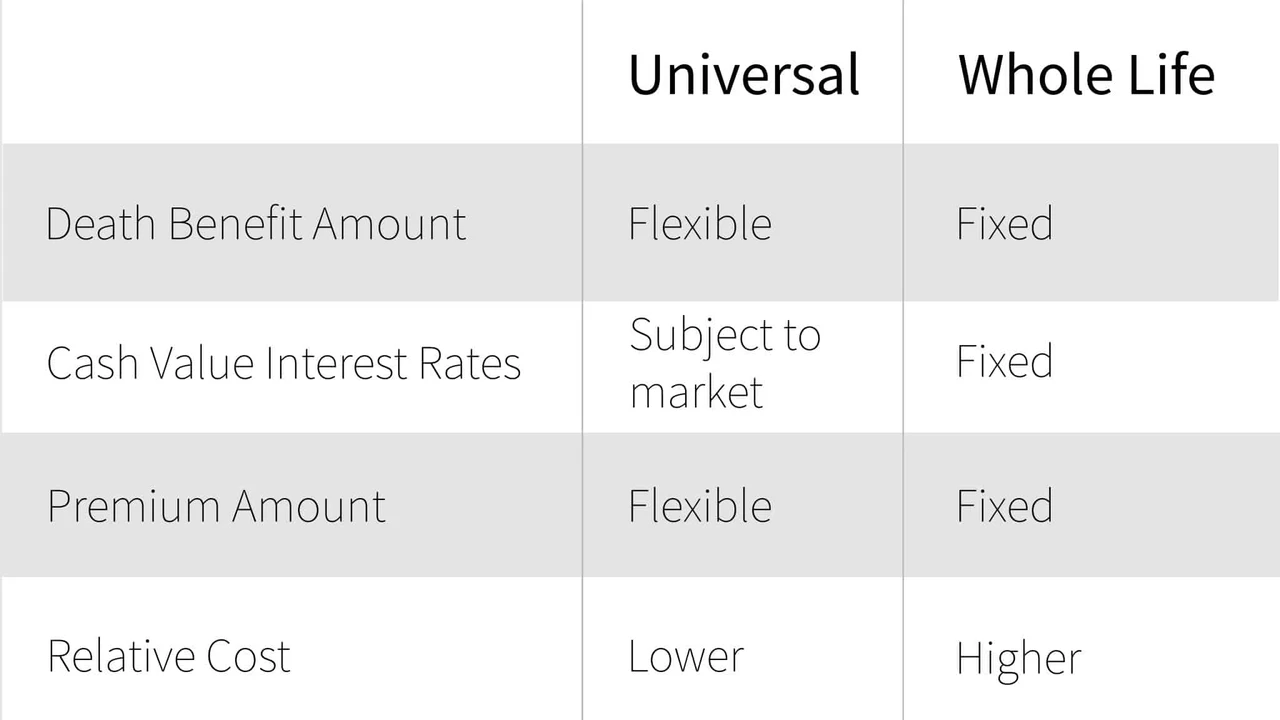

Key Differences Whole Life vs Universal Life at a Glance

Let's put them side-by-side to highlight the core distinctions:

- Premiums: Whole life has fixed, guaranteed premiums. Universal life offers flexible premiums.

- Death Benefit: Whole life has a guaranteed, fixed death benefit. Universal life allows for adjustable death benefits.

- Cash Value Growth: Whole life has guaranteed, fixed-rate growth (plus potential dividends). Universal life's cash value growth is based on declared interest rates (with a minimum guarantee) or market performance (for IUL/VUL).

- Complexity: Whole life is generally simpler. Universal life is more complex due to its flexibility and variable components.

- Risk: Whole life is lower risk due to guarantees. Universal life carries more risk, especially with market-linked options.

Choosing the Best Permanent Coverage for Your Needs Practical Scenarios

So, how do you decide? It really boils down to your personal financial situation, risk tolerance, and long-term goals.

When Whole Life Insurance Shines Stability and Predictability

Whole life is often ideal for individuals who prioritize stability and predictability above all else. If you want the peace of mind that comes with knowing your premiums will never change, your death benefit is guaranteed, and your cash value will steadily grow, whole life is a strong contender. It's particularly well-suited for:

- Conservative Savers: Those who prefer guaranteed returns over market-linked potential.

- Estate Planning: For ensuring a specific amount is passed to heirs without market fluctuations.

- Long-Term Financial Planning: As a foundational piece of a conservative financial plan.

- Individuals with Stable Income: Those who can comfortably commit to fixed premium payments.

When Universal Life Insurance is Preferred Flexibility and Growth Potential

Universal life, with its inherent flexibility, is often a better fit for those whose financial circumstances might change over time or who are comfortable with a bit more complexity for potentially higher returns. It's a good choice for:

- Individuals with Fluctuating Income: The ability to adjust premiums can be a lifesaver.

- Those Seeking Higher Cash Value Growth: IUL and VUL policies offer market-linked potential.

- People Who Want to Adjust Coverage: If you anticipate needing more or less coverage in the future.

- Business Owners: For business succession planning where flexibility is key.

Specific Product Recommendations and Use Cases for US and Southeast Asian Markets

Let's look at some hypothetical product examples and how they might be used, keeping in mind that actual policy features and availability vary greatly by insurer and region. Prices are illustrative and depend heavily on age, health, coverage amount, and riders.

Whole Life Insurance Products for US Market

1. Guardian Whole Life (e.g., Guardian Whole Life 99):

- Use Case: Ideal for individuals seeking maximum guarantees and potential for strong dividends. Excellent for conservative estate planning or as a core component of a long-term financial strategy.

- Key Features: Guaranteed level premiums, guaranteed death benefit, guaranteed cash value growth, and a strong history of paying competitive dividends. Offers various paid-up additions riders to enhance cash value and death benefit.

- Comparison: Known for its mutual structure, which often translates to higher dividend payouts compared to stock companies. Less flexible than UL but offers unparalleled stability.

- Illustrative Cost (Male, 35, non-smoker, $500,000 death benefit): ~$400-550 per month.

2. MassMutual Whole Life (e.g., MassMutual Whole Life Legacy 100):

- Use Case: Similar to Guardian, excellent for those prioritizing long-term, stable growth and wealth transfer. Often chosen by high-net-worth individuals for its robust cash value accumulation and dividend performance.

- Key Features: Strong dividend performance, guaranteed cash value growth, and a variety of riders including waiver of premium and accelerated death benefit.

- Comparison: Another top mutual company, often competing closely with Guardian on dividend rates and overall policy strength. Very similar in its guarantees and conservative approach.

- Illustrative Cost (Male, 35, non-smoker, $500,000 death benefit): ~$420-580 per month.

Universal Life Insurance Products for US Market

1. Pacific Life Pacific Discovery Xelerator IUL:

- Use Case: For individuals seeking cash value growth linked to market performance without direct market risk. Great for supplemental retirement income or long-term savings with a death benefit.

- Key Features: Cash value growth tied to an index (e.g., S&P 500) with a floor (guaranteed minimum return, often 0%) and a cap (maximum return). Offers flexible premiums and death benefit options.

- Comparison: Provides more growth potential than traditional UL or whole life, but less risk than VUL. More complex than whole life due to index crediting methods.

- Illustrative Cost (Male, 35, non-smoker, $500,000 death benefit): ~$250-400 per month (can vary widely based on funding strategy).

2. Transamerica Financial Foundation IUL:

- Use Case: Similar to Pacific Life IUL, suitable for those looking for flexible premiums and potential for higher cash value accumulation for future needs like college funding or retirement.

- Key Features: Indexed interest crediting, flexible premium payments, and various riders including chronic illness and critical illness riders.

- Comparison: A popular IUL product known for its competitive caps and participation rates. Offers a good balance of growth potential and flexibility.

- Illustrative Cost (Male, 35, non-smoker, $500,000 death benefit): ~$260-410 per month.

Life Insurance Products for Southeast Asian Markets (Illustrative Examples)

The life insurance landscape in Southeast Asia is diverse, with major global players and strong local insurers. Products often mirror those in the US but with local market adaptations.

1. AIA Singapore (e.g., AIA Guaranteed Protect Plus):

- Use Case: A whole life equivalent, suitable for Singaporeans seeking guaranteed lifelong protection and steady cash value growth. Often used for family protection and legacy planning.

- Key Features: Guaranteed cash value, guaranteed death benefit, and potential for non-guaranteed bonuses (similar to dividends). Offers various riders for critical illness, disability, etc.

- Comparison: A leading insurer in the region, known for comprehensive coverage and strong financial backing. Offers a more traditional, stable approach.

- Illustrative Cost (Male, 35, non-smoker, S$500,000 death benefit): ~$300-450 SGD per month.

2. Prudential Malaysia (e.g., PruLife Gift):

- Use Case: A universal life equivalent, offering flexibility for Malaysians whose financial needs may evolve. Can be used for long-term savings, retirement planning, and family protection.

- Key Features: Flexible premium payments, adjustable death benefit, and cash value growth based on declared interest rates. Often includes options for critical illness and disability riders.

- Comparison: Prudential is a major player in Malaysia, offering a wide range of flexible products. This type of policy provides more adaptability than traditional whole life.

- Illustrative Cost (Male, 35, non-smoker, RM500,000 death benefit): ~$400-600 RM per month.

3. Manulife Philippines (e.g., Manulife Affluence Gold):

- Use Case: An investment-linked universal life product, suitable for Filipinos who want life insurance protection combined with investment growth potential. Good for wealth accumulation and legacy.

- Key Features: Flexible premiums, adjustable death benefit, and cash value linked to investment funds chosen by the policyholder. Offers various fund options (equity, bond, balanced).

- Comparison: This is closer to a Variable Universal Life (VUL) product, offering higher growth potential but also higher risk due to market exposure. Requires more active management.

- Illustrative Cost (Male, 35, non-smoker, PHP5,000,000 death benefit): ~$5,000-8,000 PHP per month (can vary significantly based on investment allocation).

Important Note on Pricing: The illustrative costs provided are very rough estimates. Actual premiums depend on a multitude of factors including your exact age, health status (medical history, current conditions), lifestyle (smoking, dangerous hobbies), occupation, and the specific riders you choose. It's crucial to get personalized quotes from multiple insurers.

Accessing Your Cash Value How to Use Your Policy as a Living Benefit

One of the most attractive aspects of permanent life insurance is the ability to access its cash value during your lifetime. This can be done in a few ways:

Policy Loans Understanding the Mechanics

You can borrow against your policy's cash value. The loan interest rates are typically competitive, and you don't have to repay the loan on a strict schedule. However, any outstanding loan balance (plus interest) will reduce the death benefit paid to your beneficiaries. If the loan isn't repaid and the cash value runs out, the policy could lapse. This is a common way to access funds for emergencies, education, or even business opportunities without liquidating other assets.

Withdrawals What You Need to Know

You can also make withdrawals from your cash value. Unlike loans, withdrawals directly reduce the cash value and the death benefit. Withdrawals up to your basis (the amount you've paid in premiums) are generally tax-free. Withdrawals exceeding your basis may be taxable. It's important to understand the long-term impact of withdrawals on your policy's performance and longevity.

Surrendering Your Policy When It Makes Sense

If you no longer need the coverage, you can surrender your policy and receive the cash surrender value, which is the cash value minus any surrender charges. This is usually a last resort, as you'll lose your life insurance coverage. Surrender charges are typically higher in the early years of a policy and decrease over time.

Tax Implications of Whole Life and Universal Life Insurance What to Expect

Both whole life and universal life insurance offer significant tax advantages, which contribute to their appeal as financial planning tools.

Tax-Deferred Cash Value Growth A Key Benefit

The cash value in both types of policies grows on a tax-deferred basis. This means you don't pay taxes on the interest or investment gains as they accumulate, allowing your money to compound more efficiently over time. Taxes are only due if you withdraw more than your basis or surrender the policy for a gain.

Tax-Free Death Benefit for Beneficiaries

Perhaps the most significant tax benefit is that the death benefit paid to your beneficiaries is generally income tax-free. This ensures that your loved ones receive the full intended amount without it being reduced by income taxes.

Policy Loans and Withdrawals Tax Considerations

As mentioned, policy loans are generally tax-free, as they are considered debt, not income. Withdrawals up to your basis are also tax-free. However, if a policy lapses with an outstanding loan or if withdrawals exceed your basis, there could be taxable events. It's always wise to consult with a tax advisor when considering accessing your policy's cash value.

Making Your Decision Factors to Consider

Choosing between whole life and universal life is a personal decision. Here are some final thoughts to guide you:

- Your Financial Goals: Are you prioritizing guaranteed growth and stability, or flexibility and potentially higher returns?

- Risk Tolerance: How comfortable are you with market-linked performance versus guaranteed rates?

- Budget: Can you commit to fixed, higher premiums for whole life, or do you need the flexibility of universal life?

- Future Needs: Do you anticipate your coverage needs or financial situation changing significantly?

- Complexity: Are you comfortable managing a more complex policy like universal life, or do you prefer the simplicity of whole life?

Ultimately, both whole life and universal life insurance can be powerful tools for financial protection and wealth accumulation. The 'best' choice isn't universal; it's the one that aligns perfectly with your unique circumstances and long-term vision. Don't hesitate to consult with a qualified financial advisor who can help you analyze your situation and recommend the most suitable option for you and your family.

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)