Understanding Universal Life Insurance Fees and Charges

Discover survivorship life insurance, also known as second-to-die, and its role in estate planning for couples.

Discover survivorship life insurance, also known as second-to-die, and its role in estate planning for couples.

Survivorship Life Insurance for Couples Estate Planning

Hey there! Let's talk about something super important for couples, especially those thinking about their legacy and estate planning: survivorship life insurance. You might have heard it called 'second-to-die' insurance, and while that name sounds a bit grim, the policy itself is actually a fantastic tool for ensuring your loved ones are taken care of after both you and your partner are gone. It's not about replacing income for a surviving spouse, but rather about providing a lump sum of cash when the second person passes away. This can be incredibly useful for covering estate taxes, leaving a substantial inheritance, or funding a charitable gift. So, let's dive in and explore everything you need to know about this unique and powerful financial product.

What is Survivorship Life Insurance Understanding Second to Die Policies

Alright, let's break down the basics. Survivorship life insurance is a type of permanent life insurance policy that covers two lives, usually a married couple, but it can also be used for business partners or even parent-child relationships. The key differentiator here is that the death benefit isn't paid out until the second insured person passes away. This is why it's often referred to as 'second-to-die' insurance. Unlike traditional individual life insurance where the payout happens after one person dies, survivorship policies are designed for a later distribution. This structure makes it particularly cost-effective compared to buying two separate permanent policies, especially if one of the insured individuals has health issues that would make individual coverage expensive.

The policy accumulates cash value over time, just like other permanent life insurance products such as whole life or universal life. This cash value can grow on a tax-deferred basis and can be accessed later in life through loans or withdrawals, though doing so will reduce the death benefit. The premiums are typically paid until the second death, or for a specified period, depending on the policy type. Because the insurance company knows they'll eventually pay out, but not until both individuals have passed, they can offer more favorable rates. This makes it an attractive option for specific estate planning goals.

Why Couples Choose Survivorship Life Insurance Estate Tax Planning and Inheritance

So, why would a couple opt for this kind of policy? The primary reason, and arguably the most common, is estate tax planning. When a wealthy individual or couple passes away, their estate might be subject to federal and/or state estate taxes. These taxes can be substantial, sometimes reaching 40% or more of the estate's value above a certain exemption limit. While the federal estate tax exemption is quite high (over $13 million per individual in 2024), it's not always permanent and can change with new legislation. Plus, some states have much lower exemption thresholds. When the second spouse dies, the entire estate often becomes taxable, and without liquid assets, heirs might be forced to sell valuable assets, like a family business or real estate, just to pay the taxes. Survivorship life insurance provides a tax-free death benefit that can be used to cover these estate taxes, ensuring that the full value of the estate passes to the intended beneficiaries.

Beyond estate taxes, it's also a fantastic tool for leaving a substantial inheritance. Maybe you want to ensure your children or grandchildren receive a significant sum of money, or perhaps you want to leave a legacy to a specific charity. Since the death benefit is typically paid out tax-free to beneficiaries, it's an efficient way to transfer wealth. It can also be used to equalize inheritances among children, especially if some children are involved in a family business and others are not. The policy can provide a cash payout to those not involved in the business, ensuring fairness.

Comparing Survivorship Life Insurance with Other Life Insurance Types

Let's put survivorship life insurance into perspective by comparing it to other common types of life insurance. You've got your term life, your whole life, and your universal life. Each has its place, but survivorship stands out for its specific purpose.

Survivorship vs Term Life Insurance

Term life insurance is straightforward: it covers you for a specific period (e.g., 10, 20, or 30 years) and pays out if you die within that term. It's great for covering temporary needs like a mortgage or raising young children. However, it doesn't build cash value and expires at the end of the term. Survivorship life insurance, on the other hand, is permanent. It lasts your entire life (and your partner's) and is designed for long-term estate planning needs, not temporary income replacement. The death benefit is guaranteed as long as premiums are paid, and it builds cash value.

Survivorship vs Individual Whole Life Insurance

Whole life insurance is a permanent policy that covers one individual, offers guaranteed premiums, a guaranteed death benefit, and guaranteed cash value growth. If a couple wanted permanent coverage for estate planning, they could buy two separate whole life policies. However, survivorship life insurance is often more cost-effective. Because the payout is deferred until the second death, the insurance company has a longer time to invest the premiums, which translates to lower premiums for the couple compared to two individual whole life policies, especially if one spouse has health issues. The underwriting for survivorship policies can also be more lenient if one applicant is in poor health, as the risk is spread across two lives.

Survivorship vs Individual Universal Life Insurance

Universal life (UL) insurance is another type of permanent policy known for its flexibility. It allows you to adjust premiums and death benefits within certain limits. There are also different types of UL, like Indexed Universal Life (IUL) and Guaranteed Universal Life (GUL). Survivorship policies can also be structured as universal life, offering similar flexibility but still covering two lives and paying out on the second death. The choice between a survivorship whole life and a survivorship universal life often comes down to how much flexibility you want with premiums and cash value growth, versus the guarantees offered by whole life.

Key Features and Benefits of Second to Die Policies

Let's zoom in on some of the cool features and benefits that make survivorship life insurance such a valuable tool:

- Lower Premiums: As we touched on, because the death benefit isn't paid until the second death, the insurance company has a longer time horizon. This generally results in lower premiums compared to purchasing two individual permanent policies.

- Estate Tax Efficiency: This is the big one. The death benefit can be used to pay estate taxes, preventing the forced sale of assets and preserving the full value of the estate for heirs.

- Wealth Transfer: It's an excellent way to transfer wealth to future generations or leave a significant charitable legacy, often tax-free to the beneficiaries.

- Cash Value Growth: Like other permanent policies, survivorship policies build cash value on a tax-deferred basis. This cash value can be accessed later in life if needed, though it will reduce the death benefit.

- Guaranteed Payout: As long as premiums are paid, the death benefit is guaranteed to be paid out upon the second death, providing certainty for your estate plan.

- Lenient Underwriting: If one spouse has significant health issues, it might be difficult or very expensive for them to get an individual policy. With survivorship insurance, the healthier spouse can often offset the risk of the less healthy spouse, making the policy more accessible and affordable.

- Business Succession Planning: Beyond personal estate planning, survivorship policies can be used in business contexts, for example, to fund a buy-sell agreement when two business partners pass away.

Potential Drawbacks and Considerations for Couples

While survivorship life insurance offers many advantages, it's not a one-size-fits-all solution. There are a few things to consider:

- No Payout on First Death: This is the most significant point. If one spouse dies, there's no death benefit paid out to the surviving spouse. If the surviving spouse needs income replacement or funds to cover immediate expenses, a separate individual policy would be necessary.

- Long-Term Commitment: These are permanent policies, meaning you're generally committing to paying premiums for a long time, potentially for the rest of your lives.

- Complexity: Estate planning can be complex, and survivorship policies often involve trusts (more on that later) to maximize their benefits. This means working with financial advisors and estate attorneys.

- Cash Value Access: While cash value grows, accessing it reduces the death benefit. It's primarily designed for the death benefit, not as a primary savings vehicle.

- Divorce: If a couple divorces, managing a survivorship policy can become complicated. It's crucial to have a plan for this contingency.

How Survivorship Life Insurance Works with Irrevocable Life Insurance Trusts ILITs

This is where things get a bit more technical, but it's super important for maximizing the benefits of survivorship life insurance. Often, survivorship policies are owned by an Irrevocable Life Insurance Trust (ILIT). Why? Because if you, as the insured, own the policy, the death benefit could be included in your taxable estate. By having an ILIT own the policy, the death benefit is typically excluded from both spouses' taxable estates, making it truly estate tax-free for your beneficiaries.

Here's a simplified breakdown:

- You (the grantor) create an ILIT and name a trustee (often a trusted family member or professional).

- The ILIT applies for and owns the survivorship life insurance policy.

- You make gifts to the ILIT (these are often called 'Crummey notices' to qualify for the annual gift tax exclusion), which the trustee then uses to pay the policy premiums.

- When the second spouse dies, the death benefit is paid directly to the ILIT, which then distributes the funds to your named beneficiaries according to the trust's terms.

This structure ensures that the death benefit bypasses the estate, avoiding estate taxes and probate. It's a sophisticated strategy, so working with an experienced estate planning attorney is crucial to set up an ILIT correctly.

Real World Scenarios When Survivorship Life Insurance Shines

Let's look at some practical examples where this type of policy really makes a difference:

- Wealthy Couples with Large Estates: For couples whose combined assets exceed the federal or state estate tax exemption limits, a survivorship policy in an ILIT is almost a no-brainer to cover potential tax liabilities.

- Family Business Owners: If a couple owns a family business they want to pass down to their children, but some children aren't involved in the business, the policy can provide liquidity to those not inheriting the business, ensuring an equitable distribution of wealth.

- Charitable Giving: A couple passionate about a particular cause can use a survivorship policy to leave a substantial, tax-free donation to their chosen charity after they're both gone.

- Special Needs Planning: For parents of a child with special needs, a survivorship policy can fund a special needs trust, providing for the child's long-term care and financial well-being without jeopardizing government benefits.

- Blended Families: In blended families, a survivorship policy can ensure that assets are distributed fairly to children from different marriages, especially when combined with a trust.

Top Survivorship Life Insurance Providers and Products

When it comes to choosing a provider, you'll want to look for financially strong companies with a good reputation for customer service and competitive policy features. Here are a few of the big players in the US market that offer survivorship life insurance, along with some general product types they might offer. Remember, specific product names and features can change, so always check with a qualified agent.

Northwestern Mutual

- Product Type: Often known for its participating whole life insurance, Northwestern Mutual offers survivorship whole life policies that can pay dividends.

- Key Features: Strong financial ratings, potential for dividends (which can increase cash value or reduce premiums), guaranteed cash value growth, and a focus on personalized financial planning.

- Use Case: Ideal for couples seeking maximum guarantees, long-term stability, and the potential for dividend growth to offset future costs or enhance the death benefit.

- Pricing: Generally considered a premium provider, so premiums might be higher than some competitors, but the guarantees and dividend potential can be very attractive over the long term.

MassMutual

- Product Type: Another mutual company offering participating whole life survivorship policies.

- Key Features: Excellent financial strength, competitive dividend rates, strong guarantees on cash value and death benefit, and a focus on policyholder benefits.

- Use Case: Similar to Northwestern Mutual, MassMutual is great for couples prioritizing guarantees, dividend potential, and a company with a long history of financial stability.

- Pricing: Competitive within the participating whole life space, offering good value for the guarantees provided.

Pacific Life

- Product Type: Offers a range of universal life products, including survivorship universal life (SUL) and survivorship indexed universal life (SIUL).

- Key Features: Flexibility in premium payments and death benefits, potential for higher cash value growth with SIUL linked to market indexes (without direct market participation risk), and various rider options.

- Use Case: Suitable for couples who want more flexibility than whole life, are comfortable with some market-linked growth potential (for SIUL), and are looking for competitive pricing.

- Pricing: Can be more competitive than whole life, especially for SUL, with SIUL offering potential for higher cash value accumulation but also more variability.

Transamerica

- Product Type: Known for its universal life and indexed universal life offerings, including survivorship options.

- Key Features: Competitive pricing, a variety of index-linking options for IUL, and riders for long-term care or chronic illness.

- Use Case: Good for couples looking for flexible, potentially lower-cost options with the opportunity for cash value growth tied to market performance.

- Pricing: Often very competitive, especially for IUL products, making it an attractive option for those seeking value.

Prudential

- Product Type: Offers survivorship universal life (SUL) and survivorship guaranteed universal life (SGUL) policies.

- Key Features: Strong financial ratings, competitive guaranteed universal life options for those prioritizing a guaranteed death benefit with fixed premiums, and a range of riders.

- Use Case: Excellent for couples who want the certainty of a guaranteed death benefit and predictable premiums, or those looking for flexible universal life options.

- Pricing: SGUL can be very cost-effective for a guaranteed death benefit, while SUL offers more flexibility.

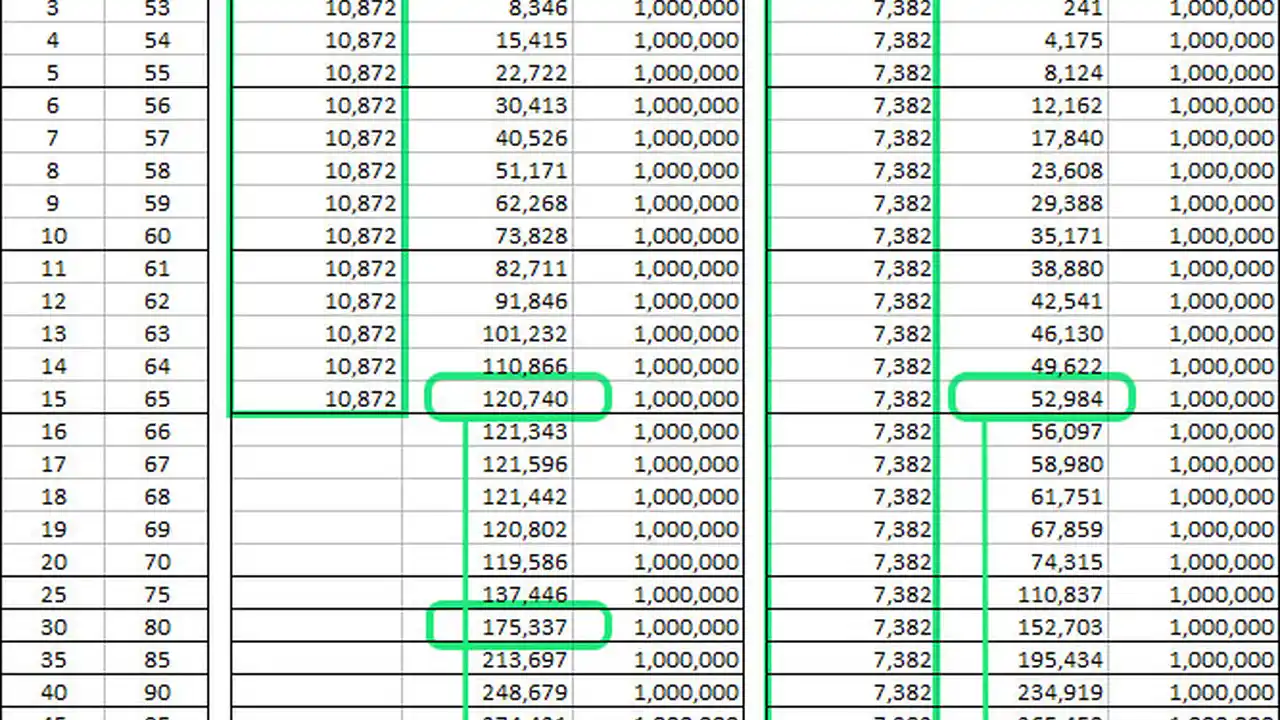

Important Note on Pricing: Providing exact 'prices' for life insurance is impossible without a detailed quote based on individual factors like age, health, lifestyle, coverage amount, and specific policy features. However, generally speaking, survivorship policies tend to have lower premiums than two comparable individual permanent policies. For example, a healthy couple in their 50s looking for a $1 million survivorship policy might see annual premiums ranging from $5,000 to $15,000, depending on the company, policy type (whole life vs. universal life), and specific health ratings. This is a very broad estimate, and a personalized quote is always necessary.

Choosing the Right Survivorship Policy for Your Needs

Selecting the best survivorship policy isn't a decision to take lightly. Here's a checklist of factors to consider:

- Your Estate Planning Goals: Are you primarily concerned with estate taxes, leaving an inheritance, or charitable giving? Your main objective will guide the type of policy and features you need.

- Budget: How much are you comfortable paying in premiums annually? This will influence the coverage amount and policy type you can afford.

- Desired Flexibility: Do you want the guarantees of whole life, or the flexibility and potential for higher cash value growth of universal life or indexed universal life?

- Health of Both Spouses: While survivorship policies can be more lenient, the health of both individuals will still impact underwriting and premium costs.

- Cash Value Needs: Do you anticipate needing to access the cash value during your lifetime? If so, consider policies with stronger cash value growth potential.

- Company Financial Strength: Always choose an insurer with high financial ratings (e.g., from A.M. Best, S&P, Moody's) to ensure they'll be around to pay the claim decades down the line.

- Riders and Features: Look for riders that might be beneficial, such as long-term care riders (if available on survivorship policies), or guaranteed insurability options.

Working with a Financial Advisor and Estate Attorney

Seriously, this isn't a DIY project. Survivorship life insurance is a sophisticated financial tool that's best integrated into a comprehensive estate plan. You'll want to work with a team of professionals:

- Experienced Life Insurance Agent/Financial Advisor: They can help you compare different policies, illustrate various scenarios, and guide you through the application process. They'll also help you understand the nuances of each product.

- Estate Planning Attorney: Crucial for setting up an Irrevocable Life Insurance Trust (ILIT) if you want the death benefit to be estate tax-free. They'll ensure your trust is legally sound and aligns with your overall estate plan.

These professionals can help you navigate the complexities, ensure your policy is structured correctly, and that it aligns perfectly with your long-term financial and legacy goals. Don't underestimate the value of expert advice here.

The Future of Your Legacy Securing Your Family's Financial Future

Ultimately, survivorship life insurance is about securing your family's financial future and ensuring your legacy is preserved exactly as you intend. It's a thoughtful way for couples to plan for the inevitable, mitigate potential tax burdens, and provide a lasting gift to their loved ones or cherished causes. By understanding how it works, its benefits, and how to integrate it into your broader estate plan, you can make an informed decision that provides peace of mind for years to come. It's not just about insurance; it's about a carefully constructed plan for the future you envision for your family.

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)