Learn why and when it's important to regularly review your life insurance policy to ensure it still meets your needs.

Learn why and when it's important to regularly review your life insurance policy to ensure it still meets your needs.

Reviewing Your Life Insurance Policy When and Why

Understanding the Importance of Regular Life Insurance Policy Reviews

Hey there! So, you've got a life insurance policy, right? That's awesome! It means you've taken a crucial step to protect your loved ones financially. But here's a little secret: buying a policy isn't a one-and-done deal. Just like you wouldn't buy a car and never check the oil, you shouldn't set and forget your life insurance. Regularly reviewing your life insurance policy is super important to make sure it still fits your life like a glove. Think about it – your life changes, and so should your financial safety net. This isn't just about making sure you're covered; it's about making sure you're covered *correctly* and *efficiently*. We're talking about ensuring your policy aligns with your current life stage, financial goals, and family needs. Neglecting this can lead to being underinsured, overpaying, or even having a policy that no longer serves its original purpose. So, let's dive into why and when you should be giving your policy a good once-over.

Key Life Events Triggering a Life Insurance Policy Review

Life is a rollercoaster, full of twists and turns. And guess what? Many of these twists and turns are big signals that it's time to look at your life insurance. These aren't just minor bumps; they're major life events that can significantly alter your financial responsibilities and future plans. Let's break down some of the big ones:

Marriage or Divorce How Relationships Impact Your Coverage

Getting hitched? Congrats! Marriage often means combining finances and taking on new shared responsibilities. Your spouse might become a primary beneficiary, and you might want to increase your coverage to protect your new joint future. On the flip side, divorce is a huge game-changer. You'll likely need to update beneficiaries, adjust coverage amounts, and potentially even split policies as part of a settlement. It's a critical time to ensure your ex-spouse isn't still listed as a beneficiary if that's not your intention, and that your children are adequately protected.

Having Children or Adopting Expanding Your Family and Responsibilities

Little bundles of joy bring immense happiness, but also significant financial obligations. From diapers to college tuition, children are expensive! When you have a child, your need for life insurance typically skyrockets. You'll want enough coverage to ensure they're financially secure if you're no longer around. This might mean increasing your death benefit significantly to cover their upbringing, education, and future needs. Adoption falls into the same category – new family members mean new responsibilities.

Buying a Home or Taking on Significant Debt Mortgage Protection

A new home is exciting, but it also comes with a hefty mortgage. For most people, a mortgage is their largest debt. Life insurance can be a fantastic way to ensure your family can stay in their home if something happens to you. Reviewing your policy after buying a home means making sure your coverage is sufficient to pay off the mortgage, preventing your loved ones from facing foreclosure during an already difficult time. The same goes for other significant debts, like large business loans or substantial personal loans – you want to make sure these don't become a burden on your family.

Career Changes Promotions or Job Loss Adjusting to New Income Levels

Got a big promotion and a fatter paycheck? Awesome! This might mean you can afford more coverage, or perhaps you want to invest in a different type of policy. Conversely, a job loss or a significant pay cut might mean you need to adjust your premiums or even consider a more affordable policy temporarily. Your income directly impacts your ability to pay premiums and your overall financial contribution to your family, so any major career shift warrants a review.

Retirement Planning and Estate Considerations Shifting Financial Priorities

As you approach retirement, your financial needs change dramatically. Your kids might be grown and out of the house, your mortgage might be paid off, and your income might be shifting from salary to retirement savings. At this stage, your life insurance might transition from income replacement to estate planning. You might want to ensure your policy helps cover estate taxes, leaves a legacy, or provides for specific beneficiaries. This is also a good time to consider if you still need as much coverage as you did when you were younger.

Changes in Health or Lifestyle Impact on Premiums and Insurability

Have you quit smoking? Lost a significant amount of weight? Started running marathons? These positive health changes could lead to lower premiums! It's worth checking if you can get a better rate. On the other hand, if your health has declined, it's still important to review your policy. While new coverage might be more expensive, understanding your current insurability is crucial. Don't forget about lifestyle changes like taking up a new, risky hobby – these can sometimes affect your policy terms.

Annual Check-ups Why a Yearly Review is a Smart Move

Even without a major life event, a yearly check-up for your life insurance policy is a brilliant idea. Think of it like your annual physical – a routine check to ensure everything is in good working order. This proactive approach helps you stay on top of your financial planning and avoid any surprises down the road.

Ensuring Beneficiary Designations Are Current and Correct

This is a big one! Life happens, and sometimes we forget to update who gets the money. A yearly review is the perfect time to confirm your beneficiaries are still who you intend them to be. Did you get married? Have another child? Did a named beneficiary pass away? You'll want to make sure the right people are listed, and that contingent beneficiaries are also in place. This prevents potential legal headaches and ensures your wishes are honored.

Assessing Coverage Adequacy Is Your Policy Still Enough

Inflation, rising costs of living, and changing financial goals mean that the coverage amount you chose years ago might not be enough today. A yearly review allows you to reassess if your death benefit is still sufficient to cover your family's needs, including future expenses, debts, and income replacement. You might find you need to increase your coverage, especially if your income has grown or you've taken on more financial responsibilities.

Evaluating Policy Performance and Cash Value Growth for Permanent Policies

If you have a permanent life insurance policy (like whole life or universal life), it likely has a cash value component. A yearly review is a great time to check how that cash value is performing. Is it growing as expected? Are the dividends (for participating policies) meeting projections? Understanding the cash value growth is crucial for policies intended for wealth accumulation or retirement planning. This also helps you understand if the policy is meeting its long-term financial objectives.

Comparing Current Market Rates and New Product Offerings

The insurance market is always evolving. New products emerge, and rates can change. A yearly review gives you an opportunity to see if there are better deals out there or new policy features that might benefit you. You might find that you can get more coverage for the same price, or even reduce your premiums for the same coverage. This doesn't necessarily mean switching policies every year, but it keeps you informed and ensures you're not missing out on potential savings or improved benefits.

Understanding Policy Riders and Their Continued Relevance

When you first bought your policy, you might have added various riders – like a waiver of premium, accidental death benefit, or a long-term care rider. A yearly review is a good time to check if these riders are still relevant to your current situation. For example, if you've paid off your mortgage, a mortgage protection rider might no longer be necessary. Conversely, you might realize you need to add a new rider, like a critical illness rider, to enhance your coverage.

Practical Steps for Reviewing Your Life Insurance Policy

Okay, so you're convinced a review is a good idea. But how do you actually do it? It's not as complicated as it sounds. Here's a straightforward approach:

Gather All Policy Documents and Information

First things first, dig out all your policy documents. This includes your policy contract, any annual statements, and records of premium payments. Having everything in one place will make the review process much smoother. If you can't find them, contact your insurance provider or agent – they can usually provide copies or access your policy details online.

Contact Your Insurance Agent or Financial Advisor

Your insurance agent or financial advisor is your best friend here. They have expertise and access to your policy details. Schedule a meeting or a call with them. They can help you understand the jargon, explain your policy's features, and guide you through the review process. They can also provide insights into market changes and new product offerings.

Assess Your Current Financial Situation and Future Needs

Before you talk to anyone, take some time to think about your current financial picture. What's your income? What are your debts? What are your family's expenses? What are your long-term financial goals (e.g., college savings, retirement, leaving an inheritance)? Be honest with yourself about how much financial support your family would need if you were no longer there. This self-assessment is crucial for determining if your current coverage is adequate.

Consider Potential Policy Adjustments or New Coverage Options

Based on your review, you might decide to make some changes. This could involve increasing or decreasing your death benefit, adding or removing riders, changing beneficiaries, or even considering a different type of policy altogether. Your agent can help you explore these options and provide quotes for any adjustments. Don't be afraid to ask questions and explore all possibilities.

Specific Product Recommendations and Scenarios

Let's get a bit more concrete. Depending on your situation, certain types of policies or adjustments might be more suitable. Here are a few scenarios and product recommendations, keeping in mind that these are general suggestions and a personalized consultation with a financial advisor is always best.

Scenario 1 Young Family with a New Mortgage

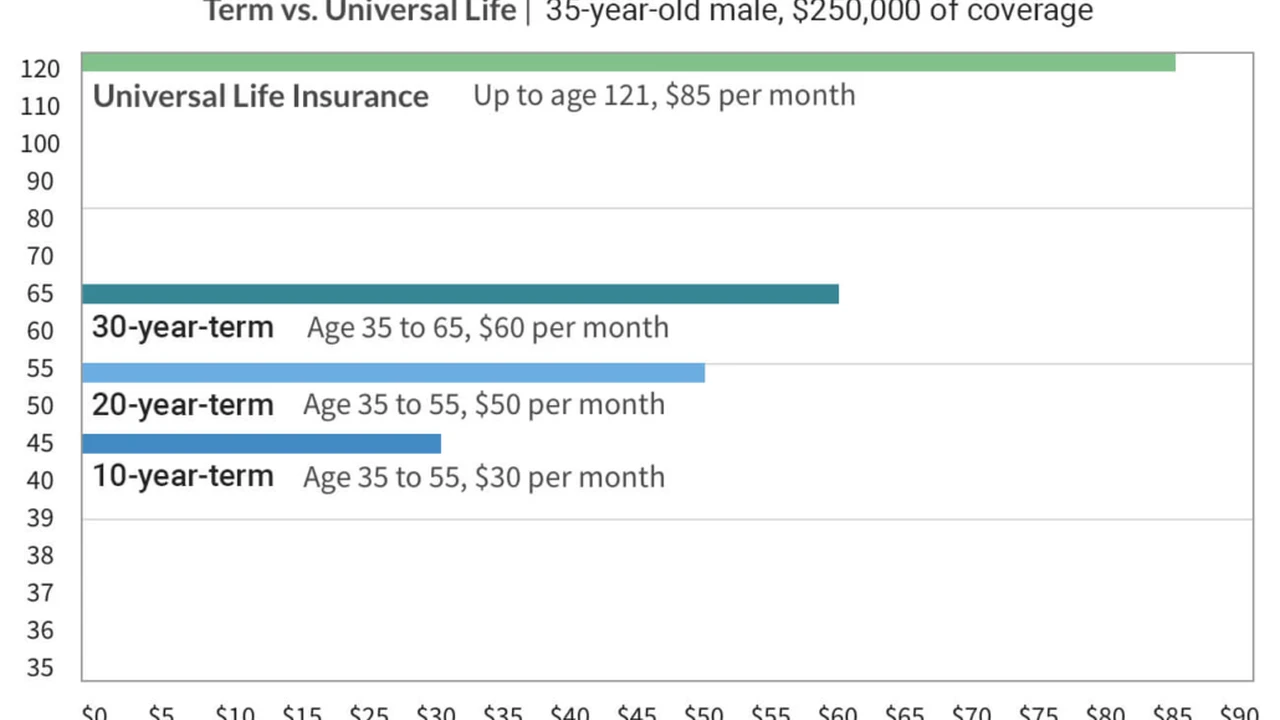

If you're a young couple with a new baby and a fresh mortgage, your primary concern is likely income replacement and debt protection. You want to ensure your family can maintain their lifestyle and stay in their home if something happens to you. For this scenario, **Term Life Insurance** is often the most cost-effective solution.

* **Recommended Product:** A 20 or 30-year term life policy with a death benefit sufficient to cover your mortgage, several years of income replacement, and future expenses like childcare and education. For example, a $1,000,000 20-year term policy.

* **Specific Providers (US Market Examples):**

* **Haven Life (backed by MassMutual):** Known for its straightforward online application process and competitive rates for healthy individuals. You can often get a quote and even approval without a medical exam for certain coverage amounts.

* **Policygenius (Brokerage):** Not an insurer itself, but a fantastic platform to compare quotes from multiple top-rated carriers like Lincoln Financial, AIG, and Pacific Life. This allows you to see a range of options and find the best fit for your budget and needs.

* **Ladder Life:** Offers flexible term life insurance where you can increase or decrease your coverage as your needs change, without having to buy a new policy. This is great for dynamic life stages.

* **Pricing Example (Illustrative, highly variable):** For a healthy 30-year-old non-smoker in the US, a $1,000,000 20-year term policy could range from $30-$60 per month, depending on the insurer and specific health ratings. Adding a child rider (which provides a small amount of coverage for each child) is usually very inexpensive, often just a few dollars a month.

Scenario 2 Mid-Career Professional Approaching Retirement

As you get closer to retirement, your income replacement needs might decrease, but estate planning and wealth transfer become more prominent. You might have paid off your mortgage, and your children are financially independent. Here, **Whole Life Insurance** or **Guaranteed Universal Life (GUL)** can be excellent choices.

* **Recommended Product:** A whole life policy with a focus on guaranteed cash value growth and a guaranteed death benefit, or a GUL policy designed to provide lifelong coverage at a fixed premium.

* **Specific Providers (US Market Examples):**

* **Northwestern Mutual:** A highly-rated mutual company known for its participating whole life policies that pay dividends. Excellent for long-term, stable growth and estate planning.

* **MassMutual:** Another strong mutual company offering competitive whole life products with good dividend performance.

* **Guardian Life:** Also a mutual company, offering robust whole life policies with strong financial ratings and dividend potential.

* **Pacific Life (for GUL):** Often has competitive GUL products that offer lifelong coverage with fixed premiums, providing peace of mind without the investment risk of other universal life options.

* **Pricing Example (Illustrative, highly variable):** For a healthy 50-year-old non-smoker in the US, a $500,000 whole life policy could range from $500-$1000+ per month, depending on the insurer, health, and dividend scale. A GUL policy for the same coverage might be slightly less, perhaps $300-$700 per month, as it focuses purely on the death benefit guarantee rather than significant cash value growth.

Scenario 3 Business Owner with Key Employees

If you own a business, your life insurance needs extend beyond your family. You need to protect the business itself. **Key Person Life Insurance** is crucial here, often using a permanent policy type.

* **Recommended Product:** A whole life or universal life policy on a key employee (or yourself as the owner) with the business as the beneficiary. The death benefit would cover losses due to the key person's absence, recruitment costs, and business continuity.

* **Specific Providers (US Market Examples):**

* **Prudential:** Offers a wide range of permanent life insurance options suitable for business planning, including competitive universal life products.

* **Transamerica:** Known for its flexible universal life policies that can be tailored for business needs.

* **Nationwide:** Provides strong support for business owners with various life insurance solutions, including those for buy-sell agreements and key person coverage.

* **Pricing Example (Illustrative, highly variable):** The cost will depend heavily on the age and health of the key person, and the desired death benefit. A $1,000,000 universal life policy on a healthy 45-year-old key employee could range from $200-$500+ per month.

Scenario 4 Single Individual with No Dependents but Wants to Leave a Legacy

Even if you don't have dependents, life insurance can still be valuable. You might want to cover final expenses, leave money to a charity, or provide for a specific individual. **Final Expense Insurance** or a smaller **Whole Life Policy** can be suitable.

* **Recommended Product:** A guaranteed issue whole life policy for final expenses, or a small whole life policy to leave a specific legacy.

* **Specific Providers (US Market Examples):**

* **Mutual of Omaha:** A leading provider of guaranteed issue whole life insurance, often marketed as final expense insurance. Easy application with no medical exam.

* **Gerber Life:** Offers guaranteed issue whole life, often for smaller coverage amounts, and is well-known for its child life insurance which can also be used for adults.

* **AARP (through New York Life):** Provides simplified issue whole life options for seniors, often with no medical exam required.

* **Pricing Example (Illustrative, highly variable):** For a 65-year-old, a $10,000 guaranteed issue final expense policy could be $50-$100+ per month, depending on the provider and gender. These policies are more expensive per dollar of coverage due to the lack of medical underwriting.

Common Pitfalls to Avoid During Your Policy Review

While reviewing your policy is a great step, there are a few traps you'll want to steer clear of:

Ignoring the Fine Print and Policy Exclusions

It's easy to skim, but the devil is in the details. Make sure you understand any exclusions, limitations, or specific conditions in your policy. For example, some policies have a suicide clause or exclusions for certain high-risk activities. Knowing these upfront prevents nasty surprises later.

Underestimating Your Coverage Needs for the Future

Don't just think about today. Project your financial needs into the future. Consider inflation, potential future debts, and long-term goals like college education for your kids or your spouse's retirement. It's better to be slightly overinsured than significantly underinsured.

Making Hasty Decisions Without Professional Advice

Life insurance is a complex financial product. Don't cancel a policy or make major changes without consulting with a qualified insurance agent or financial advisor. They can help you understand the implications of any changes and ensure you're making the best decision for your unique situation.

Forgetting to Update Beneficiary Information Regularly

This is a recurring theme because it's so important! Life changes, and so do relationships. Always, always, always double-check your beneficiaries. An outdated beneficiary designation can lead to your death benefit going to the wrong person or getting tied up in probate court.

Focusing Solely on Price Over Coverage and Company Stability

While cost is a factor, it shouldn't be the only one. A cheap policy that doesn't provide adequate coverage or is from an unstable company isn't a good deal. Look for a balance between affordability, comprehensive coverage, and the financial strength and reputation of the insurance provider. You want an insurer that will be around to pay claims when your family needs them most.

The Long-Term Benefits of Proactive Life Insurance Management

So, why go through all this trouble? Because proactive life insurance management pays off big time. It's not just about having a policy; it's about having the *right* policy that evolves with you. By regularly reviewing and adjusting your coverage, you're ensuring that your financial safety net remains strong and effective. This means peace of mind for you, knowing that your loved ones are truly protected, no matter what life throws your way. It means avoiding potential financial distress for your family during an already difficult time. It means your legacy and financial wishes are honored. So, make that annual review a habit – your future self, and your family, will thank you for it.

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)